Pharmaceuticals

Spain Cardiovascular Drugs Market Analysis

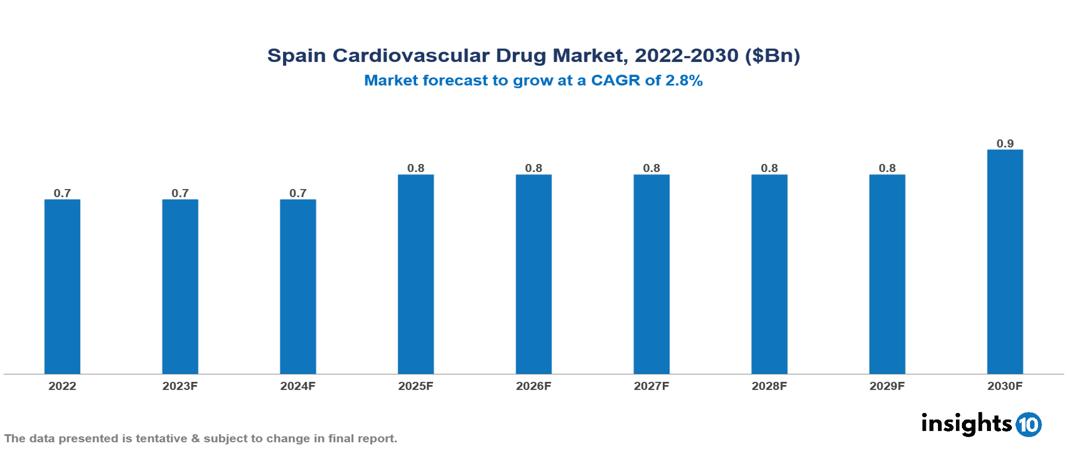

Spain Cardiovascular Drug Market is at around $2.67 Bn in 2022 and is projected to reach $3.30 Bn in 2030, exhibiting a CAGR of 2.8% during the forecast period. Major reasons propelling the growth of this market are the increasing prevalence of chronic diseases and technological advancements. The market is dominated by key players like Bristol-Myers Squibb Company, Pfizer Inc., Bayer AG, Janssen Pharmaceuticals, Inc., AstraZeneca, Sanofi, Novartis AG, Merck & Co., Inc., Gilead Sciences, Inc., and F. Hoffman-La Roche Ltd.

Buy Now

Spain Cardiovascular Drug Market Executive Summary

Spain Cardiovascular Drug Market is at around $2.67 Bn in 2022 and is projected to reach $3.30 Bn in 2030, exhibiting a CAGR of 2.8% during the forecast period.

Heart attacks, strokes, and venous thromboembolism are classified as cardiovascular disorders since they affect the blood and lymphatic vessels in addition to the cardiovascular system. Heart attacks and strokes are usually acute events caused by a blockage that prevents blood flow to the heart or brain. Access to appropriate medications such as aspirin, beta-blockers, angiotensin-converting enzyme inhibitors, and statins is crucial for patients with cardiac problems.

An aging population, improved knowledge of cardiac disease, and more research and development for the launch of innovative treatments are all driving the market's growth. 20% of the population is 65 years of age or older, with both men's and women's life expectancy consistently rising. In the upcoming years, the market is anticipated to grow due to an increase in awareness campaigns on the prevention and treatment of cardiovascular diseases.

Pharma revenues increased dramatically over the preceding two decades, reaching $138.33 Bn globally in 2022. With the introduction of new technologies and more economical and effective manufacturing techniques, the pharmaceutical industry has undergone a significant transformation. Additionally, the market's expansion has benefited from the growing influx of investments in this sector.

Bristol-Myers Squibb (BMS) holds a significant market share in the Spanish cardiovascular medicine industry, particularly in the anticoagulant and antiplatelet drug categories. Eliquis and Apixaban, the company's main products, are two of the most popular anticoagulants in Spain.

Market Dynamics

Market Growth Drivers:

Prevalence of Cardiovascular Diseases: The frequency of cardiovascular diseases is very high in Spain. This is exacerbated by sedentary lifestyles, aging populations, and food habits. In Spain, cardiovascular disorders are responsible for 32% of all deaths.

Medical Research Advancements: New medications and treatment techniques are discovered as a result of ongoing research and development activities in the field of cardiovascular medicine. The market is expanding as a result of advances in medication development, such as new therapeutic targets and modes of action.

Enhancing Healthcare Infrastructure: Diagnosis and treatment of cardiovascular diseases are supported by improvements in the healthcare infrastructure, which include the availability of well-equipped hospitals and specialist cardiovascular care centers. The need for cardiovascular medications is fuelled by accessibility to cutting-edge medical facilities.

Market Restraints:

Generic Competition: As branded cardiovascular medication patents expire, generic substitutes could become more widely available. Pricing pressures may result from generic competition's impact on the market share and profitability of brand-name medications.

Regulatory Difficulties: Pharmaceutical businesses may face difficulties navigating the intricate approval procedure and strict regulatory regulations. Overcoming regulatory obstacles could cause a delay in the release of novel cardiovascular medications.

Healthcare Budget Restraints: The use of pricey cardiovascular medications may be restricted by financial restraints in the healthcare system. Access to the market may be hampered by payers' reluctance to reimburse expensive drugs, such as the government or insurance companies.

Notable Recent Updates

- April 2022, Grifols finalizes the acquisition of Biotest. Grifols can expedite and broaden its product offering in Europe with the acquisition of Biotest AG

Healthcare Policies and Regulatory Landscape

Spanish Agency of Medicines and Medical Devices (AEMPS) is the regulatory body that grants marketing authorization for all medications used in Spain. The applicant sends the dossier with all the necessary data to the AEMPS to get the drug's marketing authorization in Spain and simultaneously files its permission application to multiple EU member states. Coordination with the European Medicines Agency (EMA) and other EU member states is required. Complicacy is increased when regulatory standards are harmonized throughout the EU.

Competitive Landscape

Key Players:

- Bristol-Myers Squibb Company

- Pfizer Inc.

- Bayer AG

- Janssen Pharmaceuticals, Inc.

- AstraZeneca

- Sanofi

- Novartis AG

- Merck & Co., Inc.

- Gilead Sciences, Inc.

- F. Hoffmann-La Roche Ltd

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Spain Cardiovascular Drug Market Segmentation

By Drug Type

- Cephalosporins

- Antihypertensive

- Antihyperlipidemic

- Anticoagulants

- Antiplatelet Drug

- Others

By Disease Indication

- Hypertension

- Hyperlipidemia

- Coronary Artery Disease

- Arrhythmia

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Saudi Arabia Photorejuvenation Market Analysis

Pharmaceuticals

Egypt Asthma Drugs Market Analysis

Related reports (by geography)

Medical Devices

Spain Cardiac Monitoring Devices Market Analysis

Clinical Trials

Spain Oncology Clinical Trials Market Analysis

Rare Diseases