Medical Devices

US Diabetes Devices Market Analysis

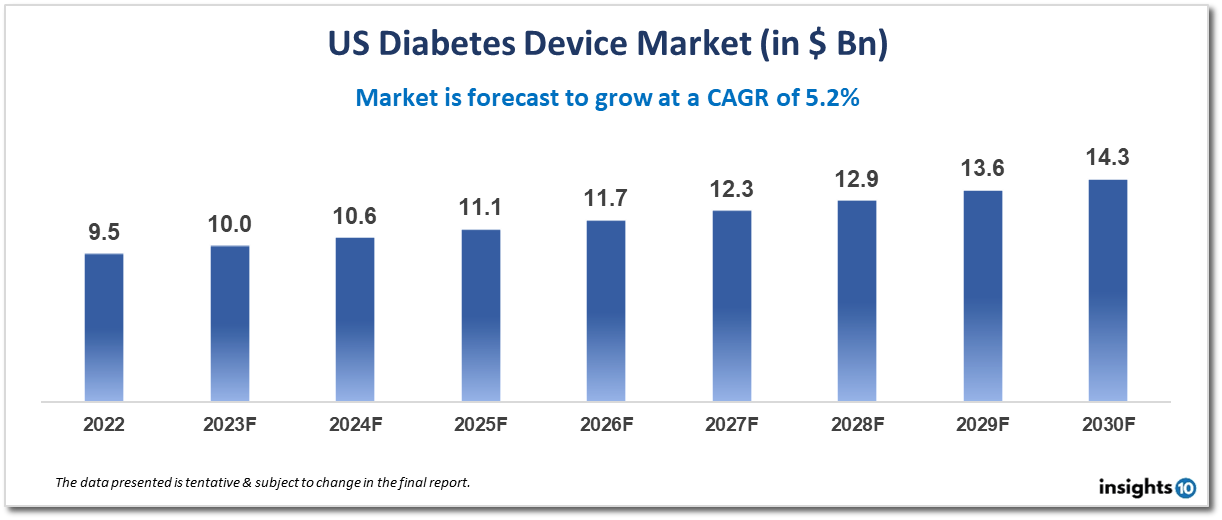

The US diabetes devices market is projected to grow from $4.7 Bn in 2022 to $5.9 Bn by 2030, registering a CAGR of 2.75% during the forecast period of 2022-30. Some of the key trends in the US diabetes devices market include the development of more advanced glucose monitoring and insulin delivery technologies, the use of digital health platforms and apps to help patients manage their diabetes, and the shift towards value-based care models that prioritize patient outcomes and cost-effectiveness. The US diabetes devices market is highly competitive, with several major players dominating the market. Some of the key players in the market include Abbott Laboratories, Medtronic, Dexcom, Roche, and Insulet Corporation.

Buy Now

US Diabetes Devices Market Executive Summary

According to projections, the US Diabetes Devices Market would increase from $4.7 billion in 2022 to $5.9 billion in 2030, exhibiting a CAGR of 2.75% from 2022 to 2030.

A variety of medical devices are used for the treatment of diabetes, and the US diabetes devices industry is a sizable and expanding business. In order to avoid long-term problems including heart disease, renal disease, and nerve damage, diabetes is a chronic condition that affects how the body processes blood sugar (glucose).

Here are some essential details about the US market for diabetes devices:

- The US market for diabetic devices consists of a number of product categories, including glucose monitoring tools (such as blood glucose metres and continuous glucose monitors), insulin administration tools (such as insulin pumps and pens), and other tools for managing diabetes (such as insulin syringes and jet injectors).

- Important players: The US market for diabetic devices is quite competitive, with a few key firms controlling the industry. Abbott Laboratories, Medtronic, Dexcom, Roche, and Insulet Corporation are a few of the market's major participants.

- The development of more sophisticated glucose monitoring and insulin delivery technologies, the use of digital health platforms and apps to assist patients in managing their diabetes, and the shift to value-based care models that place a higher priority on patient outcomes and cost-effectiveness are just a few of the key trends in the US diabetes devices market.

- The Food and Drug Administration (FDA), which establishes safety and efficacy criteria for diabetic devices and oversees their post-market performance via surveillance and enforcement actions, is in charge of regulating the diabetes devices industry in the US.

Overall, the US diabetes devices market is a dynamic and developing industry that is being influenced by medical and technological advancements, shifting patient needs, and shifting laws and regulations in the healthcare industry. The need for cutting-edge and efficient diabetic devices is projected to grow as the prevalence of the disease rises, opening up potential for both new and established market competitors.

