Healthcare Services

Vietnam Home Healthcare Market Analysis

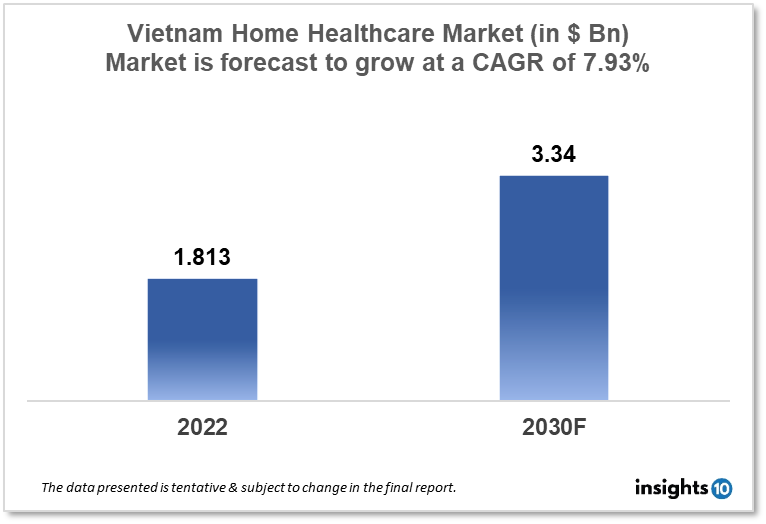

Vietnam's home healthcare market was valued at $1.813 Bn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 7.93% from 2022 to 2030 and will reach $3.34 Bn in 2030. One of the main reasons propelling the growth of this market is the introduction of newer technologies and the ageing population. The market is segmented by components and services. Some key players in this market are FPT Healthcare, Family Medical Practice, Viet Phap Hospital, Tam Duc Heart Hospital, Hoan My Medical Corporation, International SOS Vietnam, and VietCare Medical Services.

Buy Now

Vietnam Home Healthcare Market Executive Summary

Vietnam's home healthcare market was valued at $1.813 Bn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 7.93% from 2022 to 2030 and will reach $3.34 Bn in 2030. With a GDP per capita of $3694.02 in 2021, Vietnam has evolved into a lower-middle-income nation. Vietnam will have a GDP of around $368 Bn in 2021, ranking as the fifth-largest economy in Southeast Asia and 41st overall, according to the International Monetary Fund's (IMF) World Economic Outlook. According to The World Bank's projections, by 2026, the middle and affluent class will make up 26% of the population of the nation. The demand for high-quality healthcare services is rising in Vietnam, and this demand is a major driver for healthcare service providers. Vietnam's healthcare spending per capita is predicted to increase 9.2% a year between 2009 and 2025, reaching $262 by that time (USD 26 Bn of the overall market), or 5.8% of the nation's GDP.

Vietnam has made commendable progress on important measures of quality of life, including life expectancy, infant mortality, and access to reasonably priced medications. The government's concerted efforts to update the healthcare system and increase access to affordable care have been successful, as seen by this achievement. While retaining a commitment to sustainable healthcare finance, Vietnam has increased its Universal Health Coverage (UHC) to 90% of the population and aims to reach a 95% coverage percentage by 2025. This aim and coverage ratio outperform comparable local marketplaces. Vietnam is establishing the groundwork for a modern healthcare system that combines disease management, medical examination, and treatment.

Market Dynamics

Market Growth Drivers

The aging population in Vietnam is increasing, leading to an increase in demand for home healthcare services. With the rise in chronic diseases such as diabetes and cardiovascular disease is driving the demand for home healthcare services. Increasing awareness of home healthcare services and their benefits is driving the growth of the market. The Vietnamese government has implemented policies to support the development of the home healthcare sector, including tax incentives for companies operating in the sector. Technological advancements have made healthcare devices portable, user-friendly, and more convenient for patients at home or traveling. The introduction of newer technologies in this market has greatly boosted the current communication flow between patients and healthcare providers, enabling better, faster, and more effective care. Home healthcare services are more cost-effective compared to traditional hospital-based care, which is driving demand for these services.

