Pharmaceuticals

South Africa Mouth Ulcer Therapeutics Market Analysis

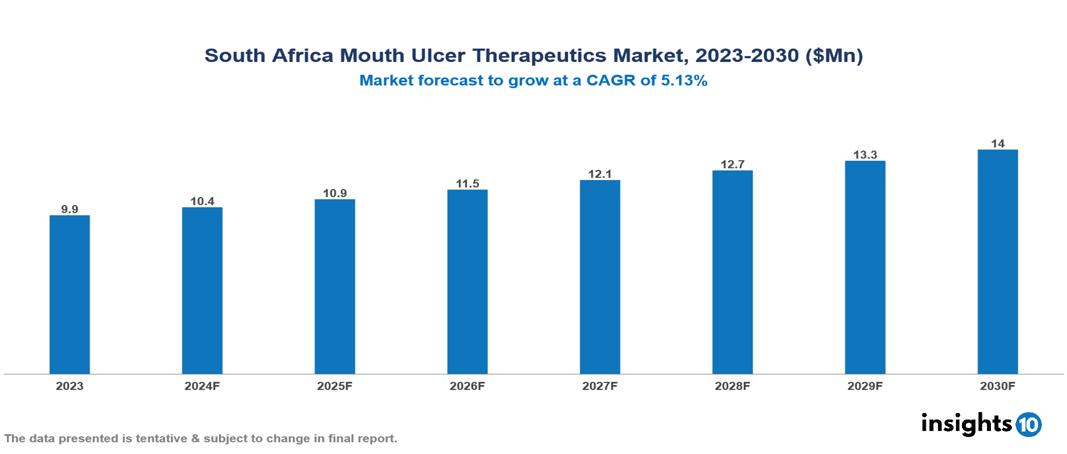

The South Africa Mouth Ulcer Therapeutics Market was valued at $9.9 Mn in 2023 and is projected to grow at a CAGR of 5.13% from 2023 to 2023, to $14 Mn by 2030. The key drivers of this industry are rising awareness about oral hygiene, increasing demand for rapid healing products, growing geriatric population, rise in tobacco consumption, increasing incidence of oral diseases, chemical-based toothpaste and unhealthy lifestyles etc. The industry is primarily dominated by players such as Aspen Pharmacare, Cipla Medpro, Sanofi, GlaxoSmithKline PLC, Pfizer, Inc. among others.

Buy Now

South Africa Mouth Ulcer Therapeutics Market Executive Summary

The South Africa Mouth Ulcer Therapeutics Market is at around $9.9 Mn in 2023 and is projected to reach $14 Mn in 2030, exhibiting a CAGR of 5.13% during the forecast period 2023-2030.

Mouth ulcers are painful sores that develop inside the mouth, characterized by small, round or oval lesions with a white, yellow, or gray center surrounded by a red border. These sores can cause significant discomfort, especially when eating or drinking. Various factors contribute to their development, including minor mouth injuries, stress, hormonal changes, nutritional deficiencies, certain medical conditions, allergic reactions, and genetic predisposition. Treatment options range from over-the-counter solutions like antimicrobial mouthwashes and topical anesthetics to home remedies such as salt-water rinses and avoiding irritating foods. In severe cases, medical interventions may include prescription mouthwashes, gels, or corticosteroids. Addressing underlying causes through stress management, improved nutrition, and treatment of related medical conditions can also be beneficial. While most mouth ulcers heal independently within 1-2 weeks, persistent, large, or frequent ulcers warrant professional medical attention to rule out more serious conditions and ensure appropriate treatment.

The prevalence of recurrent aphthous ulcers (mouth ulcers) in South Africa, ranges from 25% to 40%. The market therefore is driven by significant factors like an aging population, lifestyle changes and increasing prevalence, however, factors such as limited accessibility, hight cost of medications and competition from generic and over-the-counter products limit market growth.