Market Dynamics

Growth Drivers

- Increased prevalence of diabetes: The rising incidence of diabetes in the US is a major market driver for diabetes devices. Almost 34 million Americans have diabetes, and the number is predicted to keep rising due to factors including the ageing population, sedentary lifestyles, and bad diets, according to the Centers for Disease Control and Prevention (CDC).

- Technical developments: The US diabetes devices market is expanding as a result of the creation of novel and cutting-edge diabetic devices such continuous glucose monitors (CGMs) and closed-loop insulin delivery systems. For diabetic patients, these technologies provide higher convenience, accuracy, and safety, increasing market demand and acceptance.

- Growing awareness and education: The US market for diabetic devices is expanding as a result of greater knowledge of and education about the treatment of diabetes. Advanced glucose monitoring and insulin administration devices are getting more and more popular as patients and healthcare professionals become more aware of their advantages.

- Initiatives from the government: The US government has started a number of programmes to enhance diabetes management and lessen the strain that diabetes puts on the healthcare system. The US diabetes devices industry is expanding as a result of measures like Medicare coverage for CGMs and campaigns to prevent diabetes.

Competitive Landscape

Key Players

The US diabetes devices market is highly competitive and includes several key players. Some of the major players in this market include:

- Medtronic: Medtronic is a global medical technology company that develops and manufactures a range of products, including insulin pumps, continuous glucose monitoring systems, and other diabetes management devices.

- Abbott Laboratories: Abbott Laboratories is a diversified healthcare company that offers a range of products and services, including diabetes care products such as glucose monitoring systems, test strips, and other related devices.

- Roche Diabetes Care: Roche Diabetes Care is a division of Roche, a global healthcare company that offers a range of products and services, including blood glucose monitoring systems and insulin delivery devices.

- Dexcom: Dexcom is a medical device company that specializes in continuous glucose monitoring systems for people with diabetes.

- Johnson & Johnson

- Insulet Corporation

- Tandem Diabetes Care:

- Ascensia Diabetes Care

- Senseonics

- Novo Nordisk

Healthcare Policies and Regulatory Landscape

The US diabetes devices market is regulated by several healthcare policies and regulatory bodies, including:

- Food and Drug Administration (FDA): The FDA is responsible for regulating medical devices in the US, including diabetes management devices. Diabetes devices must meet strict standards for safety and effectiveness before they can be approved for use.

- Centers for Medicare and Medicaid Services (CMS): The CMS is a federal agency that oversees the Medicare and Medicaid programs. Medicare provides coverage for diabetes devices for eligible beneficiaries, while Medicaid coverage varies by state.

- Affordable Care Act (ACA): The ACA includes provisions that aim to improve access to diabetes care and management, such as requiring insurance plans to cover preventive services for diabetes without cost-sharing.

- American Diabetes Association (ADA): The ADA is a nonprofit organization that advocates for people with diabetes and provides resources and education on diabetes management. The ADA also works to shape healthcare policies and regulations related to diabetes care.

- National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK): The NIDDK is a research organization that focuses on improving the understanding and treatment of diabetes and related conditions.

These healthcare policies and regulatory bodies play a critical role in ensuring the safety and effectiveness of diabetes devices, as well as improving access to diabetes care for people in the US. As the diabetes device market continues to evolve, these policies and regulations will likely continue to adapt to meet the needs of patients and healthcare providers.

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Diabetes Devices Market Segmentation

By Type (Revenue, USD Billion):

The market is divided into blood glucose monitoring systems, insulin delivery systems, and mobile applications for managing diabetes within the type segment. Due to its convenience, ease of use, and usefulness in providing patients and healthcare professionals with real-time insights regarding diabetic conditions for integrated diabetes management, the segment for diabetes management mobile applications is anticipated to grow at the highest rate during the forecast period. Bare-metal Stents

- Blood glucose monitoring systems

- Self-monitoring blood glucose monitoring systems

- Continuous glucose monitoring systems

- Test strips/Test papers

- Lancets/Lancing Devices

- Insulin delivery Devices

- Insulin pumps

- Insulin pens

- Insulin syringes and needles

- Diabetes management mobile applications

By End User (Revenue, USD Billion):

The diabetes market is divided into hospitals & specialty clinics and self & home care, based on the end user.

- Hospitals & Specialty Clinics

- Self & Home Care

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

Ecuador Contraceptive Devices Market Analysis

Medical Devices

Tanzania Cardiac Surgery Instruments Market Analysis

Medical Devices

Mexico Hemodialysis Equipment Market Analysis

Related reports (by geography)

Rare Diseases

US Sickle Cell Disease Drugs Market Analysis

Pharmaceuticals

US Interactive Wound Dressing Market Analysis

Healthcare Services