Market Restraints

There is a shortage of trained and qualified personnel in the home healthcare sector, which is hindering the growth of the market. Despite the increasing awareness of home healthcare services, there is still a low level of awareness among the general population, which is hindering the growth of the market. Many areas in Vietnam lack the infrastructure necessary to provide home healthcare services, such as adequate transportation and communication systems the same time Many home healthcare providers do not have access to the latest technologies and innovations in home healthcare, which can limit the range of services they can provide. Reimbursement policies for home healthcare services in Vietnam are poor, which is affecting the growth of the market.

Competitive Landscape

Key Players

- FPT Healthcare

- Family Medical Practice

- Viet Phap Hospital

- Tam Duc Heart Hospital

- Hoan My Medical Corporation

- International SOS Vietnam

- VietCare Medical Services

- Hanoi French Hospital

- Ho Chi Minh City International Hospital

- Da Nang Hospital

Notable Deals

In 2022, Viet Phap Hospital entered into a partnership with Medtronic, a global medical technology company, to provide home healthcare services in Vietnam.

In 2021, Family Medical Practice received an investment from VinaCapital, a leading investment firm in Vietnam, to support the growth of its home healthcare services.

Healthcare Policies and Regulatory Landscape

- Licensing: Companies providing home healthcare services in Vietnam must obtain a license from the Ministry of Health

- Quality standards: The Ministry of Health sets quality standards for home healthcare services, which must be met by all providers

- Insurance coverage: The government has implemented policies to increase insurance coverage for home healthcare services in Vietnam

- Reimbursement policies: Reimbursement policies for home healthcare services are regulated by the government to ensure that patients have access to these services

- Tax incentives: The government provides tax incentives for companies operating in the home healthcare sector to encourage the growth of the market

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Home Healthcare Market Segmentation

By Device Type (Revenue, USD Billion):

Based on the Device Type the market is segmented into Testing, Screening, Monitoring Devices, Therapeutic Home Healthcare Devices, and Mobility Assist.

- Testing, Screening, and Monitoring Device

- Blood Glucose Monitors

- Blood Glucose Monitors

- Blood Pressure Monitors

- Heart Rate Monitors

- Temperature Monitors

- Sleep Apnea Monitors

- Coagulation Monitors

- Ovulation and Pregnancy Test Kits

- Pulse Oximeters

- Home Hemoglobin A1C Test Kit

- Therapeutic Home Healthcare Devices

- Oxygen Delivery Systems

- Nebulizers

- Ventilators

- Sleep Apnea Therapeutic Devices

- Wound Care Products

- IV Equipment

- Dialysis Equipment

- Insulin Delivery Devices

- Inhalers

- ?Other Therapeutic Products (ostomy devices, automated external defibrillators (AEDs)

- Mobility Assist

- Walkers and Rollators

- Wheelchairs

- Canes

- Crutches

- ?Mobility Scooters

By Service Type (Revenue, USD Billion):

- Skilled Nursing Services

- Rehabilitation Therapy Services

- Hospice and Palliative Care Services

- Unskilled Care Services

- Respiratory Therapy Services

- Infusion Therapy Services

- Pregnancy Care Services?

By Indication Type (Revenue, USD Billion):

- Cardiovascular Disorders & Hypertension

- Diabetes

- Respiratory Diseases

- Pregnancy

- Mobility Disorders

- Hearing Disorders

- Cancer

- Wound Care

- ?Other Indications (sleep disorders, kidney disorders, neurovascular diseases, and HIV)

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

Canada Point Of Care Ultrasound Market Analysis

Healthcare Services

Norway Women Health Diagnostic Market Analysis

Healthcare Services

France Interventional Radiology Market Analysis

Related reports (by geography)

Pharmaceuticals

Vietnam Outpatient Rehabilitation Centers Market Analysis

Pharmaceuticals

Vietnam Liver Diseases Therapeutics Market Analysis

Pharmaceuticals

Vietnam Biosimilar Monoclonal Antibodies Market Analysis

Pharmaceuticals