Pharmaceuticals

US Conjunctivitis Therapeutics Market Analysis

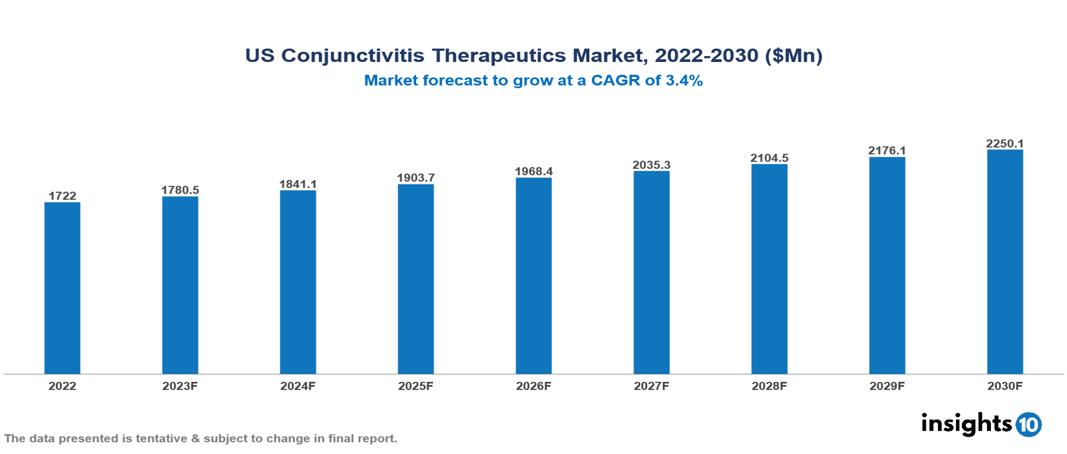

The US Conjunctivitis Therapeutics Market was valued at $1.722 Bn in 2022 and is predicted to grow at a CAGR of 3.4% from 2023 to 2030, to $2.250 Bn by 2030. The key drivers of this industry include the rising prevalence of conjunctivitis, increasing healthcare expenditure, and technological advancements in the therapeutics industry. The industry is primarily dominated by players such as Allergan, Pfizer, Novartis, Santen, IBA Vision, Alembic, and Bausch & Lomb among others.

Buy Now

US Conjunctivitis Therapeutics Market Analysis Executive Summary

The US Conjunctivitis Therapeutics Market is at around $1.722 Bn in 2022 and is projected to reach $2.250 Bn in 2030, exhibiting a CAGR of 3.4% during the forecast period.

Conjunctivitis, commonly known as pink eye, is the inflammation of the conjunctiva, a transparent membrane covering the eye's surface and the inner surface of the eyelid. This condition can arise from various factors, including viral or bacterial infections, allergic reactions, irritants, and exposure to chemicals. Symptoms of conjunctivitis encompass redness, irritation, excessive tearing, and, in some cases, a gritty sensation or the presence of mucous discharge. Diagnosis typically involves a comprehensive eye examination, and the appropriate treatment depends on the underlying cause. Allergic conjunctivitis may be managed with nonsteroidal anti-inflammatory medications, antihistamines, or topical steroid eye drops. Conversely, infectious conjunctivitis, particularly the bacterial form, is commonly treated with antibiotic eye drops or ointments. Companies such as Pfizer, Sanofi, Alcon, and Allergan are among those producing these treatment options, offering effective relief for dry eye and ocular allergy symptoms.

Bacterial Conjunctivitis affects around 135/10,000 Americans every year. These estimates are aggravated by increased risk factors like increased antibiotic resistance, use of contact lenses, and others. The market expansion is driven by several factors such as the rising prevalence of conjunctivitis, increasing healthcare expenditure, and technological advancements in the therapeutics industry. However, conditions such as limited treatment options, availability of generic alternatives, and complex regulatory environment limit the growth and potential of the market.

Market Dynamics

Market Growth Drivers

Increasing prevalence of conjunctivitis: Infectious conjunctivitis is highly prevalent in the US affecting roughly 3% of the population. Bacterial conjunctivitis has an estimated incidence of 135/10,000 individuals. This trend is anticipated to generate a heightened demand for antihistamine eye drops and other treatments. With the aging of the US population, there is an increased susceptibility to age-related eye conditions like dry eye, creating an opportunity for the market in dry eye therapies and lubricants. Additionally, the widespread use of contact lenses, which may cause eye irritation and elevate the risk of infection, is projected to drive the market for contact lens solutions and other preventative measures.

Technological advancements: The advancement of novel delivery systems such as nanoparticles, liposomes, and sustained-release formulations have the potential to enhance the effectiveness of medications, minimize side effects, and improve patient adherence, thereby possibly increasing market penetration. Exploring targeted therapies that specifically address inflammatory pathways or pathogens responsible for conjunctivitis through research could result in more efficient and personalized treatment choices, attracting a broader patient base and fostering market expansion. The enhancement of diagnostic tools, such as tear analysis and point-of-care tests, has the capability to facilitate quicker and more precise diagnoses, enabling early intervention and potentially elevating the demand for therapeutic solutions in the US market.

