Medical Devices

Vietnam Bariatric Surgery Devices Market Analysis

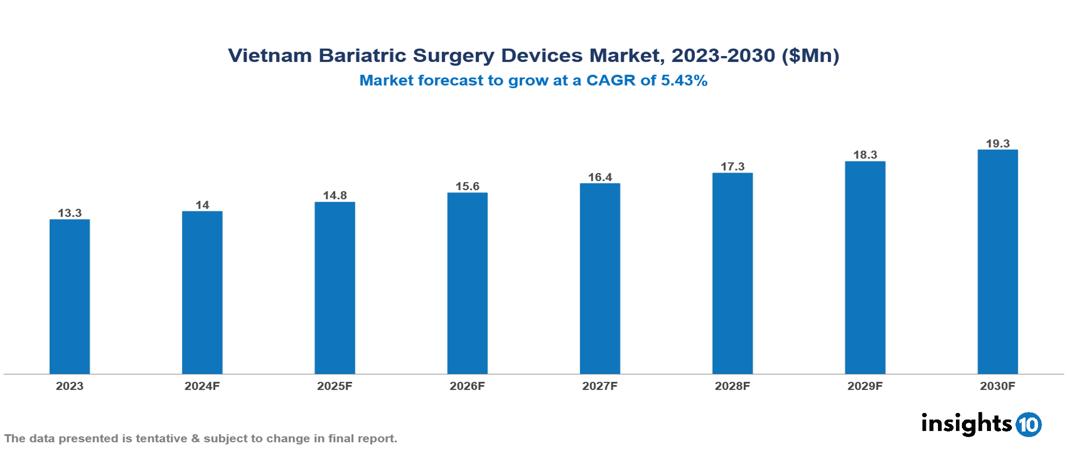

The Vietnam Bariatric Surgery Devices Market was valued at $13.3 Mn in 2023 and is projected to grow at a CAGR of 5.43% from 2023 to 2023, to $19.3 Mn by 2030. Major factors driving the market for bariatric surgical devices include the rising incidence of adult obesity brought on by altered lifestyle patterns and excessive calorie consumption. The demand for bariatric operations is also anticipated to rise over the forecast period due to increased government backing and growing public awareness of the market's unhealthy food and beverage offerings and how they affect BMI, thus driving the market growth of the Bariatric Surgery Devices. The prominent players in the market are Medtronic, B. Braun, Asenus Surgical, Johnson & Johnson, Cousin Surgery among others.

Buy Now

Vietnam Bariatric Surgery Devices Market Executive Summary

The Vietnam Bariatric Surgery Devices Market is at around $13.3 Mn in 2023 and is projected to reach $19.3 Mn in 2030, exhibiting a CAGR of 5.43% during the forecast period 2023-2030.

Gastric bypass and other types of weight-loss surgery, also called bariatric or metabolic surgery, this involve making changes to your digestive system to help you lose weight. Bariatric surgery is done when diet and exercise haven't worked or when you have serious health problems because of your weight. Some weight-loss procedures limit how much you can eat. Others work by reducing the body's ability to absorb fat and calories. Some procedures do both. While bariatric surgery can offer many benefits, all forms of weight-loss surgery are major procedures that can pose risks and side effects. Also, you must make permanent healthy changes to your diet and get regular exercise to help ensure the long-term success of bariatric surgery. Bariatric surgery is done to help you lose extra weight and reduce your risk of possibly life-threatening weight-related health problems, including: certain cancers, including breast, endometrial and prostate cancer, heart disease and stroke, high blood pressure, high cholesterol levels, Non-alcoholic fatty liver disease (NAFLD) or non-alcoholic steatohepatitis (NASH), sleep apnoea, type 2 diabetes etc.

According to Global Obesity Observatory 2023 the prevalence of obesity in Vietnam is around 1.97% among the adults. According to a report by UNICEF, the prevalence of overweight among infants and children under the age of 5 years was 7.4%. Amongst children and adolescents aged 5-19 years, the prevalence of overweight was 19.0% and the prevalence of obesity was 8.1%. Therefore, the market is driven by various factors such as increasing demand for minimally invasive surgeries, rising incidence of obesity, technological advancements, rising awareness about bariatric surgery.

