Pharmaceuticals

UAE Clinical Nutrition for Diabetes Care Market Analysis

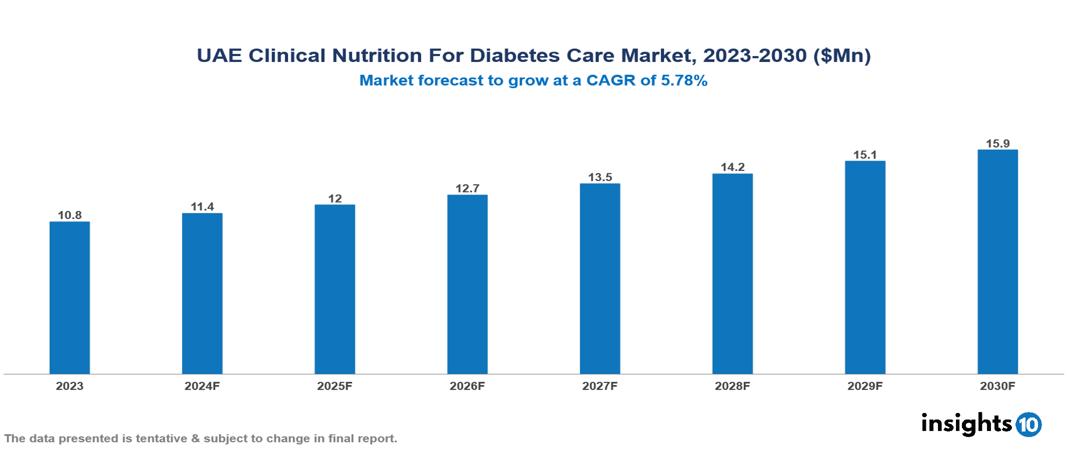

The UAE Clinical Nutrition for Diabetes Care Market was valued at $10.75 Mn in 2023 and is predicted to grow at a CAGR of 5.78% from 2023 to 2030, to $15.93 Mn by 2030. The key drivers of this industry include increasing the prevalence of diabetes, advancements in nutritional science, and initiatives for diabetes management. The key players in the industry are Nestlé Health Science, Eli Lily, Baxter International, Boehringer Ingelheim, and among others.

Buy Now

UAE Clinical Nutrition for Diabetes Care Market Executive Summary

The UAE Clinical Nutrition for Diabetes Care Market is at around $10.75 Mn in 2023 and is projected to reach $15.93 Mn in 2030, exhibiting a CAGR of 5.78% during the forecast period.

Clinical nutrition for diabetes care refers to specialized dietary interventions and nutritional strategies designed to manage and improve the health outcomes of people with diabetes mellitus. It involves using evidence-based nutrition treatment to help diabetic patients maintain blood sugar control, avoid complications, and enhance their overall metabolic health. The primary aim is to optimize nutrition, regulate blood sugar levels, prevent complications, and enhance overall health outcomes for those with diabetes.

The increase in the prevalence of diabetes due to aging, obesity, and unhealthy lifestyles is one of the factors contributing to the growth of the global clinical nutrition market. Obesity is a major factor leading to diabetes. Clinical nutrition including medical foods and parenteral nutrition can help relieve symptoms or slow down the progression of a chronic condition. As the number of people with diabetes continues to grow, so does the demand for these specialized food products. Patients afflicted with diabetes are at higher risk of comorbidities, as diabetes is a major cause of blindness, kidney failure, heart attacks, stroke, and lower limb amputation, as reported by the WHO.

The leading pharmaceutical companies include Boehringer Ingelheim, Sanofi is known for its extensive portfolio of medications, including those essential for diabetes care. Baxter International, Eli Lilly, and Danone Nutricia are also significant contributors to the Clinical Nutrition for Diabetes Care landscape, with continuous research and development activities.

