Pharmaceuticals

UK Atopic Dermatitis Therapeutics Market Analysis

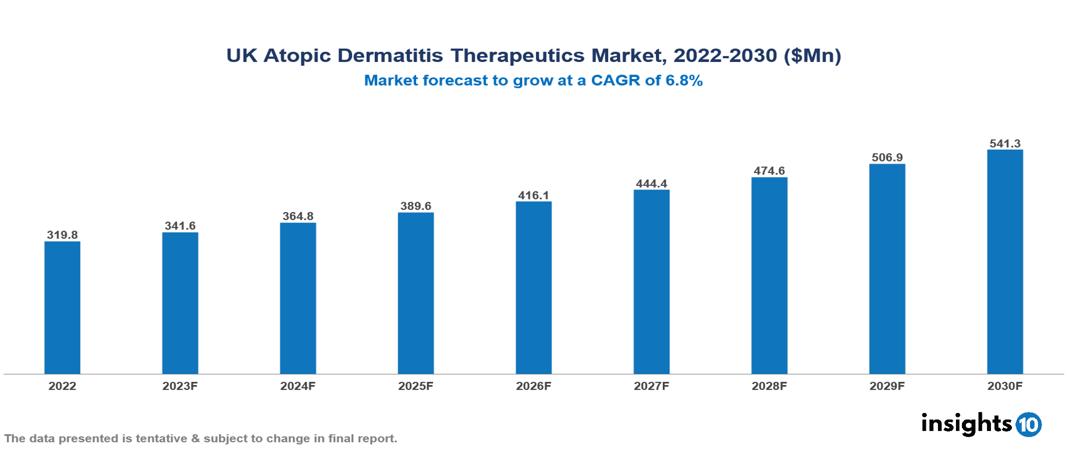

The UK Atopic Dermatitis Therapeutics Market was valued at US $320 Mn in 2022, and is predicted to grow at (CAGR) of 6.8% from 2023 to 2030, to US $541 Mn by 2030. The key drivers of this industry include the rising prevalence of Atopic Dermatitis (AD), evolving treatment landscape of the industry, and high medical unmet needs and diagnoses. The industry is primarily dominated by players such as Pfizer, Astellas, Novartis, Galderma, AbbVie, Anacor, Meda, and Allergan, among others.

Buy Now

UK Atopic Dermatitis Therapeutics Market Analysis: Executive Summary

The UK Atopic Dermatitis Therapeutics Market is at around US $320 Mn in 2022 and is projected to reach US $541 Mn in 2030, exhibiting a CAGR of 6.8% during the forecast period.

Atopic dermatitis (AD), commonly known as eczema, is a persistent inflammatory skin condition characterized by redness, itching, and inflammation. It often manifests in localized patches across various body areas and can be exacerbated by factors such as dry skin, stress, and exposure to specific irritants or allergens. Prominent symptoms include intense itching, redness, dryness, and the appearance of small, fluid-filled blisters that may release fluid and form crusts. Treatment typically involves a holistic approach, incorporating the use of emollients for skin moisturization, topical corticosteroids to alleviate inflammation, and, in severe cases, systemic immunosuppressants. Several pharmaceutical companies manufacture medications for atopic dermatitis, with notable examples including Regeneron Pharmaceuticals and Sanofi's Dupixent (Dupilumab), Pfizer's Eucrisa (Crisaborole), and Novartis's Elidel (Pimecrolimus).

Currently, more than 72,000 individuals are living with AD in the UK. The estimated prevalence ranges up to 20% for children and 10% for adults. The market is driven by significant factors such as the rising prevalence of AD, high unmet medical needs, and the evolving treatment landscape in the therapeutics market. However, conditions such as affordability challenges, complex reimbursement policies, and increased competition limit the growth and potential of the market.

Market Dynamics

Market Growth Drivers

Increase in prevalence of AD: In the United Kingdom, the estimated prevalence of AD ranges from 11–20% for children and 5–10% for adults. Currently, approximately 72,000 individuals are suffering from AD. The rising prevalence is linked to environmental factors, the hygiene hypothesis, and advancements in diagnostic methods.

