Pharmaceuticals

US Cancer Immunotherapy Market Analysis

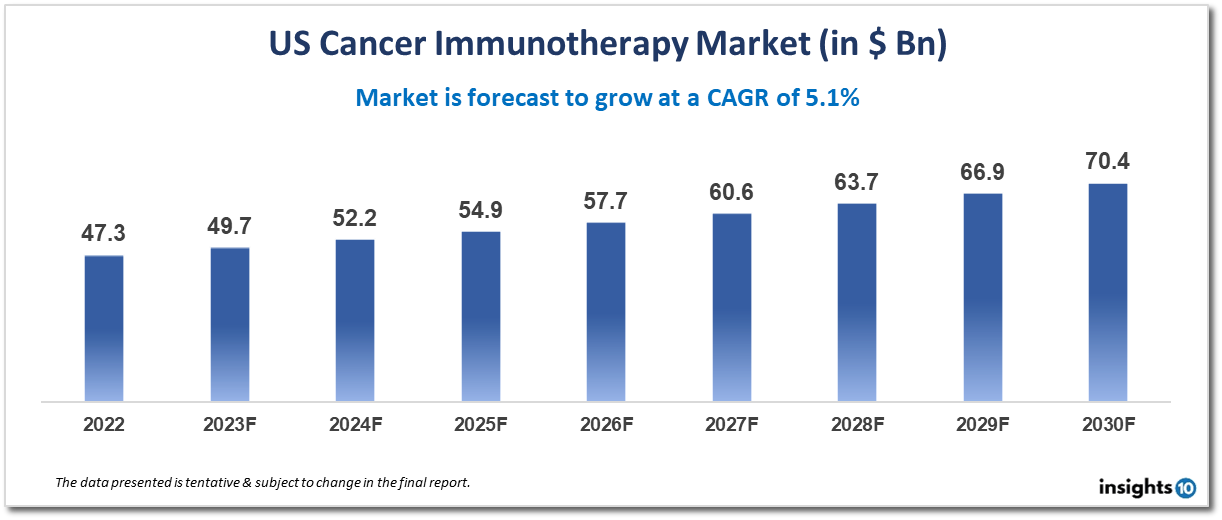

US's cancer immunotherapy market is projected to grow from $47.3 Bn in 2022 to $70.4 Bn by 2030, registering a CAGR of 5.1% during the forecast period of 2022-30. Cancer is a leading cause of death worldwide, and its prevalence is increasing due to factors such as an aging population and changing lifestyles. This has led to a growing demand for effective cancer treatments, including immunotherapies. Key players in the market include Bristol-Myers Squibb, Merck & Co., Inc., Novartis International AG, Roche Holding AG, AstraZeneca plc, Amgen Inc., and others.

Buy Now

US Cancer Immunotherapy Executive Summary

US's cancer immunotherapy market is projected to grow from $47.3 Bn in 2022 to $70.4 Bn by 2030, registering a CAGR of 5.1% during the forecast period of 2022-30.

The US cancer immunotherapy market is a quickly expanding area of the healthcare sector that is dedicated to creating cancer medicines that employ the immune system to combat the disease. Cancer immunotherapy treatments, which can be used alone or in conjunction with other cancer therapies like chemotherapy or radiation, function by triggering the immune system to detect and target cancer cells.

The market is fueled by elements including the rising incidence of cancer, technological and scientific developments, and the rising desire for tailored cancer therapies.

Bristol-Myers Squibb, Merck & Co., Inc., Novartis International AG, Roche Holding AG, AstraZeneca plc, Amgen Inc., and others are significant market participants in the US cancer immunotherapy industry. These businesses invest substantially in clinical trials to introduce cutting-edge treatments to the market while aggressively working to create cancer immunotherapies.

The most widely used cancer immunotherapy therapies are:

- Checkpoint inhibitors

- CAR-T cell therapy

- Cancer vaccines, and

- Immune system modulators

Concerning the treatment of many cancer types, such as melanoma, lung cancer, lymphoma, and others, these procedures have shown encouraging outcomes.

Overall, the US cancer immunotherapy market is a vibrant, quickly expanding sector with huge potential to improve the quality of life for cancer patients and expand the range of available cancer treatments.

Market Dynamics

Market Growth Drivers

- An ageing population and changing lifestyles are two factors contributing to the rising prevalence of cancer, which is a leading cause of mortality globally. As a result, there is an increasing need for efficient cancer therapeutics, such as immunotherapies.

- Improvements in science and technology: Checkpoint inhibitors, CAR-T cell therapy, and cancer vaccines are just a few of the cutting-edge cancer immunotherapies that have been created as a result of technological and scientific advancements. Clinical trials for these treatments have yielded encouraging results, spurring further funding and interest in the area.

