Pharmaceuticals

Spain Constipation Therapeutics Market Analysis

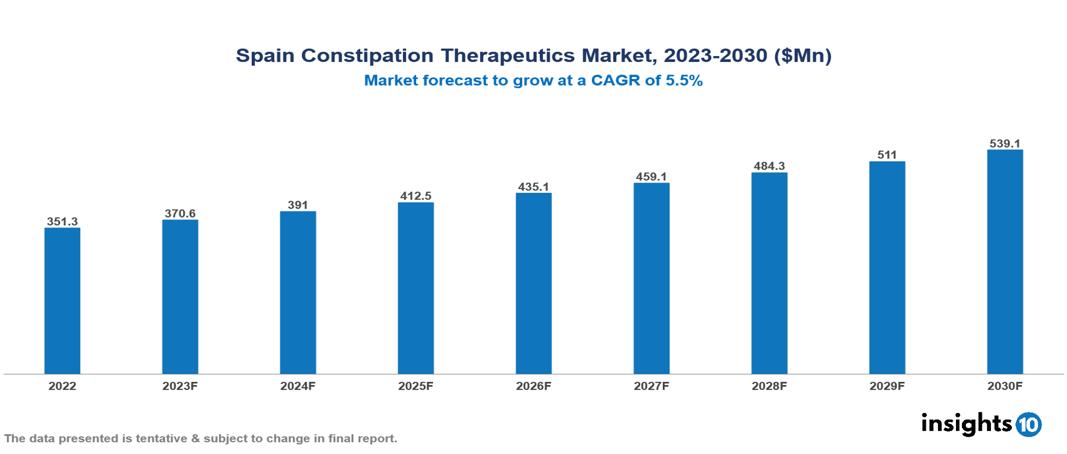

Spain Constipation Therapeutics Market was valued at $351 Mn in 2022 and is estimated to reach $539 Mn in 2030, exhibiting a CAGR of 5.5% during the forecast period. The constipation therapeutics market is experiencing growth driven by the rising prevalence of constipation worldwide, attributed to factors like aging, sedentary lifestyles, and unhealthy dietary habits, with the expanding elderly population, more prone to chronic conditions, further contributing to this market expansion. Notable participants in this industry include AbbVie, Almirall, Boehringer Ingelheim, Ferring Pharmaceuticals, Ipsen Pharma, Johnson & Johnson, Norgine Pharmaceuticals, Pierre Fabre Médicament, Recordati, and Sanofi.

Buy Now

Spain Constipation Therapeutics Market Executive Summary

Spain Constipation Therapeutics Market was valued at $351 Mn in 2022 and is estimated to reach $539 Mn in 2030, exhibiting a CAGR of 5.5% during the forecast period.

Constipation is a digestive condition characterized by infrequent, difficult, or hard bowel movements due to slowed transit of stool through the colon, leading to increased water absorption and stool hardening. This condition results from a decrease in the speed at which feces pass through the large intestine. Common symptoms of constipation include straining during defecation, a sensation of incomplete evacuation, abdominal discomfort, and irregular or infrequent bowel habits. Various factors, such as a low-fiber diet, insufficient fluid intake, lack of physical activity, specific medications, and underlying medical issues, can contribute to constipation. Treating constipation often involves lifestyle modifications, dietary changes, increased physical activity, and, when necessary, the use of medications to manage and alleviate symptoms.

Constipation is notably widespread in Spain, particularly among women. Among healthy young women, the prevalence of functional constipation stands at 28.8%, with 8.2% experiencing symptoms of dyssynergic defecation. Self-reported constipation has a prevalence rate of 29.5%. The prevalence of constipation among treated patients in Spain varies by age, with the highest rates observed in individuals aged 65 and older. Lifestyle factors like diet, physical activity, and overall health habits, along with age, can influence the prevalence of constipation, with older individuals potentially facing higher rates. Access to healthcare services and socioeconomic factors may further contribute to variations in the prevalence and management of constipation within the Spanish population.

