Pharmaceuticals

South Korea Cardiovascular Diseases Therapeutics Market Analysis

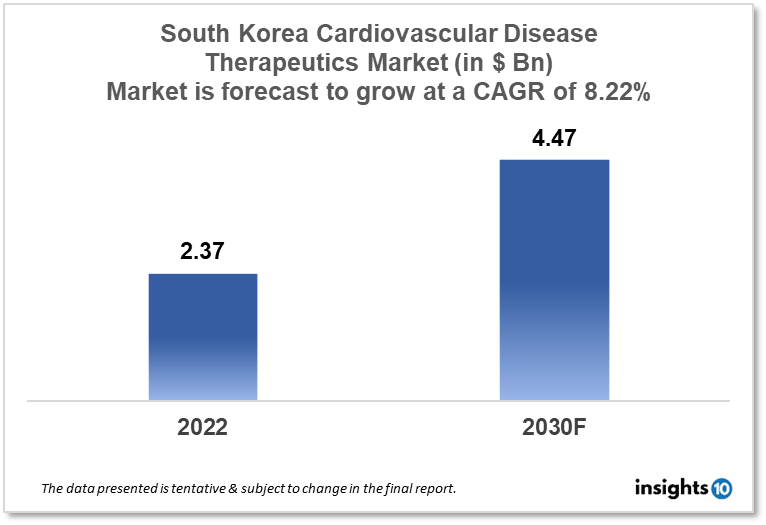

The South Korean cardiovascular disease therapeutics market is projected to grow from $2.37 Bn in 2022 to $4.47 Bn in 2030 with a CAGR of 8.22% for the year 2022-2030. The increasing awareness of cardiovascular diseases and the rising ageing population are responsible for the growth of the market. The South Korean cardiovascular disease therapeutics market is segmented by disease indication, drug type, route of administration, drug classification, mode of purchase, and by the end user. Kolmar, Kwang Dong Pharmaceutical, and AstraZeneca are the major players in the South Korean cardiovascular disease therapeutics market.

Buy Now

South Korea Cardiovascular Disease Therapeutics Market Executive Analysis

The South Korean cardiovascular disease therapeutics market is at around $2.37 Bn in 2022 and is projected to reach $4.47 Bn in 2030, exhibiting a CAGR of 8.22% during the forecast period. The fiscal imbalance is expected to decrease from 3.3% of gross domestic product (GDP) this year to 0.6% of GDP with the approved budget of South Korea, which is worth $498.89 Bn, or 6% less than this year's budget. According to the finance ministry, public health, welfare, and employment programs received the largest %age of the budget—35.4%—with 15.1% going to education and 8.9% going to national defence expenditures.

In South Korea, Cardiovascular Diseases (CVDs) are now one of the main sources of morbidity and mortality and are a significant financial burden on the healthcare system. Neoplasms accounted for 28.4% of all deaths recorded in South Korea while circulatory diseases (heart disease 12.8% and cerebrovascular disease 8.3%) accounted for 21.5%.

Plasma cholesterol, especially low-density lipoprotein (LDL) cholesterol, has been linked to the onset and progression of Atherosclerotic cardiovascular disease (ASCVD) across a number of genetic, epidemiologic, and clinical investigations. Although statins (3-hydroxy-3-methylglutaryl-coenzyme A reductase inhibitors) have long been the preferred method of treating dyslipidemia, high-risk patients still have a significant residual risk despite statin therapy. The understanding of lipoprotein metabolism has been drastically altered since the 2003 finding of proprotein convertase subtilisin/kexin type 9 (PCSK9). By encouraging the degradation of LDL receptors, PCSK9 reduces the clearance of LDL cholesterol from circulation. The findings of two recent cardiovascular outcomes trials suggest that patients with ASCVD may gain incrementally from taking a PCSK9 inhibitor in addition to statin therapy. Alirocumab has been authorized in South Korea to treat patients with clinical ASCVD or heterozygous familial hypercholesterolemia who need additional LDL cholesterol lowering in conjunction with other therapies, usually including a maximally tolerated statin. Patients with clinical ASCVD or homozygous or heterozygous familial hypercholesterolemia who need additional LDL cholesterol reduction in conjunction with other lipid-lowering therapies can use evolocumab.

