Pharmaceuticals

Tanzania ADHD (Attention Deficit Hyperactivity Disorder) Therapeutic Market Analysis

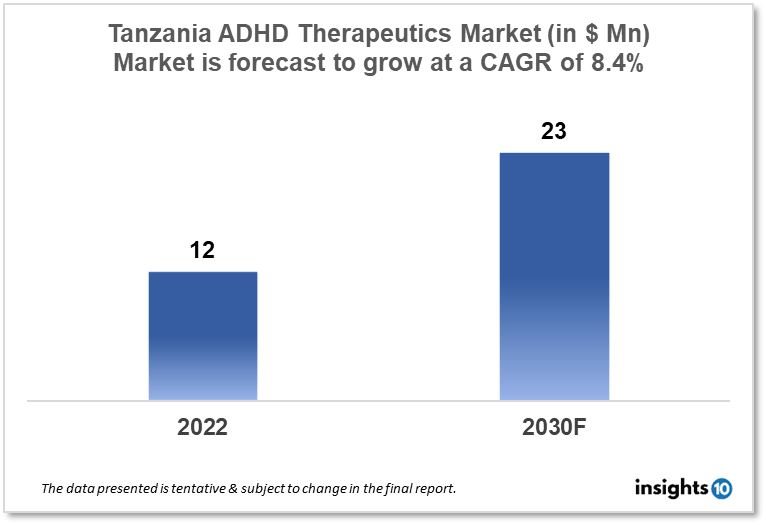

Tanzania Attention Deficit Hyperactivity Disorder (ADHD) therapeutics market is expected to witness growth from $12 Mn in 2022 to $23 Mn in 2030 with a CAGR of 8.4% for the year 2022-30. This growth is attributed to the rising incidence of ADHD among children and adults in Tanzania. The Tanzania ADHD therapeutics market is segmented by drug, drug type, demographics, and by distribution channel. Some of the major players in the market include Continental Pharma, Fern Pharmaceuticals, and Purdue Pharma.

Buy Now

Tanzania Attention Deficit Hyperactivity Disorder (ADHD) Therapeutics Market Executive Analysis

The Tanzania Attention Deficit Hyperactivity Disorder (ADHD) therapeutics market size is at around $12 Mn in 2022 and is projected to reach $23 Mn in 2030, exhibiting a CAGR of 8.4% during the forecast period. Tanzania has a weak healthcare infrastructure, limited resources, and high rates of maternal and infant mortality, HIV/AIDS, pneumonia, and malaria. The general population of Tanzania also has some of the lowest rates of worldwide access to medical professionals. In 2020–21, the government of Tanzania allotted $387.9 Mn for the health sector, of which $155.5 Mn was spent on development projects to aid in the implementation of the country's policies aimed at enhancing public health. In 2022/23, the industry received $470 Mn. International donors who give up to 40% of the health budget supplement the financing of healthcare. Through USAID and CDC, the US government makes a sizable contribution to initiatives that help the Tanzanian government. Only 32% of Tanzanians had health insurance as of 2019; this indicates the country's poor level of health insurance coverage. Only 1% of those people have private health insurance.

The most prevalent neurobehavioral childhood condition, Attention Deficit Hyperactivity condition (ADHD), manifests between the ages of 3 and 7 and is characterized by impulsivity, hyperactivity, and inattention. In Tanzania, it affects 2.2 to 17.8% of all school-age children and teenagers. Children with ADHD suffer negative consequences at home and at school. It causes agitation, reckless behavior, and lack of concentration, which could harm the child's performance. These symptoms are difficult to manage, especially for parents with limited knowledge and comprehension of the outcomes for the child. Treatments in Tanzania combine medication, psychotherapy, instruction, and information. Adult patients may receive medical care, psychoanalysis, counseling, education, or training. The most popular and well-known ADHD treatments are stimulants. When taking these medications with an immediate effect, 70 to 80 % of adolescents with ADHD experience fewer symptoms. Tanzania has authorized the use of non-stimulants for the therapy of ADHD. Although they do not work as rapidly as stimulants, they can still have an impact for up to 24 hours.

