Pharmaceuticals

UK Adult Malignant Glioma Therapeutics Market Analysis

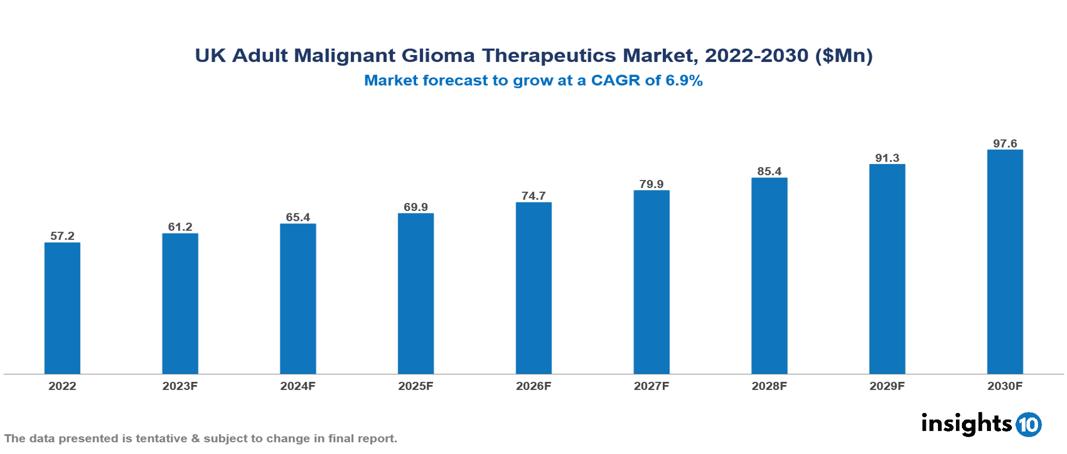

The UK Adult Glioma Therapeutics Market is valued at around $57 Mn in 2022 and is projected to reach $98 Mn by 2030, exhibiting a CAGR of 6.9% during the forecast period. A powerful convergence of factors is driving the UK Adult Malignant Glioma Therapeutics Market, including an increasing glioma burden, an aging population, a focus on customized therapy, and active research and development initiatives, both by the government and other market players. Key players in the UK Adult Malignant Glioma Therapeutics Market include companies like Merck & Co., Bristol-Myers Squibb, Roche, AbbVie, Azurity Pharmaceuticals, Aptevo Therapeutics, Peptinib Ltd., Bio-Rad Laboratories, Novocure, Pfizer etc.

Buy Now

UK Adult Malignant Glioma Therapeutics Market Executive Summary

The UK Adult Glioma Therapeutics Market is valued at around $57 Mn in 2022 and is projected to reach $98 Mn by 2030, exhibiting a CAGR of 6.9% during the forecast period.

Malignant glioma is a type of brain cancer that originates from glial cells in the central nervous system. These supporting cells can turn into tumours called gliomas, known for their aggressive nature. The three main types in adults are anaplastic astrocytoma, anaplastic oligodendroglioma, and glioblastoma multiforme (GBM). Treatment typically involves a combination of radiation therapy, chemotherapy, and surgery. Due to their aggressiveness, the prognosis for malignant gliomas is often uncertain, influenced by factors like the patient's age, tumor size and location, and how well the tumor responds to treatment.

The Glioma incidence rates vary across the UK, with greater rates in Northern Ireland and Scotland than in England and Wales. Every year, around 4,300 individuals are diagnosed with Gliomas, with GBM accounting for nearly 60% of cases. This amounts to 12 per 100,000 individuals encountering GBM each year, which is higher than the global standard. It should also be highlighted that by 2030, more than 20% of the UK population will be 65 or older, which will significantly raise the risk of Glioma, given that the average age at diagnosis is 64. The UK Adult Malignant Glioma Therapeutics Market is being driven by a compelling confluence of factors, including an increasing Glioma burden, an aging population, a focus on customized therapy, and active research and development initiatives, both by the government and other market players.

Switzerland-based pharmaceutical company Roche has the biggest market share with Avastin (Bevacizumab), a critical drug used for recurrent GBM& in the UK, while Merck & Co. dominates the first-line treatment market for Glioma& with Temozolomide.