The industry is primarily dominated by players such as Aspen Pharmacare, Takeda, Teva Pharmaceuticals, Cipla Medpro, Sanofi, GlaxoSmithKline PLC, Pfizer, Inc. among others.

Market Dynamics

Market Dynamics

Market Growth Drivers

Prevalence of mouth ulcers: High prevalence of recurrent aphthous ulcers (mouth ulcers) in South Africa, with estimates ranging from 25% to 40% in the general population. This significant patient base could drive the demand for effective treatment options.

Lifestyle and stress factors: Increased stress levels, poor dietary habits, and certain lifestyle factors prevalent in urban areas of South Africa may contribute to the development of mouth ulcers. Addressing these risk factors could drive the market for preventive and therapeutic solutions.

Aging population: South Africa has an aging population, and the elderly are more susceptible to developing mouth ulcers due to factors such as weakened immune systems and certain medical conditions. The growing elderly population could fuel the demand for mouth ulcer treatments.

Market Restraints

Limited Access to healthcare: Limited access to healthcare services, particularly in rural areas and low-income communities, can hinder the diagnosis and treatment of mouth ulcers. Inadequate healthcare infrastructure and resources may restrict market growth.

Hight Cost of Medications: The cost of certain mouth ulcer treatments, especially newer or branded medications, may be prohibitive for a significant portion of the population. Affordability concerns could limit market penetration and adoption.

Competition from generic and over-the-counter products: The availability of generic and over-the-counter (OTC) products for managing mouth ulcers may limit the market share and growth potential of branded or prescription treatments. Effective marketing and differentiation strategies may be required to compete with generic and OTC options.

Regulatory Landscape and Reimbursement Scenario

In South Africa, the main regulatory body overseeing drugs and pharmaceuticals is the South African Health Products Regulatory Authority (SAHPRA). SAHPRA is responsible for ensuring the safety, efficacy, and quality of health products, including medicines, medical devices, and complementary medicines. The authority was established to replace the Medicines Control Council (MCC) and operates independently to regulate and control these products from development to post-marketing surveillance.

The process of obtaining licensure for drugs and pharmaceuticals in South Africa involves rigorous evaluation by SAHPRA. Applicants are required to submit comprehensive documentation, including data on the product's safety, efficacy, and quality. Once a product is deemed to meet the necessary standards, it is granted marketing authorization.

The regulatory environment for new entrants is demanding, necessitating compliance with stringent regulatory requirements. However, SAHPRA aims to facilitate timely access to safe and effective health products, and new entrants can navigate the process by adhering to regulatory guidelines to ensure compliance with South Africa's pharmaceutical regulations.

Competitive Landscape

Key Players

Here are some of the major key players in the South Africa Mouth Ulcers Therapeutics Market:

- Aspen Pharmacare

- Cipla Medpro

- Pfizer, Inc.

- Teva Pharmaceuticals.

- GlaxoSmithKline plc.

- Sanofi

- Takeda

- Pfizer

- Bayer

- Novartis

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

South Africa Mouth Ulcer Treatment Market Segmentation

By Treatment Drug Class

- Corticosteroid

- Antihistamine

- Antimicrobial

- Analgesic

- Anesthetic

- Anti-inflammatory Agents

By Treatment Formulation Type

- Gel

- Mouthwash

- Ointment

- Spray

- Lozenges

Mouth Ulcer Treatment Indications

- Aphthous Stomatitis

- Oral Lichen Planus

- Others

By End Users

- Pharmacy

- Online Stores

- Hospitals and Clinics

- Home care

Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

South Africa Pancreatic Cancer Drugs Market Analysis

Pharmaceuticals

Vietnam Inhaled Nitric Oxide Market Analysis

Pharmaceuticals

UK Acne Drugs Market Analysis

Related reports (by geography)

Pharmaceuticals

South Africa Photorejuvenation Market Analysis

Pharmaceuticals

South Africa Oncology Therapeutics Market Analysis

Pharmaceuticals

South Africa Oncology Drugs Market Analysis

Pharmaceuticals