Medical Devices

US Hemodialysis Equipment Market Analysis

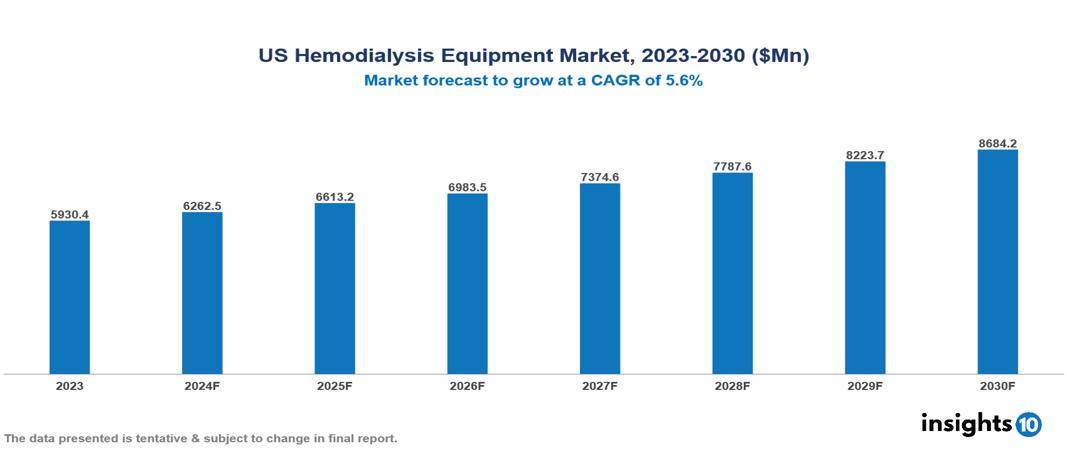

The US Hemodialysis Equipment Market was valued at $5930.4 Mn in 2023 and is projected to grow at a CAGR of 5.6% from 2023 to 2023, to $8684.2 Mn by 2030. The key drivers of this industry are increasing incidence of chronic kidney disease (CKD) and end-stage renal disease (ESRD), availability of advanced dialysis machines and consumables, government initiatives to improve dialysis accessibility, growing adoption of home haemodialysis, expansion of dialysis service providers which has contributed to market growth. The industry is primarily dominated by players such as Stryker, GE HealthCare, Baxter, B. Braun SE, Fresenius Medical Care AG, Medtronic among others.

Buy Now

US Hemodialysis Equipment Market Executive Summary

The US Hemodialysis Equipment Market is at around $5930.4 Mn in 2023 and is projected to reach $8684.2 Mn in 2030, exhibiting a CAGR of 5.6% during the forecast period 2023-2030.

Hemodialysis is a critical treatment for patients with end-stage renal disease, and it relies on specialized medical devices to function effectively. The main components of a haemodialysis machine include the dialyzer (artificial kidney), blood pump, dialysate pump, air detector, heparin pump, temperature monitor, and conductivity monitor.

The dialyzer is a filter that removes waste and excess fluid from the blood. The blood pump pulls blood from the body into the dialyzer, while the dialysate pump sends a special fluid into the dialyzer to help remove the waste and fluid. The air detector monitors for air bubbles in the blood line and stops the blood pump if air is detected to prevent air embolism. The heparin pump delivers an anticoagulant into the blood to prevent clotting during the dialysis process. The temperature monitor ensures the dialysate remains within a safe temperature range, and the conductivity monitor checks the concentration of electrolytes in the dialysate. These various components work together as part of the hemodialysis machine to filter the patient's blood, maintain the proper fluid and electrolyte balance, and prevent complications. Advancements in dialysis technology have helped improve the safety and efficacy of this life-saving treatment.

The number of Americans suffering from kidney failure reached 785,883 in 2019, with 554,038 individuals undergoing dialysis. The increasing prevalence of chronic conditions like diabetes and hypertension, which are major risk factors for chronic kidney disease. The hemodialysis market is driven by significant factors like aging population, increase prevalence rate of chronic diseases, increasing incidence of chronic kidney disease (CKD) and end-stage renal disease (ESRD), availability of advanced dialysis machines and consumables, government initiatives to improve dialysis accessibility, growing adoption of home haemodialysis, expansion of dialysis service providers which has contributed to market growth.