Market Dynamics

Market Growth Drivers

Reimbursement Landscape: While the NHS provides coverage for proven treatments such as Temozolomide and radiation, access to newer, targeted medicines like immunotherapy may be limited by cost and availability. This leaves a void in the market for affordable and accessible treatment choices.

Increased Focus on Research: The UK has a thriving clinical trial environment for glioma treatments, with over 80 studies now underway. This investment in R&D promotes innovation and offers the potential for future breakthroughs. Initiatives such as the 100,000 Genomes Project are opening the road for personalized therapy in glioma, enabling targeted treatments based on specific tumour mutations. This tailored strategy has the potential to enhance treatment results and increase market demand for specialized medications.

Increased Public Awareness: Increased public awareness of cancer and enhanced cancer screening programs result in earlier detection and treatment. The advances in supportive care and palliative therapies enable glioma patients to survive longer and with higher quality of life, resulting in a longer-term need for medicines. These factors act as drivers for market growth.

Market Restraints

Shortage of Staff and Healthcare Workers: The existing lack of numerous healthcare professions, including oncologists, nurses, and specialist technicians, is already limiting the NHS's ability to provide appropriate treatment for cancer patients. With a limited workforce, hospitals may struggle to offer the extensive and specialized care that glioma patients require while undergoing sophisticated therapies such as surgery, radiation, and immunotherapy.

Existing Healthcare Burden: The NHS is already under enormous strain because to an aging population, an increasing chronic illness load, and excessive wait times. Integrating and supporting costly novel glioma treatments such as targeted medicines and immunotherapies in this overburdened system will be difficult and time-consuming. Thus, immediate market expansion cannot be assured.

Psychological Burden of Glioma: Patients with glioma have emotional anguish, cognitive impairments, and a worse quality of life as a result of the disease's aggressiveness and treatment complications. Inadequate access to supportive care services and psychological assistance can have a negative influence on patient well-being and treatment compliance.

Healthcare Policies and Regulatory Landscape

The National Health Service (NHS) of the United Kingdom has developed a variety of regulations and standards to protect patient rights, privacy, and public involvement. The NHS Constitution for England specifies patient, public, and worker rights, as well as the NHS's commitments. It emphasizes the ability to select healthcare providers, access to information, and the NHS's core principles and values. The Medicines and Healthcare Products Regulatory Agency (MHRA), an executive agency of the Department of Health and Social Care in the UK, is responsible for ensuring that pharmaceuticals and medical equipment perform properly and are fairly safe. The MHRA's multiple independent advisory groups provide the UK government with information and suggestions on pharmaceutical and medical device regulation. In the UK, there are many regulatory avenues for medication approval, each with its own set of standards and timescales. While there are expedited options for high-priority pharmaceuticals or public health emergencies, the standard process might take years.

Competitive Landscape

Key Players

- Merck & Co.

- Bristol-Myers Squibb

- Roche

- AbbVie

- Azurity Pharmaceuticals

- Aptevo Therapeutics

- Peptinib Ltd.

- Bio-Rad Laboratories

- Novocure

- Pfizer

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

UK Adult Malignant Glioma Therapeutics Market Segmentation

By Disease Type

- Glioblastoma Multiforme

- Anaplastic Astrocytoma

- Anaplastic Oligodendroglioma

- Anaplastic Oligoastrocytoma

- Other Types

By Treatment Type

- Chemotherapy

- Targeted Drug Therapy

- Radiation Therapy

- Surgery

- Gene Therapy

- Immunotherapy

- Vaccines

By Distribution Channel

- Hospital Pharmacies

- Drug Stores & Retail Pharmacies

- Online Pharmacies

By Disease Stage

- Early-Stage Tumour

- Late-Stage Tumour

- Palliative Care

By Route of Administration

- Oral

- Parenteral

- Others

By End User

- Hospitals

- Speciality Clinics

- Chemotherapy Centres

- Radiotherapy Centres

- Homecare

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

China Medical Imaging Market Analysis

Pharmaceuticals

Brazil Human Rotavirus Vaccine Market Analysis

Pharmaceuticals

Singapore Cold Pain Therapy Market Analysis

Related reports (by geography)

Pharmaceuticals

UK Chronic Pain Therapeutics Market Analysis

Rare Diseases

UK Hypophosphatasia (HPP) Therapeutics Market Analysis

Pharmaceuticals

UK Anti-Venom Market Analysis

Medical Devices