Market Dynamics

Market Growth Drivers

Increasing Prevalence of Diabetes: The UAE has a high prevalence of diabetes, similar to many other countries around the world. This is due in part to a growing aging population, increasing rates of obesity, and unhealthy lifestyles. According to the International Diabetes Federation, about 16.4% of the total adult population is living with diabetes. This large diabetic population drives the demand for specialized clinical nutrition products and services to manage the condition.

Government Initiatives to Improve Healthcare: The UAE government is heavily investing in enhancing the country's healthcare infrastructure and services through initiatives like the Vision 2030 strategy. This includes a focus on reducing lifestyle diseases like diabetes, which boosts the clinical nutrition market. The strategy aims to expand and improve healthcare infrastructure. This includes establishing more specialized diabetic clinics and integrating diabetes management services into existing healthcare centers.

Increasing Focus on Preventative Healthcare: There is a growing emphasis on preventive healthcare in the UAE. This includes a focus on early detection of diabetes and prediabetes, as well as interventions to prevent the onset of the disease. Clinical nutritionists play a key role in preventive healthcare by helping people develop healthy eating habits and make lifestyle changes that can reduce their risk of developing diabetes.

Market Restraints

High Cost of Specialised Products: Specialized diabetic food products and enteral formulas can be significantly more expensive than regular groceries. This can be a burden for low-income individuals and families, limiting access to optimal clinical nutrition support. The high cost of specialized nutritional items and services for diabetic care can increase healthcare expenses, posing an economic burden.

Regulatory Challenge: UAE has rigorous procedures for approving new clinical nutrition products, including specialized diabetic food items and enteral feeding formulas. This can delay the availability of innovative products that could benefit patients. All new clinical nutrition products must undergo a comprehensive registration process. This includes submitting detailed product information, clinical studies, safety data, and manufacturing quality certifications. For specialized diabetic food items, additional evidence of their efficacy in managing diabetes may be required.

Workforce Shortage: Diabetes management through clinical nutrition is relatively a new area of focus compared to traditional dietetics. With fewer qualified dietitians, patients with diabetes might struggle to find appointments or receive the level of personalized attention needed to effectively manage their condition through diet. This could create a bottleneck in service availability.

Regulatory Landscape and Reimbursement Scenario

The Ministry of Health and Prevention (MoHAP) is the primary government body responsible for regulating healthcare products and services in the UAE. It oversees the registration, import, and marketing of clinical nutrition products for diabetes care. All clinical nutrition products, including specialized diabetic food items and enteral feeding formulas, must be registered with the MoHAP before being marketed or sold in the UAE. Products must have clear and accurate labeling, representing the product's contents, nutritional value, and intended use.

UAE government has implemented various healthcare initiatives and programs to improve access to diabetes care, such as the Saada and "Thiqa" programs. These programs likely include some form of reimbursement or coverage for diabetes management. Some private insurance providers in the UAE, such as Sukoon Insurance, offer specialized "Diabetic Care" insurance plans that provide lump-sum payments for major medical events related to diabetes.

Competitive Landscape

Key Players

Here are some of the major key players in the UAE Clinical Nutrition for Diabetes Care Market:

- Abbott Nutrition

- Eli Lilly

- Danone Nutricia

- Nestlé Health Science

- Baxter International

- Boehringer Ingelheim

- Sanofi

- Fresenius Kabi

- Johnson & Johnson

- Novo Nordisk

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

UAE Clinical Nutrition for Diabetes Care Market Segmentation

By Product

- Oral Nutrition

- Parenteral Nutrition

- Enteral Feedback Formulas

By Stage

- Adult

- Paediatric

By Distribution Channel

- Online

- Retail

- Institutional Sales

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

APAC Infectious Disease Therapeutics Market Analysis

Pharmaceuticals

UAE Rheumatoid Arthritis Drugs Market Analysis

Related reports (by geography)

Pharmaceuticals

UAE Hepatitis B Drugs Market Analysis

Pharmaceuticals

UAE Asthma Drugs Market Analysis

OTC & Nutraceuticals

UAE Herbal Supplements Market Report

Pharmaceuticals