The prominent players in the market are Medtronic, B. Braun, Asenus Surgical, Johnson & Johnson, Cousin Surgery among others.

Market Dynamics

Market Drivers

Rising obesity rates in Vietnam: According to Global Obesity Observatory 2023 the prevalence of obesity in Vietnam is around 1.97% among the adults. The increasing prevalence of obesity in Vietnam is a significant driver. As lifestyle changes lead to higher obesity rates, the demand for bariatric surgeries and associated medical devices rises.

Improved Quality of Life Post-Surgery: Many patients experience significant health improvements and quality of life enhancements after bariatric surgery, which motivates others to seek similar interventions. Thus, enhancing the market growth rate.

Increase in Disposable Income: In 2024, Vietnam's GDP grew by 6.42%, with a notable 6.93% growth in the second quarter. As the economic situation improves, more individuals can afford bariatric surgery, leading to increased demand for related medical devices.

Market Restraints

Limited Coverage: A substantial number of health insurance policies in Vietnam exclude bariatric surgery from their coverage. This means that individuals seeking this type of surgery often have to bear the full cost out of pocket, which can be prohibitively expensive.

Postoperative problems: Like any major surgery, bariatric procedures carry risks such as infection, bleeding, and adverse reactions to anaesthesia. Long-term complications like nutritional deficiencies and dumping syndrome can also occur. These risks may deter some patients from pursuing surgical options.

Absence of Skilled Professionals: The availability of operations and the equipment needed for them may be restricted by a lack of specialist healthcare professionals trained in bariatric surgery.

Regulatory Landscape and Reimbursement Scenario

Vietnam Food and Drug Administration (VFDA), which is part of the Ministry of Health. The VFDA is responsible for ensuring the safety, quality, and efficacy of medical devices used in the country. Bariatric surgery devices are classified based on their risk level, with most falling into Class B (low-moderate risk) or Class C (moderate-high risk). The classification determines the regulatory requirements for approval. Registration and Approval; Manufacturers or importers must register their devices with the VFDA and obtain marketing approval before they can be sold in Vietnam. This process involves submitting documentation on the device's design, manufacturing, and clinical performance.

The reimbursement landscape for bariatric surgery in Vietnam is evolving, with a mix of public and private coverage options. Vietnam's public health insurance scheme, known as Vietnam Social Security (VSS), covers some bariatric surgery procedures, but coverage is limited. Many private health insurance plans in Vietnam offer coverage for bariatric surgery, but the extent of coverage varies by insurer and policy. Factors like BMI thresholds, previous weight loss attempts, and the presence of obesity-related conditions impact coverage decisions.

Competitive Landscape

Key Players

Here are some of the major key players in the Vietnam Bariatric Surgery Devices Market:

- Medtronic plc.

- Ethicon, Inc. (Johnson & Johnson)

- Asenus Surgical US, Inc.

- B Braun Melsungen AG

- Cousin Surgery

- Olympus Corporation

- Richard Wolf GmbH

- SPATZ FIGA, Inc.

- Teleflex Incorporated

- USGI Medical, Inc.

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Vietnam Bariatric Surgery Devices Market Segmentation

By Products

- Minimally invasive surgical devices

- Stapling Devices

- Vessel-sealing devices

- Suturing devices

- Others

- Non-invasive surgical devices

By Procedure

- Sleeve gastrectomy

- Gastric bypass

- Revision bariatric surgery

- Non-invasive bariatric surgery

- Adjustable gastric banding

- Others

End Users

- Hospitals

- Ambulatory surgical centers

- Specialty Clinics

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

Germany Hemodialysis Vascular Grafts Market Analysis

Medical Devices

Kenya ENT Devices Market Analysis

Medical Devices

Mexico Cardiac Pacemakers Market Analysis

Related reports (by geography)

Healthcare Services

Vietnam Women Health Diagnostic Market Analysis

Pharmaceuticals

Vietnam Transdermal Skin Patches Market Analysis

Pharmaceuticals

Vietnam Infectious Wound Care Management Market Analysis

Pharmaceuticals