Market Dynamics

Market Growth Drivers

Tanzania is experiencing a rise in the incidence of ADHD, which is fuelling the Tanzania ADHD therapeutics market's expansion. Although the precise causes are unknown, variables like dietary changes, lifestyle changes, and environmental factors may be adding to the increase in prevalence.

Market Restraints

Tanzania is becoming more aware of ADHD, but many communities there still don't comprehend the disorder. Delays in diagnosis and therapy may result from this, which may have an effect on the market's expansion. Due to Tanzania's limited healthcare means, it may be difficult to diagnose and treat ADHD patients. There might be an extended wait to see a specialist, and many people might find the cost of treatment to be unaffordable. ADHD medications are frequently controlled drugs, so Tanzania may not have easy access to them. The capacity of medical professionals to prescribe medication may be affected by this, which may also restrict the Tanzania ADHD therapeutics market expansion.

Competitive Landscape

Key Players

- Abacus Chemists (TZA)

- Afya Laboratories (TZA)

- Biocare Health Products (TZA)

- Continental Pharma (TZA)

- Fern Pharmaceuticals (TZA)

- Purdue Pharma

- RespireRx Pharmaceuticals

- Supernus Pharmaceuticals

- Takeda Pharmaceutical

- Tris Pharma

Healthcare Policies and Regulatory Landscape

An executive agency under the Ministry of Health, Community Development, Gender, Elderly, and Children (MOHCDGE) is Tanzania Medicines and Medical Devices Authority (TMDA). The TMDA is in charge of overseeing the security, caliber, and efficacy of pharmaceuticals, medical equipment, and tests. The Tanzania Food, Drugs, and Cosmetics Act (TFDCA) cap. 219 as amended by the Finance Act of 2019 specifies the TMDA's mandate and outlines its primary responsibilities. The act outlines effective and thorough regulations and controls for the security and caliber of medications, medical equipment, and diagnostics on Tanzania's mainland. The TMDA is run as an Executive Agency in accordance with the 2009 amendments to the Executive Agencies Act, cap. 245, in order to enhance the delivery of public services.

The Tanzania Medicines and Medical Devices Authority (TMDA) has the following responsibilities to safeguard and advance public health: It is assessed both domestically produced products and services as well as imports for the quality, safety, and efficacy of human and veterinary medicines, herbal medicines, medical devices, and diagnostics. The TMDA should register the premises and issue a Premises Registration Certificate to any location intended to be used for the manufacture, storage, or sale of regulated products. Products that are subject to TMDA regulation must be registered and issued with a Product Registration Certificate after they are made or imported into the nation in order to be permitted to be sold. Once their facilities and goods have been listed, all TMDA-regulated product manufacturers and dealers should receive a TMDA Business Permit.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

ADHD (Attention Deficit Hyperactivity Disorder) Therapeutic Market Segmentation

By Drug Type (Revenue, USD Billion):

- Stimulants

- Amphetamine

- Methylphenidate

- Dextroamphetamine

- Dexmethylphenidate

- Lisdexamfetamine

- Others

- Non-Stimulants

- Atomoxetine

- Bupropion

- Guanfacine

- Clonidine

By Age Group (Revenue, USD Billion):

- Pediatric And Adolescent

- Adult

By Distribution Channel (Revenue, USD Billion):

- Hospital Pharmacies

- Speciality Clinics

- Retail Pharmacies

- e-Commerce

By Psychotherapy (Revenue, USD Billion):

- Behaviour Therapy

- Cognitive Behavioral Therapy

- Interpersonal Psychotherapy

- Family Therapy

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Malaysia Cough Remedies Market Analysis

Pharmaceuticals

Mexico Ophthalmic Drugs Market Analysis

Pharmaceuticals

Malaysia Transthyretin Amyloidosis (ATTR) Market Analysis

Related reports (by geography)

OTC & Nutraceuticals

Tanzania Over The Counter (OTC) Analgesics Market Analysis

Pharmaceuticals

Tanzania Vitamin and Minerals Market Analysis

Pharmaceuticals

Tanzania Obesity Drugs Market Analysis

Pharmaceuticals