High unmet medical need: Owing to the huge patient pool, the majority of atopic dermatitis treatments take place within the home environment, involving minimal interaction with healthcare providers or services. This indicated the high unmet medical need of the UK population for advanced treatments, driving the therapeutics market forward.

Evolving treatment landscape: In the UK market, there is a transition towards biologics such as dupilumab (Dupixent) and secukinumab (Cosentyx), providing targeted effectiveness and enhancing the quality of life for patients. The emergence of JAK inhibitors like abrocitinib (Cetrolizumab) and baricitinib (Olumiant) presents another encouraging category of treatment.

Market Restraints

Affordability challenges: New biologic therapies provide heightened effectiveness but come with a high cost, which may hinder access for patients and put pressure on healthcare budgets. Disparities in healthcare coverage and socioeconomic differences can lead to unequal access to advanced treatments, especially for underprivileged communities.

Stringent reimbursement policies: The National Health Service (NHS) enforces stringent criteria for medication reimbursement, necessitating proof of cost-effectiveness before endorsing therapies. This protocol can impede market entry for innovative yet costly treatments. The sluggish approval procedure and the possibility of coverage restrictions may limit patients' access to newer, potentially more efficient alternatives.

Increased competition: The presence of generic alternatives for topical corticosteroids and calcineurin inhibitors exerts significant pricing pressure on the market. While this enhances affordability for certain patients, it has the potential to diminish profits for pharmaceutical companies and discourage investment in research and development for new therapies. Striking a balance between promoting generics for cost-effectiveness and fostering innovation through patent protection is crucial for ensuring sustainable growth in the market.

Notable Updates

September 2021, Pfizer's CIBINQO obtained marketing authorization in the UK for the treatment of moderate to severe atopic dermatitis in adults and adolescents aged 12 years and older.

Healthcare Policies and Regulatory Landscape

The healthcare regulatory landscape in the United Kingdom is overseen by several agencies and organizations to ensure the safety, efficacy, and quality of healthcare products and services. One of the key authorities in the pharmaceutical sector is the Medicines and Healthcare Products Regulatory Agency (MHRA). The MHRA is responsible for regulating medicines, medical devices, and blood components for transfusion in the UK. It assesses the safety and quality of drugs before they can be authorized for use, monitors their safety once on the market, and ensures compliance with regulatory standards.

Obtaining a license for pharmaceutical products in the UK involves a rigorous evaluation process conducted by the MHRA. Applicants must submit comprehensive data on the safety, efficacy, and quality of their products, and the MHRA conducts thorough assessments before granting marketing authorization. The regulatory environment aims to strike a balance between ensuring patient safety and facilitating innovation in the pharmaceutical industry.

New entrants must navigate complex regulatory procedures, adhere to stringent quality standards, and demonstrate the benefits of their products to gain approval in the UK market. The regulatory framework is designed to safeguard public health while fostering an environment conducive to the development and introduction of innovative healthcare solutions.

Competitive Landscape

Key Players

- Pfizer

- Novartis

- Astellas Pharma

- Galderma

- Regeneron Pharmaceutical

- Sanofi

- Valeant Pharmaceutical

- Anacor Pharmaceutical

- Meda Pharmaceutical

- Allergan Plc

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

UK Atopic Dermatitis Therapeutics Market Segmentation

By Drug Class

- Corticosteroids

- Calcineurin Inhibitors

- Immunosuppressants

- Biologic Therapy

- PDE-4 Inhibitor

- Antibiotics

- Antihistamines

- Emollients

By Route of Administration

- Topic

- Oral

- Injectable

By Severity type

- Mild

- Moderate

- Severe

By Age Group

- 18 years and below

- 19 years and above

By Distribution channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

- Dermatology Clinics

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

France Liver Diseases Therapeutics Market Analysis

Pharmaceuticals

Indonesia Gram-Negative Infection Therapeutics Market Analysis

Pharmaceuticals

Saudi Arabia Dry Eye Medication Market Analysis

Related reports (by geography)

Pharmaceuticals

UK Generic and Biosimilar Pharmaceutical Market Analysis

Rare Diseases

UK Acute Myeloid Leukemia Market Analysis

Healthcare Services

UK GMP Testing Service Market Analysis

Digital Health