Healthcare Services

UAE Patient Adherence Programs Market Analysis

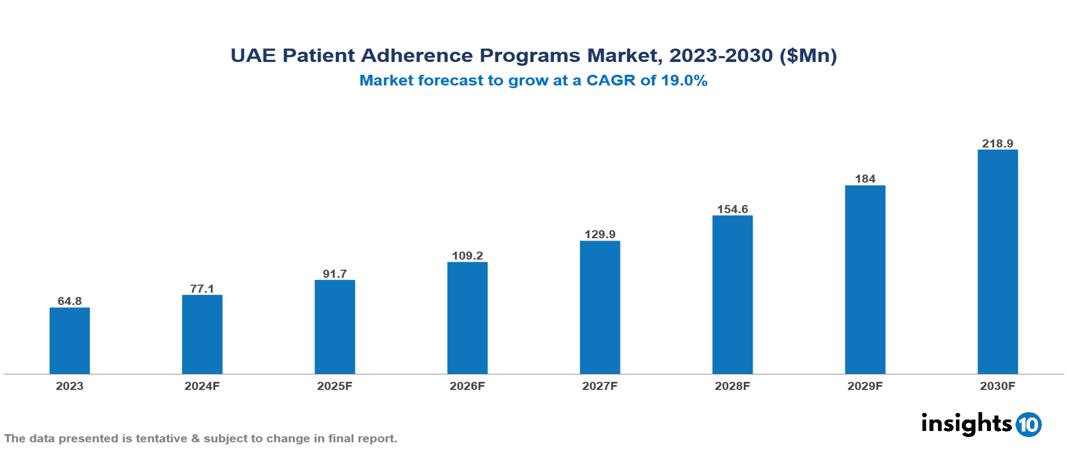

The UAE Patient Adherence Programs Market was valued at $64.8 Mn in 2023 and is predicted to grow at a CAGR of 19% from 2023 to 2030, to $218.9 Mn by 2030. The key drivers of the market include increasing non-adherence, rising chronic conditions, and an aging population. The prominent players in the UAE Patient Adherence Programs Market are Medspero Pharma, Julphar Gulf Pharmaceuticals, Neopharma, Globalpharma, Medpharma, Avernus Pharma, and Lavasta Pharma, among others.

Buy Now

UAE Patient Adherence Programs Market Executive Summary

The UAE Patient Adherence Programs market is at around $64.8 Mn in 2023 and is projected to reach $218.9 Mn in 2030, exhibiting a CAGR of 19% during the forecast period.

A patient adherence program aims to ensure that patients follow prescribed medication regimens to improve treatment outcomes, using both direct and indirect methods to assess adherence. Direct methods include monitoring therapy by measuring drug levels, metabolites, or biological markers in blood or urine, and confirming medication intake. Indirect methods, more commonly used, involve patient self-reports, pill counts, prescription refill rates, clinical response evaluations, and electronic medication monitors. Pill counts compare the number of pills taken between appointments with the prescribed dosage, while patient self-reports collect information through interviews, questionnaires, or diaries. Electronic devices such as pill bottles or blister packs track medication access to provide precise data. A widely used tool for assessing adherence is the Morisky Medication Adherence Scale (MMAS), a validated and reliable questionnaire suitable for clinical use. These approaches help healthcare providers ensure consistent medication use, ultimately enhancing patient health outcomes.

The UAE Patient Adherence Program Market is thus driven by significant factors such as increasing non-adherence, rising chronic conditions, and an aging population. However, inadequate healthcare infrastructure, high implementation costs, and limited accessibility restrict the growth and potential of the market.

The leading players in the UAE Patient Adherence Programs Market are Medspero Pharma, Julphar Gulf Pharmaceuticals, Neopharma, Globalpharma, Medpharma, Avernus Pharma, and Lavasta Pharma, among others.

Market Dynamics

Market Growth Drivers

Increasing non-adherence: According to a study conducted to evaluate patient adherence, 45.6% of patients reported as being non-adherent to anti-hypertensive patients. To overcome the issue of non-compliance in the UAE, patient adherence programs can be implemented which leads to the overall market growth.

Rising Chronic Conditions: According to the MoHAP, cardiovascular disease is the leading cause of NCD deaths, accounting for 34% of all deaths in the country, followed by cancer which constitutes 12%. Chronic diseases such as diabetes, hypertension, and heart disease require ongoing treatment and long-term medication adherence. Patient adherence programs can help during the treatment of chronic conditions which creates a positive effect on the market growth.

