Medical Devices

UK MRI Market Analysis

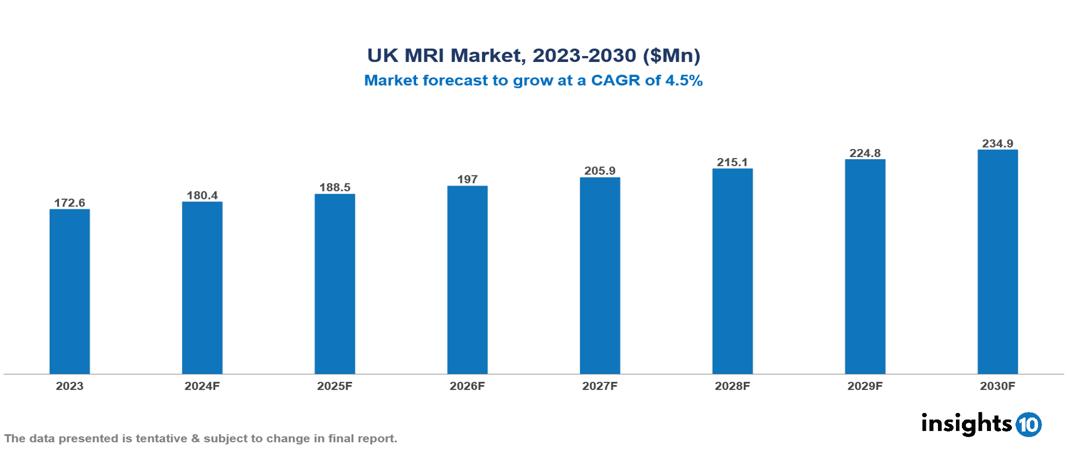

The UK MRI Market was valued at $172.64 Mn in 2023 and is predicted to grow at a CAGR of 4.5% from 2023 to 2030, to $234.94 Mn by 2030. The key drivers of this industry include increasing prevalence of chronic diseases, rise in healthcare expenditure, and increasing awareness for early and accurate diagnosis. The key players in the industry are GE Healthcare, Philips Healthcare, Siemens Healthineers, and Vista Health among others.

Buy Now

UK MRI Market Executive Summary

The UK MRI Market is at around $172.64 Mn in 2023 and is projected to reach $234.94 Mn in 2030, exhibiting a CAGR of 4.5% during the forecast period.

Magnetic resonance imaging (MRI) is a type of diagnostic test that can create detailed images of nearly every structure and organ inside the body. It uses strong magnetic fields and radio waves to produce detailed images of the inside of the body. The MRI machine is a large, cylindrical (tube-shaped) device that generates a powerful magnetic field around the patient and emits pulses of radio waves from a scanner. Some MRI machines resemble narrow tunnels, while others are more spacious. The intense magnetic field produced by the MRI scanner causes the atoms in your body to align in the same direction. Subsequently, radio waves are emitted from the MRI machine, which disrupt this alignment, causing the atoms to return to their original positions. As the radio waves cease, the atoms revert to their initial alignment and emit radio signals. These signals are then picked up by a computer, which transforms them into an image of the area being examined. This image is displayed on a viewing monitor.

UK has 6.1 MRI systems per Mn people. The market therefore is driven by significant factors like increasing prevalence of chronic diseases, rise in healthcare expenditure, and increasing awareness for early and accurate diagnosis. However, high cost, limited accessibility, and patient suitability restrict the market's growth.

The leading pharmaceutical companies include Siemens Healthineers and GE Healthcare for MRI machines. Canon Medical Systems Corporation, Hitachi, and United Imaging are also significant contributors to the MRI market, with continuous research and development activities.

Market Dynamics

Market Growth Drivers

Rising Prevalence of Chronic Diseases: A growing number of people in the UK are living with chronic diseases like cardiovascular diseases, cancer, neurological disorders, and musculoskeletal conditions. Approximately 3 Mn people in the UK are living with cancer, breast cancer and prostate cancer being the most common ones. These conditions often require MRI scans for accurate diagnosis and treatment planning, increasing demand for MRI services.

Increasing Awareness of Early Diagnosis: There is growing awareness about early diagnosis and treatment of diseases like tuberculosis is driving demand for diagnostic imaging like MRI. Initiatives like the "TB Alert" program are also focused on ensuring quick diagnosis and treatment of conditions like tuberculosis, boosting the need for diagnostic imaging technologies like MRI.

Increasing Healthcare Expenditure: UK's total healthcare expenditure reached £269 billion, with the share of GDP related to healthcare rising to 12.8%. This increased healthcare spending has been a major driver for the MRI market, as it has enabled greater investment in MRI machines and infrastructure. The National Health Service (NHS) in the UK performs over 4 Mn MRI scans annually, and the government-funded Medical Research Council has heavily invested in imaging research centers and networks across the country.

Market Restraints

High Cost of MRI: MRI machines are expensive, with the cost of 1.5T MRI systems ranging from $1-2 Mn, and high-field (3T) MRI systems costing around $2.5-5 Mn. The high cost of equipment and procedures limits the adoption of MRI technology among end users with constrained budgets.

Limited Accessibility: MRI scanners are primarily located in hospitals and specialized diagnostic centers, which can be a significant barrier for patients living in remote areas or those with limited mobility. This geographic concentration of MRI services can restrict access and lead to longer wait times.

Patient Suitability: MRI scans may not be appropriate for all individuals, which restricts their use due to factors like claustrophobia, as well as discomfort for patients with metal implants, heart pacemakers, or metal chips/clips near the eyes. These situations may result in patients feeling anxious, declining to proceed with the procedure, and ultimately impeding the growth of the MRI market in the UK.

Regulatory Landscape and Reimbursement Scenario

The Medicines and Healthcare Products Regulatory Agency (MHRA) is the responsible regulatory body that oversees the approval and use of MRI systems and related medical devices in the UK. It also sets standards and guidelines for the installation, operation, and maintenance of MRI equipment to minimize risks and ensure patient safety.

The NHS, which provides universal healthcare coverage in the UK, is the primary payer for MRI services. However, the reimbursement rates and policies for MRI scans within the NHS can vary depending on factors such as the clinical indication, the type of MRI scanner used, and the healthcare setting. Some private health insurance plans in the UK may cover the cost of MRI scans performed outside the NHS. However, coverage details and limitations will vary depending on the specific plan.

Competitive Landscape

Key Players

Here are some of the major key players in the UK MRI Market:

- GE Healthcare

- Canon Medical Systems Corporation

- Siemens Healthineers

- Philips Healthcare

- Hitachi

- Medserena Upright MRI

- United Imaging

- Vista Health

- Pro Scan Imaging

- Esaote

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

UK MRI Market Segmentation

By Architecture

- Closed MRI Systems

- Open MRI Systems

By Field Strength

- Low Field MRI Systems

- High Field MRI Systems

- Ultra-High Field MRI Systems

By Application

- Neurology

- Musculoskeletal

- Cardiovascular

- Oncology

- Others ( Abdominal, Pediatric)

By End-User

- Hospitals and Clinics

- Diagnostic Imaging Centers

- Research Institutes

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

Indonesia Biomaterials in Healthcare Market Analysis

Medical Devices

Saudi Arabia Medical Devices Market Analysis

Medical Devices

Canada Bio-implant Market Analysis

Related reports (by geography)

Pharmaceuticals

UK Topical Drugs Delivery Market Analysis

Rare Diseases

UK Hodgkin Lymphoma Therapeutics Market Analysis

Rare Diseases