Pharmaceuticals

South Africa Acute Lymphocytic Leukemia (ALL) Therapeutics Market Analysis

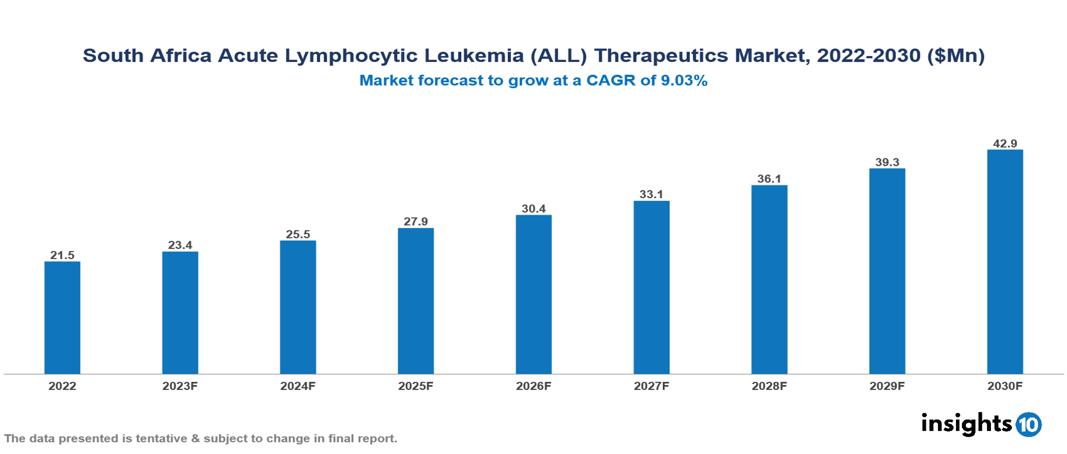

The South Africa Acute Lymphocytic Leukemia (ALL) Therapeutics Market was valued at US $21 Mn in 2022, and is predicted to grow at (CAGR) of 9.03% from 2023 to 2030, to US $43 Mn by 2030. The key drivers of this industry include a surge in the incidence of acute lymphocytic leukemia cases, rising investment, increased government initiatives, and other factors. The industry is primarily dominated by players such as Spectrum Pharmaceutical, AbbVie, Pfizer, AstraZeneca, Novartis and other players

Buy Now

South Africa Acute Lymphocytic Leukemia (ALL) Therapeutics Market Analysis

The South Africa Acute Lymphocytic Leukemia (ALL) Therapeutics Market is at around US $21 Mn in 2022 and is projected to reach US $43 Mn in 2030, exhibiting a CAGR of 9.03% during the forecast period.

Acute Lymphocytic Leukemia (ALL) is a type of cancer that is identified by the rapid multiplication of immature white blood cells, known as lymphoblasts, within the bone marrow. This condition is typically triggered by a genetic mutation affecting developing lymphocytes, resulting in the buildup of undifferentiated lymphoid cells. Symptoms observed include frequent infections, swollen lymph nodes, weight loss, bone pain, fever, and other indicators. Treating ALL involves an extensive treatment plan lasting months or even years, incorporating various therapies like chemotherapy, targeted treatments, CAR-T cell immunotherapy, and, in extreme conditions, stem cell transplantation. These advancements in treatment substantially enhance the chances of a cure, often achieving success rates of up to 80% in adults and children.

ALL incidence rates are estimated at approximately 1.5–2/1,00,000 cases under 15 years of age in South African children. ALL accounts for approximately 76% of all diagnosed childhood leukemia cases. The market is therefore driven by major factors like the surge in the incidence of ALL cases, rising investment, and increased government initiatives in the therapeutics industry. However, conditions such as limited healthcare infrastructure in South Africa, treatment non-compliance among the diagnosed, and others hinder the growth and potential of the market.

