Pharmaceuticals

Singapore HIV Therapeutics Market Analysis

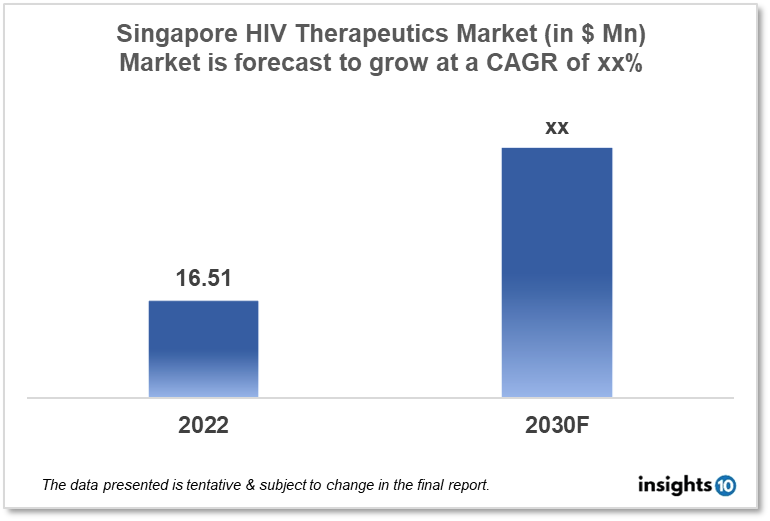

By 2030, it is anticipated that the Singapore HIV therapeutics market will reach a value of $xx Mn from $16.51 Mn in 2022, growing at a CAGR of xx% during 2022-2030. The market is primarily dominated by local players such as Invida Group, Tanax Pharmaceuticals, and Aslan Pharmaceuticals. The market is driven by cutting-edge healthcare infrastructure, the prevalence of HIV infections, and treatment for HIV. The HIV therapeutics market in Singapore is segmented by type, product, and geography, end user, and distribution channel.

Buy Now

Singapore HIV Therapeutics Market Analysis Summary

By 2030, it is anticipated that the Singapore HIV therapeutics market will reach a value of $xx Mn from $16.51 Mn in 2022, growing at a CAGR of xx% during 2022-2030.

The Southeast Asian Island nation of Singapore is located off the southernmost point of the Malay Peninsula. Singapore's adult HIV/AIDS prevalence in 2021 was 0.2%, placing it in 104th globally. According to the most recent WHO data, 18 HIV/AIDS deaths—or 0.08% of all deaths—occurred in Singapore in 2020. Singapore is ranked 145th in the world with an age-adjusted death rate of 0.20 per 100,000 people.

The expected share of GDP for healthcare in Singapore, which includes both public and private spending, is 5.9%, with a potential increase to 9% by 2029. Given the aging population and a trend toward earlier diagnosis of chronic conditions, close monitoring, and follow-up, rising government healthcare spending and local population use of healthcare services are both major contributors to this increase.

Market Dynamics

Market Growth Drivers

According to the World Health Organization (WHO), Singapore's healthcare system ranks 6th globally and provides the 4th best healthcare infrastructure in the world. Singapore has achieved world-class standards in healthcare. Asia's top healthcare system is available there, and it also serves as the region's healthcare and medical hub. The HIV therapeutics market in Singapore may be driven by this factor for new entrants.

Market Restraints

All locally sold goods and rendered services are subject to a 7% goods and services tax (GST). This may discourage new players from entering Singapore's HIV therapeutics market.

Competitive Landscape

Key Players

- Aslan Pharmaceuticals (SGP)

- Tanax Pharmaceuticals (SGP)

- Invida Group (SGP)

- Trikaal Pharmacy (SGP)

- Gilead Sciences

- ViiV Healthcare

- Merck & Co.

- Pfizer

- AstraZeneca

- Novartis

- GlaxoSmithKline

- Johnson & Johnson

Healthcare Regulations and Reimbursement Policies

In Singapore, the regulatory body responsible for the approval of HIV therapeutics is the Health Sciences Authority (HSA). The HSA is the federal agency in charge of overseeing the use of drugs and medical equipment in the healthcare industry. Drugs are evaluated by the HSA for their quality, safety, and efficacy before being approved for use in Singapore. Additionally, the HSA keeps an eye on the efficacy and safety of medicines that have already been approved and made available to patients, and it has the authority to restrict or withdraw their use if they are discovered to be unsafe or ineffective.

In Singapore, MediShield Life—a required government-run health insurance program—provides reimbursement for HIV therapeutics. Numerous medical procedures are covered by MediShield Life, including the price of HIV medications. The type of drug being used and the individual's plan determine how much coverage is provided.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

HIV Therapeutics Segmentation

By Types (Revenue, USD Billion):

- Nucleoside-Analog Reverse Transcriptase Inhibitors (NRTIs)

- Coreceptor Antagonists

- Entry and Fusion Inhibitors

- Integrase Inhibitors

- Protease Inhibitors (PIs)

- Non-Nucleoside Reverse Transcriptase Inhibitors (NNRTIs)

By Distribution Channel (Revenue, USD Billion):

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Philippines Coenzyme Q10 Market Analysis

Pharmaceuticals

Kenya Infectious Disease Drugs Market Analysis

Pharmaceuticals

Malaysia Clinical Nutrition for Cancer Care Market Analysis

Related reports (by geography)

Pharmaceuticals

Singapore Varicella Vaccine Market Analysis

Digital Health

Singapore eHealth Market Analysis

Pharmaceuticals

Singapore Cord Blood Banking Service Market Analysis

Pharmaceuticals