Pharmaceuticals

UAE Cholesterol Therapeutics Market Analysis

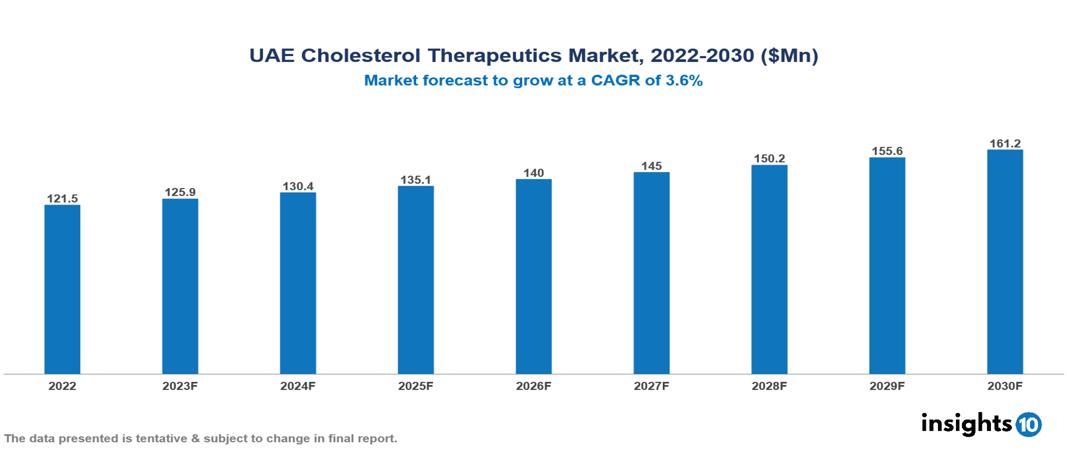

The UAE Cholesterol Therapeutics Market is anticipated to experience a growth from $122 Mn in 2022 to $161 Mn by 2030, with a CAGR of 3.6% during the forecast period of 2022-2030. The key factors propelling the market growth in the UAE include the rising prevalence of dyslipidemia due to factors like urbanization, western dietary patterns, and obesity, increased awareness about the health risks associated with high cholesterol, and significant government investments and initiatives aimed at improving healthcare facilities. The UAE Cholesterol Therapeutics Market encompasses various players across different segments, Amgen, Pfizer, Merck, AstraZeneca, Johnson & Johnson, Julphar, Cadila, Sinopharm, Sanofi, AbbVie, etc., among various others.

Buy Now

UAE Cholesterol Therapeutics Market Analysis Executive Summary

The UAE Cholesterol Therapeutics Market is anticipated to experience a growth from $122 Mn in 2022 to $161 Mn by 2030, with a CAGR of 3.6% during the forecast period of 2022-2030.

Cholesterol is a fatty, waxy molecule that helps create cell membranes, produce hormones, and aid in the digestion of fat-soluble vitamins. It circulates in the blood and is divided into two types: LDL and HDL. LDL, sometimes known as "bad" cholesterol, can cause plaque buildup in arteries, resulting in atherosclerosis and an increased risk of heart disease and stroke. On the other hand, HDL, sometimes known as "good" cholesterol, helps eliminate LDL from the bloodstream, lowering the risk of cardiovascular disease. Elevated LDL cholesterol levels are linked to a variety of disorders, most notably cardiovascular disease, which includes coronary artery disease and peripheral artery disease. These disorders are caused by plaque formation in the arteries, which reduces blood flow and increases the risk of blockages. Traditional therapy methods for high cholesterol include lifestyle changes such as diet, exercise, and smoking cessation. Statins, which suppress cholesterol formation, have been routinely prescribed. Newer therapeutic possibilities include PCSK9 inhibitors, which improve LDL elimination, as well as developing medications that target particular cholesterol metabolic pathways. These innovative therapies provide choices for people who have not responded well to standard approaches or are suffering pharmaceutical side effects, giving a holistic strategy for regulating cholesterol levels and preventing related disorders.

The Arabian Gulf area has a threefold higher frequency of familial hypercholesterolemia (FH) than the rest of the globe. Cardiovascular disease accounts for more than a quarter of all fatalities in the UAE. Hypercholesterolemia is prevalent in the UAE, with rates ranging from 47.2% to 53% among the Arab population.

The key factors propelling the market growth in the UAE include the rising prevalence of dyslipidemia due to factors like urbanization, western dietary patterns, and obesity, increased awareness about the health risks associated with high cholesterol, and significant government investments and initiatives aimed at improving healthcare facilities.

Pfizer has the greatest market share, most likely due to its established presence and popular cholesterol-lowering medications. AstraZeneca is also a big participant, with a strong market share due to well-known medications such as Crestor and Brilinta. Numerous smaller local Gulf enterprises contribute to the lower market share. They mostly supply generic pharmaceuticals or serve as distributors for major brands.