Market Dynamics

Market Growth Drivers

Increased cases of ALL: ALL contributes to about 76% of all childhood leukemia cases in South Africa. Epidemiological studies suggest that the annual incidence of ALL ranges from 1.5–2/1,00,000 cases in children under the age of 15 years. These estimates are higher than in other African countries, and the rising number of cases could potentially drive the growth of the market.

Increased government initiatives: The government has introduced the National Cancer Control Plan, which strives to offer a comprehensive approach for prevention, treatment, and monitoring of leukemia to all citizens, encompassing accessibility to vital cancer treatments such as ALL chemotherapy. It has also launched the Childhood Cancer Registry, aiming for a holistic approach to ALL treatments, fueling market expansion.

Government funding: The National Health Insurance (NIH) aims to offer Universal Health Coverage (UHC), reducing financial hardships. The government's focus on initiatives like the NHI, enhancing capabilities, research activities, and partnering with patient advocacy groups is expected to drive the market's growth and expansion.

Market Restraints

Limited healthcare infrastructure: There are very few dedicated oncology treatment centres. Discrepancies in the allocation of specialized equipment and treatment facilities result in unequal access to precise diagnoses and efficient therapy, especially for advanced cases of ALL

Lack of human resources: Insufficient availability of paediatric oncologists and haematologists, notably in rural regions, limits the accessibility of comprehensive care and treatment choices for ALL patients.

High cost: There are challenges concerning the accessibility and affordability of laboratory tests. Numerous families face difficulties affording the required laboratory studies necessary for optimal risk-oriented therapy, potentially surpassing the financial means of many patients and the limits of their healthcare coverage as the scope of ALL treatment is still evolving.

Regulatory compliance: The process of getting approvals and licensure for therapeutics is very complex, which results in the delay of new therapies impacting treatment options and is a restraining factor.

Healthcare Policies and Regulatory Landscape

South Africa's healthcare policies and regulations are overseen by the Department of Health (DoH) and primarily governed by the Medicines and Related Substances Act and the Pharmacy Act. The South African Health Products Regulatory Authority (SAHPRA) is tasked with overseeing the regulation of medicines, medical devices, and diagnostics within South Africa.

Obtaining a license for healthcare products in South Africa necessitates adherence to regulations established by SAHPRA. To register pharmaceuticals and medical devices, companies must acquire authorization for marketing and registration from SAHPRA. The registration entails submitting technical and scientific data to validate the product's safety, quality, and efficacy. Moreover, companies must have a local importer or distributor for product liability, with some low-risk products potentially exempt from registration.

Both the public and private healthcare sectors in the country offer diverse opportunities for companies operating within the healthcare industry.

Competitive Landscape

Key Players

- Pfizer

- F. Hoffman La Roche Ltd

- Aspen Pharmacare

- Novartis

- Zuelling Pharma

- AbbVie

- Sanofi-Aventis

- Bayer

- AstraZeneca

- Spectrum Pharmaceuticals

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

South Africa Acute Lymphocytic Leukemia (ALL) Therapeutics Market Segmentation

By Type

- Paediatrics

- Adults

By Drug

- Hyper CVAD regimen

- Linker Regimen

- Nucleoside Metabolic Inhibitors

- Targeted drugs and Immunotherapy

- CALGB 811 Regimen

By Cell

- B Cell ALL

- T Cell ALL

- Philadelphia Chromosome

By Therapy

- Chemotherapy

- Targeted therapy

- Radiation therapy

- Stem Cell Transplantation

By Distribution channel

- Hospital Pharmacy

- Retail Pharmacy

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Spain Anemia Therapeutics Market Analysis

Pharmaceuticals

Philippines Pediatric Healthcare Market Analysis

Pharmaceuticals

India Exosome Research Market Analysis

Related reports (by geography)

Pharmaceuticals

South Africa Dermatology Drugs Market Analysis

Pharmaceuticals

South Africa Opioid Drugs Market Analysis

Pharmaceuticals