Pharmaceuticals

South Africa HIV Drugs Market Analysis

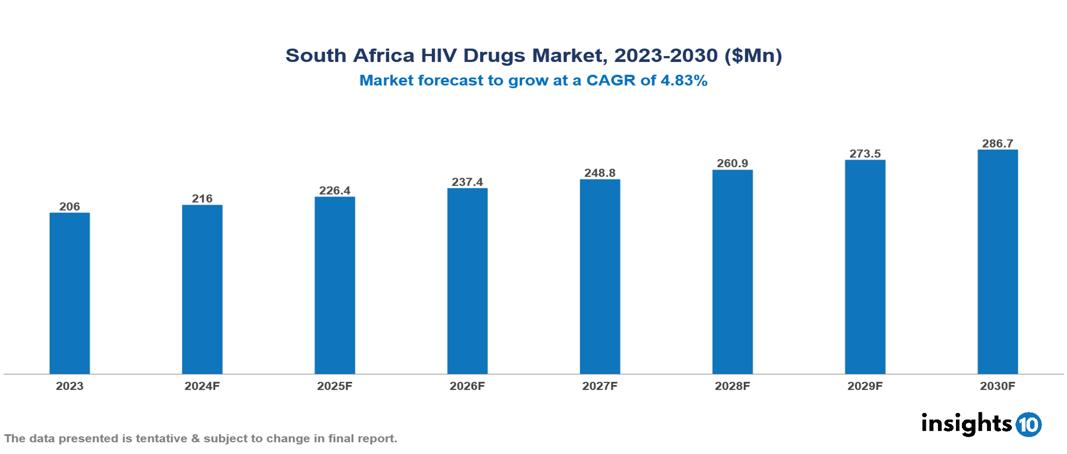

South Africa HIV Drugs Market is at around $0.21 Bn in 2023 and is projected to reach $0.29 Bn in 2030, exhibiting a CAGR of 4.83% during the forecast period. The expansion of the market is due to factors such as collaboration and partnership with foreign organizations, the increasing prevalence of HIV/ Aids, and technological advancements in the field. The market is dominated by key players like Aspen Pharmacare, Adcock Ingram, Gilead Sciences, ViiV Healthcare, Boehringer Ingelheim International GmbH, Janssen Pharmaceuticals, Merck & Co., Bristol-Myers Squibb, AbbVie Inc., F. Hoffmann-La Roche Ltd., and Novartis.

Buy Now

South Africa HIV Drugs Market Executive Summary

South Africa HIV Drugs Market is at around $0.21 Bn in 2023 and is projected to reach $0.29 Bn in 2030, exhibiting a CAGR of 4.83% during the forecast period.

South Africa's HIV pharmaceuticals market produces, distributes, and consumes medications used to treat HIV/ AIDS within the country. With one of the highest rates of HIV prevalence in the world, South Africa has a major market for antiretroviral therapy (ART) and other related drugs. Government regulations, the quality of the healthcare system, prevalence rates, and the accessibility of generic medications are some of the variables that impact the market.

Due to the high prevalence rates and government initiatives to increase treatment accessibility, the market for HIV medications in South Africa is still expanding steadily. Prominent participants in the industry are global pharmaceutical corporations and regional producers, emphasizing the creation of reasonably priced generic antiretroviral medications. Continual research and development endeavors are directed at enhancing treatment alternatives and tackling novel obstacles such as medication resistance and co-occurring conditions.

The global market for HIV medications has grown drastically, and in 2023 it reached $31.7 Bn. Increased diagnosis rates and government campaigns to raise awareness about HIV management have had a positive impact on the HIV medicine market. The market's terrain is shifting due to an increase in generic competition. Reducing stigma, removing price obstacles, and ensuring that more people in developing countries have access to medical care are all necessary steps toward the future.

With more than 40% of the market for generic antiretroviral (ARV) medications, Aspen is the top provider in South Africa. They have played a significant role in expanding access to reasonably priced HIV treatment by providing superior generic substitutes for name-brand medications. Aspen produces a variety of pharmaceutical goods, including ARVs, at its four manufacturing plants in South Africa. This capacity for domestic manufacture lessens reliance on imports and helps to guarantee a steady supply of HIV medications.

Market Dynamics

Market Growth Drivers:

High prevalence of HIV/ AIDS: With millions of people infected, South Africa has one of the highest rates of HIV prevalence worldwide. HIV medications are in high demand due to this large patient population, propelling market expansion. In 2021, 78% of people in South Africa were on antiretroviral treatment.

Technological Developments: The advent of novel antiretroviral medications and formulations with enhanced safety, convenience, and efficacy can propel market expansion. The creation of long-acting injectable medications and advancements in medication delivery technologies could fuel market growth.

Collaborations and Partnerships: Working together, government agencies, pharmaceutical firms, nonprofits, and other interested parties solve issues around HIV/ AIDS treatment effectively and increase medication accessibility. Collaborations with foreign organizations and public-private partnerships make introducing innovative medications and treatment plans easier for the South African market.

Market Restraints:

Affordability Hurdles: Many South Africans, especially those from low-income households, may find it difficult to receive treatment due to the high cost of HIV medications. Inability to pay for the drugs, potential customers may be discouraged from entering the market.

Regulatory Obstacles: Pharmaceutical companies seeking to market HIV medications in South Africa may face regulatory difficulties, including drug approval and registration.

Intellectual Property Issues: Patent protection and intellectual property rights may have an impact on South Africa's capacity to obtain reasonably priced generic HIV medications. Patent-holding pharmaceutical companies may demand exorbitant costs for HIV treatments, which makes it challenging for generic producers to enter the market and provide more affordable options.

Healthcare Policies and Regulatory Landscape

The regulatory body in charge of approving pharmaceuticals in the nation is the South African Health Products Regulatory Authority, or SAHPRA. The applicant company has to produce the product dossier, which is regarded as a legal contract that must be approved by the Medicines Control Council (MCC). This is supported by the medicine's Certificate of Registration, which also functions as a sales permission. Any modifications the business makes after registering require MCC approval. Timelines may be further prolonged because SAHPRA has fewer resources than wealthier nations.

Competitive Landscape

Key Players:

- Aspen Pharmacare

- Adcock Ingram

- Gilead Sciences

- ViiV Healthcare

- Boehringer Ingelheim International GmbH

- Janssen Pharmaceuticals

- Merck & Co.

- Bristol-Myers Squibb

- AbbVie Inc.

- F. Hoffmann-La Roche Ltd

- Novartis

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

HIV Drugs Market Segmentation

By Drug Class

- Integrase Inhibitors

- Non- Nucleoside Reverse Transcriptase Inhibitors (NRTIs)

- Combination HIV Medicines

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

UAE Congestive Heart Failure Therapeutics Market Analysis

Pharmaceuticals

India Head and Neck Cancer Therapeutics Market Analysis

Pharmaceuticals

Saudi Arabia T-Cell Lymphoma Market Analysis

Related reports (by geography)

Pharmaceuticals

South Africa Human Insulin Drugs Market Analysis

Pharmaceuticals