Some of the major players operating in the US Hemodialysis Equipment Market are GE HealthCare, Baxter, B. Braun SE, Fresenius Medical Care AG, Medtronic, Stryker among others.

Market Dynamics

Market Drivers

Rising Prevalence of Chronic Kidney Disease: The number of Americans suffering from kidney failure reached 785,883 in 2019, with 554,038 individuals undergoing dialysis. The increasing prevalence of chronic conditions like diabetes and hypertension, which are major risk factors for chronic kidney disease, is driving the demand for hemodialysis treatments.

Aging Population: The US population is aging, with the number of adults aged 65 and older projected to reach 94.7 Mn by 2060. The risk of chronic kidney disease increases with age, leading to higher demand for dialysis treatments in the elderly population.

Adoption of Telehealth-based Dialysis Treatments: Regulations like the Bipartisan Budget Act in the US have enabled increased adoption of telehealth-based dialysis treatments, allowing patients to receive care remotely. This has expanded access to dialysis services, especially for patients in rural or underserved areas.

Restraints

High Cost of Dialysis Treatments: The average cost of hemodialysis in the US is around $90,000 per patient per year. The high cost of treatment can limit access to dialysis for patients without adequate insurance coverage or financial resources.

Lack of Healthcare Infrastructure: Many regions in the US lack adequate healthcare infrastructure to support dialysis treatments, particularly in rural areas. Limited availability of dialysis centers and qualified healthcare professionals can restrict access to care.

Product Recalls: There have been several product recalls in the dialysis market due to health hazards and regulatory non-compliance issues. This has eroded patient and provider confidence, hindering market growth.

Regulatory Landscape and Reimbursement Scenario

In the US, regulation and reimbursement of hemodialysis medical devices operate under a complex system involving multiple federal agencies and private insurers. The Food and Drug Administration (FDA) is the primary regulatory body for medical devices, including hemodialysis equipment. The FDA classifies these devices, typically as Class II or III, requiring premarket notification (510(k)) or premarket approval (PMA) before they can be marketed. Manufacturers must comply with Quality System Regulations and conduct post-market surveillance.

Reimbursement for hemodialysis services primarily comes through Medicare, as most patients with end-stage renal disease (ESRD) qualify for Medicare coverage regardless of age. The Centers for Medicare & Medicaid Services (CMS) oversees this process, using a bundled payment system for dialysis services that includes equipment, supplies, and certain medications. Private insurance may provide coverage for those not eligible for Medicare or to supplement Medicare coverage. Some states offer additional coverage through Medicaid for low-income patients.

The Department of Veterans Affairs provides coverage for eligible veterans. Home hemodialysis is increasingly supported, with Medicare covering equipment and supplies, though there may be out-of-pocket costs. Dialysis centres receive funding through a combination of government reimbursement and private insurance payments. This system aims to ensure access to necessary hemodialysis treatment while maintaining device safety and efficacy standards.

Competitive Landscape

Key Players

Here are some of the major key players in the US Hemodialysis Equipment Market:

- GE HealthCare

- Stryker

- Medtronic

- Boston Scientific

- Philips

- Siemens Healthineers

- Fresenius Medical Care

- Baxter International

- B. Braun

- Nipro Corporation

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

US Hemodialysis Equipment Market Segmentation

By Hemodialysis Type

- Conventional Hemodialysis

- Short Daily Hemodialysis

- Nocturnal Hemodialysis

By Product & Services

- Equipment

- Consumables

- Dialysis Drugs

- Services

By End Use

- Home-based

- Hospital-based

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

Senegal Medical Devices Market Analysis

Medical Devices

Libya Medical Devices Market Analysis

Medical Devices

Singapore Cardiac Pacemakers Market Analysis

Related reports (by geography)

Pharmaceuticals

US Inhalation Anesthesia Market Analysis

Medical Devices

US Hemodialysis Vascular Grafts Market Analysis

Healthcare Services