In the field of constipation therapeutics, innovative methods are gaining traction. Promising results in clinical trials highlight drugs targeting serotonin 4 (5-HT4) and guanylate cyclase C (GC-C) receptors as novel approaches. These pharmacological interventions open avenues for expanded treatment options. Simultaneously, ongoing research explores the intricate role of the gut microbiome in constipation. Studying microbiome-based therapies aims to enhance bowel function by modifying gut microbiota. This evolving field holds potential for tailored treatments that leverage the microbiome's capabilities, offering exciting prospects for the future of constipation management.

Market Dynamics

Market Growth Drivers

High Prevalence among Specific Demographics: The constipation therapeutics market in Spain is driven by a high prevalence of constipation, particularly among specific demographic groups such as women and the elderly, creating a substantial demand for effective treatment options.

Lifestyle Factors Impacting Prevalence: Lifestyle factors, including sedentary habits and dietary choices, contribute significantly to the widespread occurrence of constipation, further boosting the demand for therapeutic interventions in the market.

Aging Population's Impact: As of 2023, Spain ranks among the top five countries in the EU with the highest proportions of elderly citizens, as 19.1% of its population is aged 65 and over, and this percentage is anticipated to steadily rise, reaching 37% by 2050, positioning Spain as the second-highest globally in terms of the percentage of elderly individuals, following Japan. With the expanding aging population, particularly individuals aged 65 and older exhibiting higher prevalence rates, there is a growing need for targeted constipation treatments, driving market growth.

Market Restraints

Regulatory and Safety Concerns: Some medications, such as cisapride and tegaserod, have been withdrawn from the market or granted restricted indications due to potential undesirable consequences, which has led to a cautious approach to approving new drugs for constipation treatment.

Cost and Affordability: The constipation therapeutics market faces notable challenges in terms of cost and affordability, with the high expenses linked to newer medications limiting accessibility, particularly for individuals without comprehensive insurance coverage. Unequal healthcare access in rural areas further hampers timely diagnosis and treatment. Additionally, elevated out-of-pocket costs, even with insurance, act as barriers for some patients, affecting market penetration and growth.

Patient Compliance and Side Effects: Some constipation treatments, such as laxatives, may have side effects that can deter patients from using them consistently, which can limit the effectiveness of these therapies. Additionally, some patients may not be willing to adopt lifestyle changes, such as increased fluid intake and physical activity, which can also impact the success of constipation treatments.

Healthcare Policies and Regulatory Landscape

In Spain, the oversight of pharmaceutical effectiveness, safety, and quality, encompassing treatment drugs, falls under the purview of the Spanish Agency for Medicines and Health Products (Agencia Española de Medicamentos y Productos Sanitarios, AEMPS). The national healthcare system, providing coverage to all citizens, exerts influence on healthcare policies. Spain follows a decentralized healthcare model, the Systema Nacional de Salud (SNS), where local regions manage healthcare services. Regulations also govern drug access, pricing, and reimbursement policies, with decisions often made at both national and regional levels.

Competitive Landscape

Key Players

- AbbVie

- Almirall

- Boehringer Ingelheim

- Ferring Pharmaceuticals

- Ipsen Pharma

- Johnson & Johnson

- Norgine Pharmaceuticals

- Pierre Fabre Médicament

- Recordati

- Sanofi

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Spain Constipation Therapeutics Market Segmentation

By Therapeutic

- Laxatives

- Chloride Channel Activators

- Peripherally Acting Mu-Opioid Receptor Antagonists

- GC-C Agonists

- 5-HT4 Receptor Agonists

By Disease

- Chronic Idiopathic Constipation

- Irritable Bowel Syndrome with Constipation

- Opioid-Induced Constipation

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Indonesia Hepatitis C Drugs Market Analysis

Pharmaceuticals

Japan Oral Contraceptives Market Analysis

Pharmaceuticals

Japan Cancer Induced Bone Diseases Therapeutics Market

Related reports (by geography)

Digital Health

Spain Blockchain Technology in Healthcare Market Analysis

Pharmaceuticals

Spain Respiratory Drugs Market Analysis

Pharmaceuticals

Spain Liver Diseases Therapeutics Market Analysis

Healthcare Services