Market Dynamics

Market Growth Drivers

The demand for therapeutics to control and treat these conditions is being driven by South Korea's high prevalence of cardiovascular diseases. The market is expanding in part due to the rising prevalence of risk factors like high blood pressure, high cholesterol, obesity, and diabetes. The prevalence of cardiovascular diseases rises as the populace ages. The rapidly ageing populace of South Korea is predicted to increase the demand for treatments for cardiovascular disease. The area of cardiovascular disease therapeutics is continually developing new technologies and treatment options. South Korea is renowned for its cutting-edge medicinal technology, which will probably aid in South Korea's cardiovascular disease therapeutics market expansion.

Market Restraints

The cost of cardiovascular disease therapies may prevent people with lower incomes from accessing them. This may hinder the South Korean cardiovascular disease therapeutics market expansion, especially considering the rising expense of healthcare. There are now generic versions of many cardiovascular disease treatments, which can result in price competition and reduced profit margins for businesses that manufacture branded medications. For businesses creating novel therapeutics for cardiovascular disease, the regulatory climate in South Korea can be difficult. Stringent criteria for clinical trials and approvals can result in delays and increased expenses for drug development.

Competitive Landscape

Key Players

- DanDi Bioscience (KOR)

- SparkBiopharma (KOR)

- Yuhan Corporation (KOR)

- Kolmar (KOR)

- Kwang Dong Pharmaceutical (KOR)

- AstraZeneca

- Bayer

- Sanofi

- Pfizer

- Eli Lilly

- Sanofi

- Bristol-Myers Squibb

Healthcare Policies and Regulatory Landscape

The National Health Insurance (NHI) program, part of South Korea's complete healthcare system, provides coverage for cardiovascular health services and medications. Over 98% of the population, including both citizens and legal residents, is covered by the NHI, a social insurance scheme that is required by law. To determine the health of their heart and blood arteries, patients can undergo diagnostic tests like electrocardiograms (ECGs), echocardiograms, stress tests, and angiograms. The NHI covers a variety of medications, such as antiplatelets, anticoagulants, beta-blockers, ACE inhibitors, and statins, for the therapy of cardiovascular diseases. For patients with more severe cardiovascular diseases, the NHI also provides procedures like percutaneous coronary intervention (PCI), coronary artery bypass grafting (CABG), and cardiac pacemaker implantation. The government sets the reimbursement rates for these services and medicines, which are open to adjustment based on elements like service costs, inflation, and advancements in medical technology. In order to assist patients with low incomes cover the cost of healthcare, the NHI also provides subsidies.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Cardiovascular Disease Therapeutics Segmentation

By Disease Indication (Revenue, USD Billion):

- Hypertension

- Coronary Artery Disease

- Hyperlipidaemia

- Arrhythmia

- Others

By Drug Type (Revenue, USD Billion):

- Antihypertensive

- Anticoagulants

- Antihyperlipidemic

- Antiplatelet Drugs

- Others

By Route of Administration (Revenue, USD Billion):

- Oral

- Parenteral

- Others

By Drug Classification (Revenue, USD Billion):

- Branded Drugs

- Generic Drugs

By Mode of Purchase (Revenue, USD Billion):

- Prescription-Based Drugs

- Over-The-Counter Drugs

By End Users (Revenue, USD Billion):

- Hospital Pharmacies

- Online Pharmacies

- Retail Pharmacies

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Kenya Alcohol Addiction Therapeutics Market Analysis

Pharmaceuticals

Kenya Anti Aging Therapeutics Market Analysis

Pharmaceuticals

South Africa Clinical Nutrition for Cancer Care Market Analysis

Related reports (by geography)

Pharmaceuticals

South Korea Liver Disease Drugs Market Analysis

Pharmaceuticals

South Korea Pharmaceutical Market Analysis

Pharmaceuticals

South Korea Depression Therapeutics Market Analysis

Pharmaceuticals