Pharmaceuticals

South Africa Cardiovascular Drugs Market Analysis

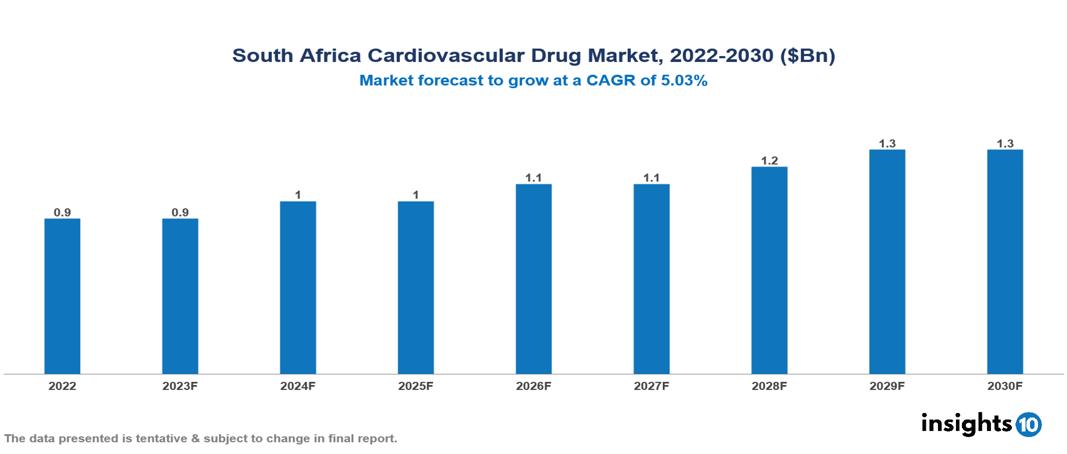

South Africa Cardiovascular Drug Market is at around $0.9 Bn in 2022 and is projected to reach $1.3 Bn in 2030, exhibiting a CAGR of 5.03% during the forecast period. The market is expanding as a result of the rise in research and development, government initiatives, and the burden of cardiovascular diseases. The market is dominated by key players like Aspen Pharmacare, Adcock Ingram, Cipla Medpro, Bristol-Myers Squibb Co., F. Hoffman-La Roche, Pfizer Inc., Astra Zeneca, Merck & Co., Sanofi, Novartis, and GSK.

Buy Now

South Africa Cardiovascular Drug Market Executive Summary

South Africa Cardiovascular Drug Market is at around $0.9 Bn in 2022 and is projected to reach $1.3 Bn in 2030, exhibiting a CAGR of 5.03% during the forecast period.

Heart and blood vessel conditions are collectively referred to as cardiovascular diseases. These comprise deep vein thrombosis, pulmonary embolism, congenital heart disease, peripheral artery disease, rheumatic heart disease, and coronary heart disease. The three main groups of drugs used to treat heart-related problems are ACE inhibitors (like ramipril), antiarrhythmics (like amiodarone), and angiotensin-II antagonists (like losartan).

Rising rates of heart disease and growing healthcare access initiatives are fueling a demand increase in the cardiovascular medicine market in South Africa. Notably, local firms like Aspen are driving the generics market, putting global behemoths up against fierce competition. The future of the market is dependent on several factors, including innovation, affordability, and the effect of government laws, all of which are critical in determining the cost and accessibility of the sector.

Revenues from pharmaceuticals climbed dramatically during the last 20 years, surpassing $138.33 Bn globally in 2022. With the introduction of new technologies and more economical and effective manufacturing techniques, the pharmaceutical industry has undergone a significant transformation. The industry's growing influx of capital has also contributed to the success of the company.

In South Africa, Aspen has the biggest market share for generic cardiovascular medications and provides reasonably priced substitutes for numerous name-brand medications. Their robust generics portfolio addresses a range of cardiovascular health therapeutic areas, such as antihypertensives like atenolol, lisinopril, and amlodipine, and cholesterol-lowering medications like simvastatin and atorvastatin.

Market Dynamics

Market Growth Drivers:

Increasing Prevalence of Cardiovascular Diseases: Stress, poor diets, and sedentary lifestyles are all contributing factors to the rise in cardiovascular diseases, in turn propelling the market growth.

Government Initiatives: To increase access to healthcare, the South African government has put in place several programs, such as the Chronic Disease Management Program and the Essential Medicines List (EML). These programs offer financial aid and assistance for the acquisition of necessary pharmaceuticals, such as heart medicines.

Research and Technology Development: The development of cardiovascular drugs is aided by ongoing research and technology developments, which fuel market expansion.

Market Restraints:

Regulatory Hurdles: Tight regulations and approval procedures may provide a serious obstacle to the market for cardiovascular drugs. Getting authorization for brand-new medications or even changes to already approved ones may be a costly and time-consuming procedure.

Generic Competition: As branded cardiovascular medications' patents expire, generic alternatives may become more competitive. This may affect the original pharmaceutical company's profits and market share.

Strict Guidelines for Clinical Trials: Getting a medicine approved requires meeting the strict requirements imposed for clinical studies. However, meeting these requirements can be difficult, and it could cause delays and higher expenses.

Healthcare Policies and Regulatory Landscape

South African Health Products Regulatory Authority, or SAHPRA, is the regulatory agency that oversees the approval of drugs in the country. The product dossier, which is considered a formal contract, was put together by the applicant company and needs to be approved by the Medicines Control Council (MCC). This is verified by the medicine's Certificate of Registration, which also serves as a sales authorization. The MCC must approve any changes the company makes after registering. SAHPRA has fewer resources in comparison to wealthier countries therefore timelines may be further extended.

Competitive Landscape

Key Players:

- Aspen Pharmacare

- Adcock Ingram

- Cipla Medpro

- Bristol-Myers Squibb Co.

- F. Hoffman-La Roche

- Pfizer Inc.

- Astra Zeneca

- Merck & Co.

- Sanofi

- Novartis

- GSK

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

South Africa Cardiovascular Drug Market Segmentation

By Drug Type

- Cephalosporins

- Antihypertensive

- Antihyperlipidemic

- Anticoagulants

- Antiplatelet Drug

- Others

By Disease Indication

- Hypertension

- Hyperlipidemia

- Coronary Artery Disease

- Arrhythmia

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

UK Nanomedicine Market Analysis

Pharmaceuticals

UAE Seasonal Flu Vaccine Market Analysis

Pharmaceuticals

US Medical Information Market Analysis

Related reports (by geography)

Pharmaceuticals

South Africa Pharmaceutical Drugs Delivery Market Analysis

Pharmaceuticals

South Africa Lipid Lowering Drugs Market Analysis

Pharmaceuticals

South Africa Microspheres Market Analysis

Pharmaceuticals