- Customized cancer therapies are in greater demand because they are more effective and are more closely matched to a patient's unique genetic profile and disease kind. Many patients find immunotherapies to be an appealing therapy choice since they may be tailored to a patient's particular needs.

- Substantial support from regulatory bodies: The FDA, for example, has given cancer immunotherapy research its full backing and has authorised a number of immunotherapies for use in the treatment of cancer. New immunotherapies have been developed and approved more quickly because of this support.

- Collaboration amongst industry players is expanding as they work together to create and test novel immunotherapies. These partnerships have aided in quickening the development of innovative therapies and their introduction to the market.

Overall, these factors are boosting the US market for cancer immunotherapy and are anticipated to do so for some time to come.

Competitive Landscape

Key Players

The US market for cancer immunotherapy is quite competitive, and there are numerous major manufacturers. The following are some of the major market participants:

- With multiple licenced immunotherapy medications, including Opdivo and Yervoy, Bristol-Myers Squibb is a market leader in cancer immunotherapy

- Merck & Co.: With multiple licenced immunotherapy medications, including Keytruda, Merck & Co. is a significant player in the cancer immunotherapy business

- Roche: Roche is a significant player in the cancer immunotherapy business. Tecentriq and Avastin are only two of the company's authorised immunotherapy medications

- AstraZeneca: With numerous licenced immunotherapy medications, such as Imfinzi and Lynparza, AstraZeneca is a significant player in the cancer immunotherapy business

- Novartis: With numerous licenced immunotherapy medications, such as Kymriah and Cosentyx, Novartis is a significant player in the cancer immunotherapy business

With multiple licenced immunotherapy medications, including Yescarta, Gilead Sciences is a key competitor in the cancer immunotherapy business.

Overall, these prominent companies are propelling the growth and innovation in the US cancer immunotherapy market, along with other market participants.

Healthcare Policies and Regulatory Landscape

Many healthcare regulations and laws apply to the US cancer immunotherapy sector. The US Food and Drug Administration (FDA), which is in charge of assessing the efficacy and safety of novel cancer immunotherapy medications and treatments, controls the market's regulatory environment. The FDA also controls the production, promotion, and labelling of goods used in cancer immunotherapy.

The following are a few of the major healthcare laws and guidelines that affect the US cancer immunotherapy market:

- FDA approval procedure: Before being marketed and sold in the US, cancer immunotherapy treatments must pass a stringent FDA clearance procedure. Clinical trials to assess the goods' efficacy and safety are a part of this procedure, as well as expert FDA assessment.

- Medicare benefits: Certain cancer immunotherapy therapies are covered by Medicare, the government-run health insurance programme for the elderly and those with disabilities. The acceptance and use of immunotherapy therapies, however, may be impacted by the coverage guidelines and reimbursement rates for these procedures.

- Healthcare Act of 2010: The Affordable Care Act (ACA), sometimes referred to as Obamacare, contains regulations that have an effect on the market for cancer immunotherapy, such as the mandate that insurance plans cover cancer screenings and treatments.

- FDA post-market surveillance: The FDA keeps an eye out for any negative side effects or potential safety issues after approving and putting cancer immunotherapy medicines on the market.

The overall goal of these healthcare regulations and policies is to guarantee the efficacy and safety of cancer immunotherapy products and to facilitate patient access to these therapies. To remain compliant and competitive in the market, industry participants must stay up to speed on these rules and regulations, which are always changing.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

US Cancer Immunotherapy Segmentation

By Type (Revenue, USD Billion):

- Monoclonal Antibodies

- Cancer Vaccines

- Checkpoint Inhibitors

- Immunomodulators

- PD-1/PD-L1

- CTLA-4

By Application (Revenue, USD Billion):

- Lung Cancer

- Breast Cancer

- Head and Neck Cancer

- Prostate Cancer

- Colorectal Cancer

- Melanoma

- Others

By End User (Revenue, USD Billion):

- Hospitals

- Clinics

- Ambulatory Surgical Centers (ASCs)

- Cancer Research Centers

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Hong Kong Antiviral Drugs Market Analysis

Pharmaceuticals

UK Medical Cannabis Drugs Market Analysis

Pharmaceuticals

Malaysia pH Meters Market Analysis

Related reports (by geography)

Pharmaceuticals

US Type 2 Diabetes Mellitus Drugs Market Analysis

Pharmaceuticals

US Sarcoma Drugs Market Analysis

Healthcare Services

US Palliative Care Market Analysis

Rare Diseases