Pharmaceuticals

UAE Chronic Obstructive Pulmonary Disease (COPD) Therapeutics Market Analysis

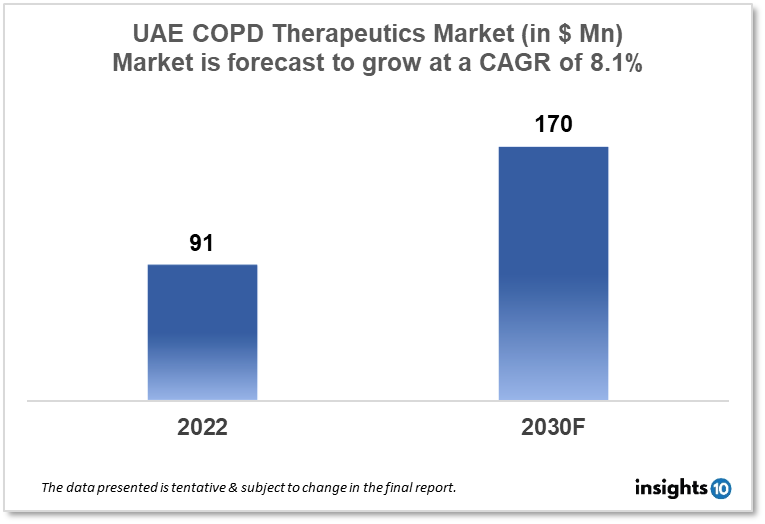

UAE Chronic Obstructive Pulmonary Disease (COPD) therapeutics market was valued at $91 Mn in 2022 and is estimated to expand at a CAGR of 8.1% from 2022-30 and will reach $170 Mn in 2030. One of the main reasons propelling the growth of this market is the increased prevalence rate and government initiative. The market is segmented by Drug class and By distribution channel. Some key players in this market are Julphar, Neopharma,b Global Pharma, Medpharma, Pharmaforte, Abbott Laboratories, Almirall, Astellas Pharma, AstraZeneca, Boehringer Ingelheim Pharmaceuticals, Novartis, Pfizer, Teva Pharmaceuticals and others.

Buy Now

UAE Chronic Obstructive Pulmonary Disease (COPD) Therapeutics Market Executive Summary

UAE Chronic Obstructive Pulmonary Disease (COPD) Therapeutics Market was valued at $91 Mn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 8.1% from 2022-30 and will reach $170 Mn in 2030. Chronic Obstructive Pulmonary Disease (COPD) is defined by the Global Initiative for Chronic Obstructive Lung Disease (GOLD) as "a common preventable and treatable disease characterized by persistent airflow limitation that is usually progressive and associated with an enhanced chronic inflammatory response in the airways and the lung to noxious particles or gases". Globally, COPD is one of the main causes of illness and mortality.

The prevalence of COPD (Chronic Obstructive Pulmonary Disease) in the UAE is estimated to be around 4.2% of the adult population. This prevalence is expected to increase due to factors such as the aging population, smoking habits, and environmental pollution. According to a study conducted in 2019 by the Ministry of Health and Prevention in the UAE, the prevalence of COPD was found to be higher among men than women, with a rate of 5.2% among men and 3.1% among women. The study also found that smoking was the most common risk factor for COPD, with a prevalence of 20.1% among current smokers and 5.5% among ex-smokers. Another study conducted in Dubai in 2017 found that the prevalence of COPD among Emirati nationals was 5.7%, while the prevalence among non-Emirati residents was 3.4%. The study also found that the prevalence of COPD was higher among individuals aged 60 years or above, with a rate of 10.4%.

Market Dynamics

Market Growth Drivers

The prevalence of COPD is increasing in the UAE due to factors such as air pollution, smoking, and an aging population. According to a report by the World Health Organization (WHO), the prevalence of COPD in the UAE is estimated to be around 4.2% of the total population. This increasing prevalence of COPD is a major driver for the growth of the COPD therapeutics market. Combination therapies, which use two or more drugs to treat COPD, are becoming increasingly popular due to their effectiveness in managing COPD symptoms. The combination therapies segment is expected to grow at a CAGR of 9.2% during the forecast period. This growth is driven by the increasing adoption of combination therapies among patients and healthcare providers.

Pharmaceutical companies are investing heavily in research and development to introduce new and innovative treatments for COPD. The introduction of new and innovative treatments is expected to drive the growth of the COPD therapeutics market. The UAE government has launched several initiatives to address the increasing prevalence of COPD in the country. For instance, the Ministry of Health and Prevention has launched a national campaign to raise awareness about the disease and promote early detection and treatment. These initiatives are expected to drive the growth of the COPD therapeutics market in the UAE.

