Pharmaceuticals

Vietnam Dermatological Therapeutics Market Analysis

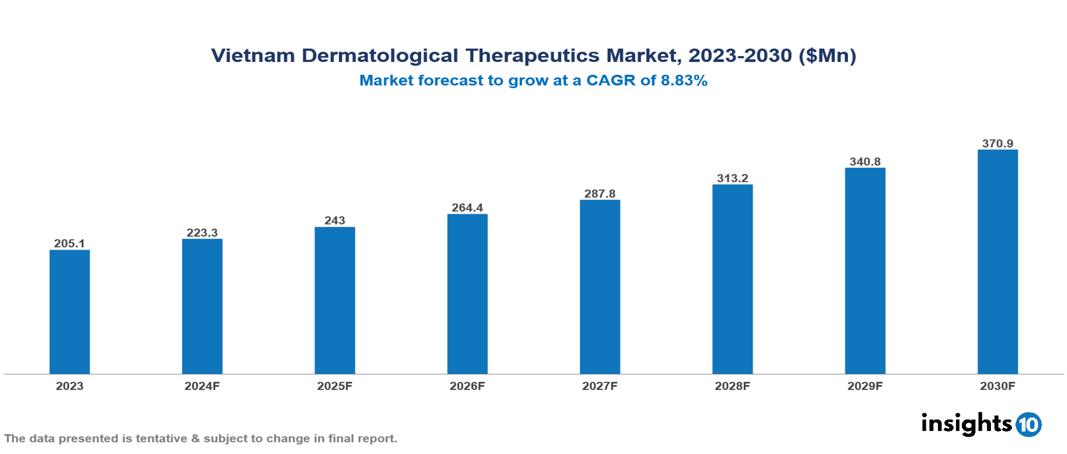

Vietnam Dermatological Therapeutics Market is at around $0.21 Bn in 2023 and is projected to reach $0.37 Bn in 2030, exhibiting a CAGR of 8.83% during the forecast period. Advances in technology, the prevalence of skin disorders, and increased awareness of skin health are driving the expansion of the market. The market is dominated by key players like Almirall SA, Pfizer Inc., GlaxoSmithKline Plc (GSK), AbbVie Inc., Amgen Inc., Novartis AG, Roche, Sanofi, Bayer, and Johnson & Johnson.

Buy Now

Vietnam Dermatological Therapeutics Market Executive Summary

Vietnam Dermatological Therapeutics Market is at around $0.21 Bn in 2023 and is projected to reach $0.37 Bn in 2030, exhibiting a CAGR of 8.83% during the forecast period.

Vietnam Dermatological Therapeutics examines how skincare and treatment approaches are changing in the Vietnamese setting. To address skin health issues in Vietnam, this dynamic area spans a wide spectrum of dermatological disorders and therapeutic techniques, reflecting the junction of medical breakthroughs and cultural considerations.

The market for dermatological therapeutics in Vietnam is expanding steadily, propelled by rising demand for dermatological therapies and growing awareness of skin health. Evolving lifestyles and an increase in skin-related illnesses are important contributing causes. Pharmaceutical businesses from both domestic and foreign markets compete with one another to meet Vietnam's changing needs for dermatological healthcare.

The global market for dermatological treatments generated $40.94 Bn in revenue by 2023, a substantial increase over the previous year. This industry transformation is being driven by low-cost technology and modern production practices. The dynamic combination of accessibility, innovation, and financial help has led to the growth and expansion of the market for dermatological treatments.

GSK is a prominent player in the Vietnamese dermatological medicines industry, with a particular emphasis on treating fungal infections, psoriasis, and acne. In 2022, GSK and Ho Chi Minh City Dermatology Hospital collaborated to initiate a psoriasis awareness campaign to enhance diagnosis and treatment accessibility. With the introduction of PanOxyl in Vietnam, their line of acne treatments is expanded and patient needs are met.

Market Dynamics

Market Growth Drivers:

Increasing Skin Health Awareness: The Vietnamese public's growing understanding of the value of good skincare and the accessibility of dermatological treatments is propelling the market.

Technological Developments: As dermatological treatments and technology are progressing, more patients looking for cutting-edge, efficient treatments for a range of skin problems may become interested.

Prevalence of Skin problems: The need for dermatological therapies is influenced by the population's prevalence of skin problems.

Market Restraints:

Regulatory Obstacles: Strict legal requirements and an extensive approval procedure for novel dermatological products may prevent the industry from expanding. Regulatory obstacles could impede the prompt launch of cutting-edge treatments.

Limited Insurance Coverage: Patients' access to cutting-edge therapy may be impacted by the extent of insurance coverage for dermatological treatments. Inadequate coverage could result in out-of-pocket costs, which would limit the adoption of dermatological therapeutics.

Infrastructure Difficulties: In isolated or rural areas, logistical and distribution issues within the nation may affect the availability of dermatological products.

Healthcare Policies and Regulatory Landscape

All drugs brought into Vietnam require approval from the Ministry of Health (MOH) and the Drug Administration of Vietnam (DAV). To obtain approval from the Drug Administration of Vietnam, the manufacturer (applicant) must submit an application dossier containing all the details and supporting evidence required by the Regulation on Registration of Drugs. Conducting a clinical study can be difficult in Vietnam due to a lack of appropriate facilities and trained investigators, which could delay the clearance procedure.

Competitive Landscape

Key Players:

- Almirall SA

- Pfizer Inc.

- GlaxoSmithKline Plc.

- AbbVie Inc.

- Amgen Inc.

- Novartis AG

- Roche

- Sanofi

- Bayer

- Johnson & Johnson

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Vietnam Dermatological Therapeutics Market Segmentation

By Type

- Prescription-based Drugs

- Over-the-counter Drugs

By Disease

- Alopecia

- Herpes

- Psoriasis

- Rosacea

- Skin Cancer

- Acne

- Atopic Dermatitis

- Vitiligo

- Hidradenitis

- Other Applications

By Drug Class

- Anti-infectives

- Corticosteroids

- Anti-acne

- Calcineurin Inhibitors

- Retinoids

- Other Drug Classes

By Route of Administration

- Topical Administration

- Oral Administration

- Parenteral Administration

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Saudi Arabia Oral Care Market Analysis

Pharmaceuticals

South Africa Type 2 Diabetes Mellitus Drugs Market Analysis

Pharmaceuticals

Global Radiotherapy Market Analysis

Related reports (by geography)

Pharmaceuticals

Vietnam Pharmaceutical Packaging Market Analysis

Pharmaceuticals

Vietnam Tetanus Toxoid Vaccine Market Analysis

Healthcare Services

Vietnam Dental Care Market Analysis

Pharmaceuticals