Increasing healthcare expenditure: The general rise in healthcare spending in the US offers additional resources for the diagnosis and treatment of conjunctivitis, potentially resulting in increased demand for therapeutic solutions. If insurance coverage for eye care services expands, it has the potential to enhance accessibility to both diagnosis and treatment, thereby boosting the utilization of conjunctivitis therapeutics.

Market Restraints

Limited treatment options: Viral conjunctivitis, the predominant form of the condition, usually resolves spontaneously, necessitating only supportive measures like cool compresses and artificial tears. This diminishes the demand for therapeutic interventions. At present, there are no effective antiviral medications designed specifically for treating conjunctivitis. This limitation hinders the growth of the market for this type when compared to bacterial or allergic conjunctivitis, which can be addressed with targeted medications.

Complex regulatory environment: The stringent regulatory framework governing drug approval in the US can result in prolonged and costly development processes for new conjunctivitis therapeutics. This delay in market entry and the associated increased costs can pose challenges for manufacturers. The rigorous environment may deter investment in research and development, potentially restricting the introduction of innovative treatments.

Availability of generics: The availability of generic drugs designed to address mild conjunctivitis symptoms exerts a downward influence on prices and market share for prescription medications. Over-the-counter (OTC) eye drops and artificial tears provide cost-effective choices for self-treatment, diminishing the demand for prescription drugs in cases of mild severity.

Notable Updates

December 2023, Lupin Ltd announced that it has obtained approval from the U.S. health regulatory authority FDA to sell its generic version of Loteprednol Etabonate ophthalmic suspension. This product is designed for the temporary relief of seasonal allergic conjunctivitis.

February 2023, Aldeyra Therapeutics, Inc. has reported that the U.S. Food and Drug Administration (FDA) has approved the New Drug Application (NDA) for topical ocular reproxalap. This investigational new drug candidate, a first-in-class, is intended for treating the signs and symptoms associated with dry eye disease.

October 2021, Biopharmaceutical company Ocular Therapeutix, Inc. disclosed that the U.S. Food and Drug Administration (FDA) has granted approval for its Supplemental New Drug Application (sNDA). This approval aims to expand the label of DEXTENZA, adding a new indication for the treatment of ocular itching linked with allergic conjunctivitis.

Healthcare Policies and Regulatory Landscape

The primary regulatory body overseeing therapeutic products in the US is the Food and Drug Administration (FDA). The FDA's responsibility is to guarantee the safety and effectiveness of drugs, biologics, and medical devices before they are released to the public. The agency adheres to a meticulous and standardized evaluation process, scrutinizing data provided by pharmaceutical and biotechnology companies to assess if a product meets the requisite standards for approval.

Companies seeking licensure for therapeutics in the U.S. typically undergo a multi-phase process, including trials. Upon positive outcomes and demonstrated safety in these trials, the company submits a New Drug Application (NDA) or Biologics License Application (BLA) to the FDA.

The regulatory landscape for new entrants is demanding, characterized by high standards set by the FDA, necessitating substantial investments in research, development, and compliance. However, this stringent process is deliberately implemented to ensure that only safe and effective therapeutics reach the market, upholding public health and fostering confidence in the industry.

Competitive Landscape

Key Players

- Allergan

- Novartis

- Sanofi

- Pfizer

- Alembic Pharmaceuticals

- Bausch & Lomb

- Johnson & Johnson

- Sirion Therapeutics

- IBA Vision Ophthalmics

- Santen Pharmaceutical

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Conjunctivitis Therapeutics Market Segmentation

By Drug Class

- Antibiotics

- Antiviral

- Antiallergic

- Others

By Treatment

- Mast Cell Stabilizers

- Decongestant

- Immunotherapy

- Antihistamines

- Non-steroidal anti-inflammatory drugs

- Olopatadine

- Epinastine

- Others

By Disease Type

- Bacterial

- Chemical

- Viral

- Allergic

By Formulation

- Ointment

- Drops

- Drugs

By End Users

- Hospitals and clinics

- Online Pharmacies

- Retail Pharmacies

- Drug Stores

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

South Africa Cell Based Immunotherapy Market Analysis

Pharmaceuticals

Spain PEGylated Proteins Market Analysis

Pharmaceuticals

France Photorejuvenation Market Analysis

Related reports (by geography)

Pharmaceuticals

US Alopecia (Hair Loss) Therapeutics Market Analysis

Rare Diseases

US Neuroendocrine Tumor Therapeutics Market Analysis

Pharmaceuticals

US Polycystic Kidney Disease (APDKD) Market Analysis

Healthcare Services