Market Restraints

COPD therapeutics can be expensive, particularly newer and more innovative treatments. This can make it difficult for patients to afford the treatment they need, particularly those without adequate health insurance coverage. Despite the increasing prevalence of COPD in the UAE, awareness and diagnosis rates remain relatively low. Many people with COPD do not realize they have the disease, which can delay treatment and lead to more severe symptoms. Low awareness and diagnosis rates can also make it difficult for pharmaceutical companies to market their products effectively. Some patients with COPD may face limited access to healthcare, particularly in rural or remote areas. This can make it difficult for patients to receive the treatment they need and can limit the growth of the COPD therapeutics market. The regulatory environment in the UAE can be complex, particularly for pharmaceutical companies looking to introduce new products. Obtaining regulatory approval for new products can be a lengthy and expensive process, which can limit the ability of companies to bring new and innovative treatments to market. As patents on some COPD therapeutics expire, generic versions of these drugs become available, which can reduce the market share and revenue of branded products. This can limit the growth of the COPD therapeutics market and reduce the profitability of pharmaceutical companies operating in this space.

Competitive Landscape

Key Players

- Julphar

- Neopharma

- Global pharma

- Medpharma

- Pharmaforte

- Abbott Laboratories

- Almirall,

- Astellas Pharma

- AstraZeneca

- Boehringer Ingelheim Pharmaceuticals

- Novartis

- Pfizer

- Teva Pharmaceuticals

Healthcare Policies and Regulatory Landscape

The healthcare policies and regulatory framework in the UAE aim to ensure that healthcare services and products meet the highest standards of quality and safety. Ministry of Health and Prevention (MOHAP): MOHAP is responsible for regulating and supervising the healthcare sector in the UAE, including the licensing of healthcare professionals and facilities.

Health Authority Abu Dhabi (HAAD) is responsible for regulating and supervising healthcare in the Emirate of Abu Dhabi, including the licensing of healthcare facilities and the accreditation of healthcare professionals.

Dubai Healthcare City (DHCC) is a free zone in Dubai dedicated to healthcare, education, and research. DHCC has its own regulatory framework, including licensing and accreditation requirements for healthcare facilities and professionals.

The UAE government has launched several initiatives to promote health and prevent disease, including campaigns to raise awareness about healthy lifestyles and disease prevention, and programs to promote early detection and treatment of diseases such as COPD. The UAE has a robust regulatory framework for the registration and approval of pharmaceutical products, including strict requirements for quality and safety, and the regulation of pharmaceutical pricing to ensure affordability and accessibility.

Reimbursement Scenario

The UAE government provides free or heavily subsidized healthcare services to UAE nationals and residents through its national health insurance program, the Abu Dhabi National Insurance Company (ADNIC), and the Dubai Health Authority's (DHA) mandatory health insurance scheme. Public insurance plans typically cover a portion of the cost of medications, and some plans may have specific restrictions or requirements for coverage, such as prior authorization or step therapy requirements. Patients with private insurance may also be entitled to coverage for COPD therapeutics, depending on their specific insurance plan. Private insurance plans may have different coverage requirements and restrictions than public insurance plans, and coverage levels may vary depending on the type of insurance plan and the specific medication being prescribed.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

UAE Chronic Obstructive Pulmonary Disease (COPD) Therapeutics Market Segmentation

By Drug Class

Bronchodilators: Bronchodilators are medications that help to relax the muscles around the airways, making it easier to breathe. These can be further classified as short-acting or long-acting bronchodilators.

Corticosteroids: Corticosteroids are anti-inflammatory medications that can help reduce swelling and inflammation in the airways. These can be used alone or in combination with bronchodilators.

Combination therapies: Combination therapies combine bronchodilators and corticosteroids in a single medication. These are often used for patients with more severe COPD.

Phosphodiesterase-4 inhibitors: Phosphodiesterase-4 inhibitors are medications that help to reduce inflammation and improve airflow in the lungs.

Others: Other medications that may be used to treat COPD include mucolytics, oxygen therapy, and vaccines for influenza and pneumococcal disease.

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Tanzania Obesity Drugs Market Analysis

Pharmaceuticals

Ireland Radiotherapy Market Analysis

Pharmaceuticals

Malaysia Medical X-ray Market Analysis

Related reports (by geography)

Rare Diseases

UAE CDKL5 deficiency disorder (CDD) market Analysis

Rare Diseases

UAE Hemophilia B Therapeutics Market Analysis

Rare Diseases

UAE Hyperhidrosis Therapeutics Market Analysis

Pharmaceuticals