Healthcare Services

Spain Physiotherapy Market Analysis

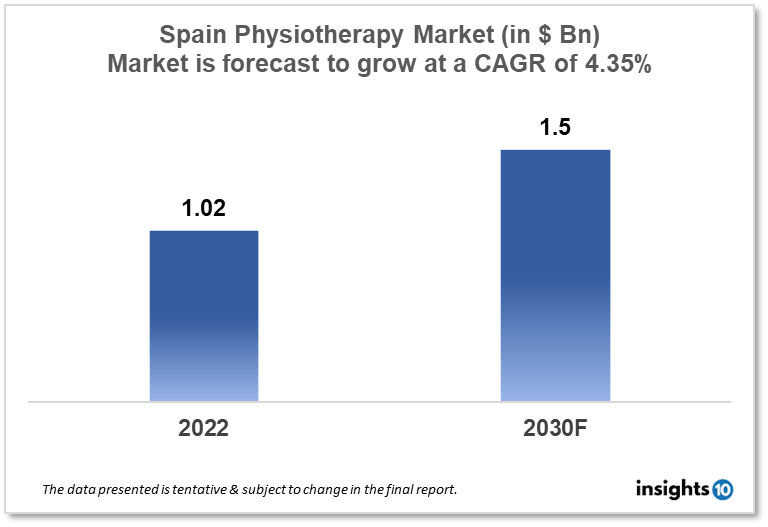

The Spain physiotherapy market size was valued at $1.02 Bn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 4.35% from 2022 to 2030 and will reach $1.5 Bn in 2030. Spain physiotherapy market is expected to grow due to, an increase in chronic diseases, an aging population, and a growing awareness on physiotherapy. The market is segmented by Product Type, Application Type and End User. The major players in the Spain physiotherapy market Fisio Equipment, Fisioterapia-movil, Fisio-line, Physiomed and others.

Buy Now

Spain Physiotherapy Market Executive Summary

The Spain physiotherapy market size was valued at $1.02 Bn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 4.35% from 2022 to 2030 and will reach $1.5 Bn in 2030. Spain's healthcare expenditure as a percentage of GDP is around 9.6% as of 2021. This is considered to be a relatively high level of expenditure when compared to other countries. The Spanish government funds most of the healthcare expenditures through taxes and social security contributions. The country has a public healthcare system that provides universal coverage to all citizens.

Physiotherapy services in Spain can include a wide range of treatments such as manual therapy, exercise therapy, electrotherapy, ultrasound therapy, and other techniques to help patients recover from injuries, surgeries, or conditions that affect mobility and function.

This report also notes that there are many small and medium-sized businesses working in the sector, which contributes to the market's extreme fragmentation. In Spain, physical therapy is most frequently provided in hospitals, rehabilitation facilities, nursing homes, and private offices.

Market Dynamics

Market Growth Drivers

Spain's Physiotherapy market growth is driven by a number of factors, including an aging population and increasing incidence of chronic conditions such as obesity, diabetes, and cardiovascular disease, which require physiotherapy services. Additionally, the increasing awareness of the benefits of physiotherapy and the government's efforts to improve access to healthcare services are also contributing to the growth of the market.

Market Restraints

The reimbursement rates for these services are very low, which may restrict certain patients' access to these therapies even though physiotherapy is covered by Spain's national healthcare system and patients are typically compensated for a portion of the treatment costs. Despite the fact that physiotherapy treatments are offered in Spain, access might occasionally be restricted, especially in remote or underserved areas, which will constrain the country's physiotherapy market.

Competitive Landscape

Key Players

- Fisio Equipment (ESP)

- Fisioterapia-movil (ESP)

- Fisio-line (ESP)

- Physiomed (ESP)

- BTL Industries

- EMS Physio Ltd.

- DJO Global, Inc.

- Dynatronics Corporation, Inc.

- Medline Industries

- Performance Health

Healthcare Policies and Regulatory Landscape

Policy changes and Reimbursement scenario of Spain Physiotherapy Market

In Spain, the regulatory body for physiotherapy equipment is the Spanish Agency for Medicines and Medical Devices (AEMPS). This agency is responsible for the regulation and control of medical devices in Spain, including physiotherapy equipment. The AEMPS is responsible for ensuring that all physiotherapy equipment sold in Spain meets certain safety and performance standards and that they are labeled and marketed correctly.

The AEMPS works closely with the European Medicines Agency (EMA) and the European Union (EU) to ensure that all physiotherapy equipment sold in Spain complies with EU regulations. All physiotherapy equipment must be CE marked to indicate that it meets the essential requirements of the EU Medical Devices Directive before it can be sold in Spain.

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Physiotherapy Market Segmentation

By Product: (Revenue, USD Billion):

Based on product, the physiotherapy equipment market is divided into two major segments, namely, equipment and accessories. The equipment segment accounted for the largest share of the physiotherapy equipment market in 2021. The equipment segment is further segmented into electrotherapy equipment, ultrasound equipment, exercise therapy equipment, heat therapy equipment, cryotherapy equipment, combination therapy equipment, continuous passive motion therapy equipment, shockwave therapy equipment, laser therapy equipment, magnetic pressure therapy equipment, traction therapy, and other physiotherapy equipment (hydrotherapy and vacuum therapy). Owing to the increasing use of electrotherapy equipment in the treatment of musculoskeletal disorders and owing to increasing concerns for patients’ safety and minimal/no side-effects during the physiotherapy treatments.

- Equipment

- Electrotherapy equipment

- Ultrasound equipment

- Exercise therapy equipment

- Heat therapy equipment

- Cryotherapy equipment

- Combination therapy equipment

- Continous passive motion therapy equipment

- Shockwave therapy equipment

- Laser therapy equipment

- Magnetic pressure therapy equipment

- Traction therapy

- Other physiotherapy equipment

- Accessories

- Manual Therapy

- Specialized treatment

- Joint Mobilization Techniques

- Suspension Therapy

By Application (Revenue, USD Billion):

Based on application, the physiotherapy equipment market is segmented into musculoskeletal applications, neurological applications, cardiovascular and pulmonary applications, pediatric applications, gynecological applications, and other applications (including sports and palliative care). The musculoskeletal applications segment holds a dominating share attributed to the increasing adoption of physiotherapies to accelerate recovery of accidental injuries, rising incidence of musculoskeletal disorders, and growth in the geriatric population.

By Applications

- Musculoskeletal applications

- Neurological applications

- Cardiovascular and pulmonary applications

- Pediatric applications

- Gynecological applications

- Other applications

By End-user (Revenue, USD Billion):

Based on end users, the physiotherapy equipment market is segmented into physiotherapy & rehabilitation centers, hospitals, home care settings, physician offices, and other end users (community health centers and elderly care facilities). In 2021, the physiotherapy & rehabilitation centers segment accounted for the largest share of the physiotherapy equipment market due to increasing demand for advanced physiotherapy equipment and their wide usage across the care continuum across these centers.

- Physiotherapy & Rehabilitation centers

- Hospitals

- Home care settings

- Physician offices

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

Africa Bioinformatics Market Analysis

Healthcare Services

Denmark Healthcare Insurance Market Analysis

Healthcare Services

Europe Clinical Diagnostics Market Analysis

Related reports (by geography)

Pharmaceuticals

Spain Alexipharmic Drugs Market Analysis

Medical Devices

Spain Medical Devices Market Analysis

Healthcare Services