Aging Population: The UAE is going through a demographic transition as the number of persons aged 60+ is expected to increase more than six-fold between 2020 and 2050 from about 311,000 (3.1% of the total population) to 2 Mn (19.7%). The elderly population is more prone to risk from chronic diseases and multiple comorbidities, necessitating complex medication regimens that are difficult to manage without structured adherence programs. Adherence programs help with polypharmacy and provide monitoring and support. The aging population is thus a potential pool that can benefit from these programs which increases the market growth.

Market Restraints

Inadequate Healthcare Infrastructure: By restricting access to vital healthcare services and resources required for these programs to be successful, inadequate healthcare infrastructure impedes the expansion of patient adherence initiatives. Patients face challenges in adhering to recommended therapies on a regular basis due to inadequate technology support, a lack of healthcare personnel, and poorly equipped facilities. Furthermore, inadequate infrastructure frequently results in healthcare practitioners' inability to adequately monitor and promote patient adherence, which has a negative impact on patient outcomes and diminishes confidence in these programs. As a result, these obstacles hinder market expansion by discouraging investments and limiting the efficacy and scalability of patient adherence programs.

High Implementation Costs: Establishing advanced technologies like electronic health records (EHRs), mobile health applications, telemedicine platforms, and electronic monitoring devices necessitates significant financial outlays. Additionally, the need to hire specialized personnel, such as IT experts, adherence counselors, and extra healthcare providers, adds to operational expenses. Integrating these new adherence technologies with existing healthcare systems and EHRs can be particularly complex and expensive. Thus, these all expenses related to patient adherence programs can negatively affect the market.

Limited Accessibility: Accessibility issues can hinder the expansion of the patient adherence program market, especially in regions with inadequate healthcare infrastructure. Patients in these areas often encounter obstacles like long travel distances to clinics, a scarcity of healthcare professionals, and limited access to affordable medications and adherence support. Socioeconomic challenges, such as low income and lack of insurance, further impede participation in adherence programs. These barriers reduce enrolment and engagement, thereby restricting the effectiveness and growth potential of these programs.

Regulatory Landscape and Reimbursement Scenario

In UAE, the Ministry of Health and Prevention (MoHAP) is the federal regulatory authority responsible for overseeing the healthcare system. It plays a critical role in safeguarding public health by ensuring the safety, quality, and efficacy of the medicines. In addition to MoHAP, other regulatory bodies that oversee licenses, register different types of products, and create healthcare policies and guidelines for hospitals and pharmacies are the Dubai Health Authority (DHA) and the Health Authority Abu Dhabi (HAAD).

The pharmaceuticals require approval before importing, selling, or marketing in the UAE. Registration of pharmaceutical products is a complex process that requires extensive documentation and several requirements to be fulfilled by the companies. The overall approval process for pharmaceuticals and medical devices involves classification, application submission, review, and potential inspection. Depending on the device’s complexity and the application’s thoroughness, the evaluation procedure may take up to 45 working days.

The UAE’s healthcare reimbursement landscape involves a mix of public and private insurance. In the public sector, Government funds and taxes collected from patients with required insurance are frequently used to reimburse public hospitals and clinics. In the private sector, private insurance providers employ a range of techniques, including Fee-For-Service (FFS) which pays medical professionals according to the services they offer (e.g., consultation, operation); the Diagnosis Related Groups (DRGs) define a set fee for the treatment of a certain illness. Lastly, through Managed Care, individuals with insurance might receive discounted treatments from networks of healthcare providers.

Competitive Landscape

Key Players

Here are some of the major key players in the UAE Patient Adherence Programs Market:

- Medspero Pharma

- Lacasa Pharma

- Qiagen

- Biopharma

- Julphar Gulf Pharmaceuticals

- Neopharma

- Globalpharma

- Medpharma

- Avernus Pharma

- Lavasta Pharma

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

UAE Patient Adherence Programs Market Segmentation

By Type

- Hardware centric

- Software centric

By Medication

- Cardiovascular

- Nervous System

- Diabetes

- Gastrointestinal

- Oncology

- Rheumatology

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

Canada Metabolomics Market Analysis

Healthcare Services

US Biobanks Market Analysis

Healthcare Services

South Africa Medical and Diagnostic Laboratory Service Market Analysis

Related reports (by geography)

Pharmaceuticals

UAE Allergy Therapeutics Market Analysis

Rare Diseases

UAE Rare Hematology Disorders Market Analysis

Pharmaceuticals

UAE Atopic Dermatitis Drugs Market Analysis

Pharmaceuticals