Market Dynamics

Market Growth Drivers

Rising Prevalence of Dyslipidemia: Dyslipidemia, particularly excessive cholesterol, is becoming increasingly common in the UAE population. Contributing factors include increased urbanization, the adoption of Western diets heavy in saturated fats and processed sweets, and a lack of physical activity all contribute to increased cholesterol. Additionally, rising obesity rates in the UAE compound the cholesterol problem. As the population ages, the likelihood of acquiring high cholesterol naturally rises.

Increased Awareness about the Diseases: High cholesterol has been linked to health issues such as heart disease, stroke, and peripheral artery disease, leading to increased awareness and concern in the UAE. This awareness increases demand for preventative measures and treatment choices, hence increasing the market for cholesterol-lowering pharmaceuticals.

Government Investments and Initiatives: The UAE government is investing in enhancing healthcare facilities and ensuring pharmaceutical access. Increased insurance coverage makes cholesterol-lowering drugs more affordable to a larger population. Government measures promote routine health checks and the early detection of dyslipidemia, resulting in prompt treatment and market growth. Investing in local production of generic cholesterol medicines may increase affordability and market accessibility.

Market Restraints

Competitive Market Landscape: The presence of a highly competitive market with several pharmaceutical companies producing cholesterol-lowering drugs might result in pricing pressures. Intense competition may lead to price wars and lower profit margins for businesses, reducing their motivation to spend in R&D for new and novel cholesterol-lowering medications.

Cultural and Lifestyle Factors: Cultural preferences and lifestyle choices can both impact the incidence of high cholesterol in a group. Saturated fat diets and sedentary lifestyles have been linked to elevated cholesterol levels. If there is a lack of attention on healthy living and eating habits, it can lead to an increased prevalence of high cholesterol, making it difficult to regulate and manage with therapeutic measures.

High cost and low adherence: The high cost of pharmaceuticals is another barrier to market expansion in the UAE cholesterol-lowering therapeutics industry. Cholesterol-lowering medicines can be costly, limiting therapy options for certain patients, particularly those without insurance or with limited financial means. This might have an influence on market growth by diminishing the overall demand for cholesterol-lowering therapies in the UAE. Furthermore, the high cost of drugs can have an influence on treatment adherence, limiting the efficacy of cholesterol-lowering therapy and potentially affecting patient outcomes.

Healthcare Policies and Regulatory Landscape

Healthcare policies in the UAE are predominantly guided by an array of laws, standards, regulations, and policies at both the federal and emirate levels. Overseeing the healthcare industry, including the oversight of drugs and medicines, is the responsibility of the UAE's drug regulatory authority, the Ministry of Health (MOH). Collaborating with entities like the Health Authority-Abu Dhabi (HAAD), the Dubai Health Authority (DHA), and the newly established Emirates Health Authority (EHA), the MOH plays a crucial role in monitoring and regulating the UAE's healthcare sector. Notably, the UAE has witnessed substantial growth and advancements in its healthcare sector, driven by efforts to diversify the economy and enhance public health. Significant investments in healthcare infrastructure, with over two-thirds of overall healthcare expenditure coming from public spending, underscore the government's commitment. Specialized healthcare zones, including Dubai Healthcare City and Dubai Biotechnology and Research Park, feature their regulatory bodies. The National Drug Policy focuses on governing the manufacturing, selling, and use of drugs and medicines for specific medical purposes, ensuring their safe and effective utilization in the UAE. This policy framework contributes to the overall enhancement of the country's healthcare system.

Competitive Landscape

Key Players:

- Amgen

- Pfizer

- Merck

- AstraZeneca

- Johnson & Johnson

- Julphar

- Cadila

- Sinopharm

- Sanofi

- AbbVie

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

UAE Cholesterol Therapeutics Market Segmentation

By Indication

- Hypercholesterolemia

- Hyperlipidaemia

- Cardiovascular Diseases

- Others

By Drug Class

- Statins

- Bile Acid Sequestrants

- Lipoprotein Lipase Activators

- Fibrates

- Others

By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

By End User

- Hospitals

- Speciality Clinics

- Homecare

- Academics & Research Centers

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Malaysia Pharmacy Market Analysis

Pharmaceuticals

Kuwait Diabetes Therapeutics Market Analysis

Pharmaceuticals

UK Brain Cancer Therapeutics Market

Related reports (by geography)

Healthcare Services

UAE Biomaterial Wound Dressing Market Analysis

Pharmaceuticals

UAE Viscosupplementation Market Analysis

Medical Devices

UAE Bio-Implant Market Analysis

Rare Diseases