Pharmaceuticals

UAE Oral Care Market Analysis

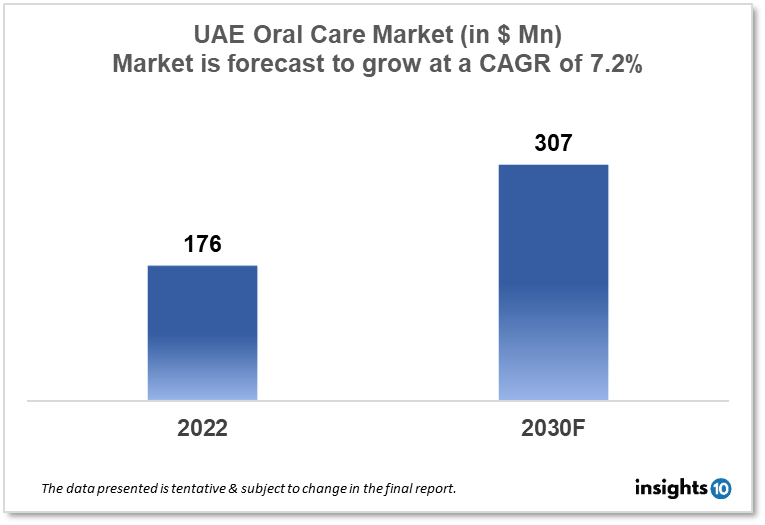

The UAE oral care market was valued at $176 Mn in 2022 and is estimated to expand at a CAGR of 7.2% from 2022 to 2030 and will reach $307 Mn in 2030. One of the main reasons propelling the growth of this market is the introduction of newer technologies, Technological advancements. The market is segmented by type, drug, and distribution channel. Some key players in this market are Dr. Michael's Dental Clinic, Dubai Smile Dental Center, Bin Arab Dental Center, Al Ain Dentistry Perfect, Smile Orthodontic and Cosmetic Dental Center, and The Dental Studio

Buy Now

UAE Oral Care Market Executive Summary

The UAE oral care market was valued at $176 Mn in 2022 and is estimated to expand at a CAGR of 7.2% from 2022 to 2030 and will reach $307 Mn in 2030. The demand for oral care products in the UAE is increasing as people become more conscious of their oral hygiene. The availability of a wide range of oral care products, including toothpaste, mouthwash, dental floss, and teeth whitening products, has contributed to the growth of the market. There has also been an increase in demand for specialized oral care products, such as those for sensitive teeth, gum disease, and halitosis. The UAE has a well-developed private healthcare sector, which dominates the oral care market. Many private dental clinics and hospitals in the UAE offer state-of-the-art facilities and equipment, as well as highly trained and experienced dentists. The cost of dental treatments and procedures in the UAE is generally higher than in other countries, but the quality of care is also generally higher.

Market Dynamics

Market Growth Drivers

The UAE has a rapidly growing population, which is driving demand for oral care services and products. According to the World Bank, the population of the UAE grew by 50% between 2000 and 2020, from 3.6 Mn to 9.9 Mn people. This growth is expected to continue, with the population projected to reach 12.1 Mn by 2050. This increasing population is likely to drive demand for oral care products and services, as more people require dental treatments and services. The UAE has a high per capita income, which is driving demand for premium oral care products and services. According to the World Bank, the gross national income per capita in the UAE was $43,390 in 2020, one of the highest in the world. This high-income level allows consumers to spend more on oral care products and services, including premium products that offer additional benefits such as teeth whitening or sensitivity relief.

The UAE government has been promoting oral health awareness through various initiatives, such as the annual National Oral Health Campaign. This has helped to increase awareness of the importance of oral health among consumers. In a survey conducted by Euromonitor in 2019, 70% of respondents in the UAE reported brushing their teeth twice a day, a sign of the growing awareness of oral hygiene in the country. The UAE oral care market is also being driven by technological advancements, particularly in the area of dental treatments and procedures. For example, the use of 3D printing technology to produce dental implants and orthodontic appliances is becoming increasingly popular in the country, allowing for more precise and efficient dental treatments.

Market Restraints

The UAE oral care market is highly competitive, with multinational and local companies vying for market share. This can make it difficult for new entrants to gain a foothold in the market and may lead to price wars and promotional activities that can erode profit margins. Unlike some other countries, dental insurance coverage is not widespread in the UAE. This can make it difficult for consumers to afford dental treatments and procedures and may limit the growth of the market. While the UAE government has been promoting oral health awareness through various initiatives, there is still a lack of oral health education among some segments of the population. This can lead to poor oral hygiene practices and an increased risk of dental problems. Cultural factors can also pose challenges to the UAE oral care market. For example, traditional remedies and practices may be preferred over Western-style oral care products and services, particularly among older generations or those from more conservative backgrounds.

Competitive Landscape

Key Players

- Dr. Michael's Dental Clinic

- Dubai Smile Dental Center

- Bin Arab Dental Center

- Al Ain Dentistry

- Perfect Smile Orthodontic and Cosmetic Dental Center

- The dental studio

Healthcare Policies and Regulatory Landscape

The Health Authority Abu Dhabi is responsible for regulating and overseeing the healthcare sector in Abu Dhabi. HAAD sets standards for healthcare providers, including dental clinics, and ensures that they comply with regulations related to quality of care, patient safety, and licensing. Dubai Health Authority (DHA) is responsible for regulating and overseeing the healthcare sector in Dubai. DHA sets standards for healthcare providers, including dental clinics, and ensures that they comply with regulations related to quality of care, patient safety, and licensing.

The Ministry of Health and Prevention (MOHAP) is responsible for setting healthcare policies and standards at the federal level in the UAE. MOHAP regulates healthcare providers across the country and is responsible for approving new drugs and medical devices.

The UAE government has launched the National Oral Health Program, which aims to promote oral health awareness and provide access to oral care services for all UAE residents. The program focuses on preventive measures, such as regular dental check-ups and oral health education.

Reimbursement Scenario

In the UAE, dental insurance coverage is not yet widespread, which can make it difficult for patients to afford dental treatments and procedures. However, some employers do offer health insurance plans that include dental coverage, which can help to offset the cost of dental care.

The Dubai Health Authority (DHA) has recently launched a new initiative called the Dubai Dental Outpatient Clinic (DDOC), which aims to provide affordable dental care to UAE residents. The DDOC provides a range of dental services, including preventive care, restorative dentistry, and cosmetic dentistry, at reduced rates. Additionally, some dental clinics in the UAE offer financing options for patients who cannot afford to pay for their treatments up front. These financing options allow patients to pay for their treatments in installments over time, making it easier for them to manage the cost of dental care.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

UAE Oral Care Market Segmentation

By Product Type (Revenue, USD Billion):

- Toothpaste

- Toothbrush

- Mouthwash

- Dental Accessories

- Denture Products

- Others

By Distribution Channel (Revenue, USD Billion):

- Retail Pharmacies

- Online Channels

- Supermarkets

- Dental Dispensaries

By Demographics

- Age (children, adults and geriatric population)

- Gender

- Income

- Education

- Occupation

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

US Axial Spondyloarthritis (axSpA) Market Analysis

Pharmaceuticals

APAC Oncology Drugs Market Analysis

Pharmaceuticals

Italy Obesity Drugs Market Analysis

Related reports (by geography)

Pharmaceuticals

UAE Axial Spondyloarthritis (axSpA) Market Analysis

Pharmaceuticals

UAE Cardiovascular Drugs Market Analysis

Pharmaceuticals

UAE Blood Plasma Market Analysis

Rare Diseases