Pharmaceuticals

Saudi Arabia Oncology Therapeutics Market Analysis

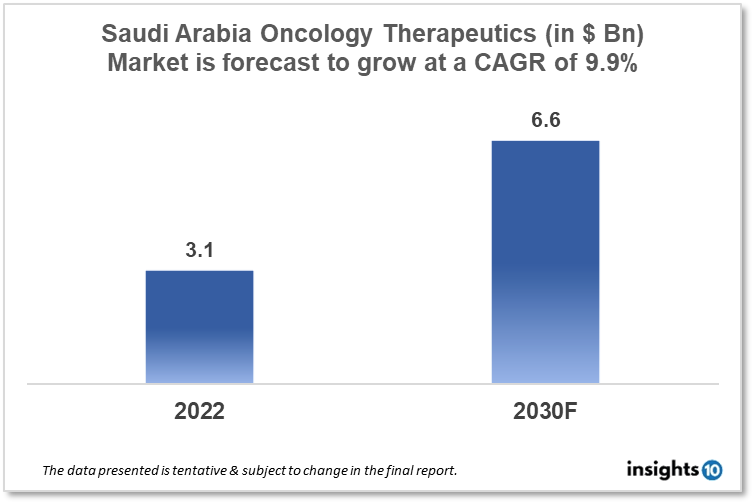

By 2030, it is anticipated that the Saudi Arabia Oncology Therapeutics Market will reach a value of $6.6 Bn from $3.3 Bn in 2022, growing at a CAGR of 9.9% during 2022-2030. The Oncology Therapeutics Market in Saudi Arabia is dominated by a few domestic pharmaceutical companies such as Tabuk Pharmaceuticals, Jamjoom Pharma, and SPIMACO. The Oncology Therapeutics Market in Saudi Arabia is segmented into different types of cancer and different therapy type. The major risk factors associated with cancer are diet, alcohol, tobacco, air pollution, and physical inactivity. The demand for Saudi Arabia Oncology Therapeutics is increasing on account of the rise in initiatives taken by the Government of the country.

Buy Now

Saudi Arabia Oncology Therapeutics Market Analysis Summary

By 2030, it is anticipated that the Saudi Arabia Oncology Therapeutics Market will reach a value of $6.6 Bn from $3.3 Bn in 2022, growing at a CAGR of 9.9% during 2022-30.

The Gulf region's largest country is the Kingdom of Saudi Arabia. With an increasing cancer burden both internationally and locally, as well as a young population with an expanding life expectancy, the hurdles to providing optimal healthcare are significant. Saudi Arabia is a Middle Eastern country with a high revenue that borders the Persian Gulf and the Red Sea. The Ministry of Health (MOH) regulates the Saudi healthcare system, and oncology services are available in a variety of public and private facilities around the kingdom. The SLCA has created a set of guidelines appropriate to our patient population in collaboration with the Saudi National Cancer Center, encompassing patient characteristics, disease biology, and the practice environment of systemic therapy for cancer.

The Saudi Cancer Registry (SCR), a population-based registry, was created in 1992 by the Ministry of Health (MOH). SCR was transferred to the Saudi Health Council's Department of National Registries in the National Center for Health Information in 2014. According to the most current SCR cancer incidence data, the total number of newly diagnosed cancer cases reported to the Saudi Cancer Registry (SCR) in 2016 was 17,602. Saudi Arabia's government spent 6.2% of its GDP on healthcare in 2020.

Market Dynamics

Market Growth Drivers Analysis

The Saudi Ministry of Health has consistently taken steps in cancer prevention, diagnosis, and treatment. Breast cancer, colorectal cancer, and thyroid cancer are the most frequent cancers in the general population. Oncology care is provided throughout the Kingdom by multiple public sectors, including the Ministry of Health, the Ministry of Higher Education through university hospitals, and specialised hospitals serving various governmental sectors (e.g., the Military, the National Guard Ministry, Arabian American Oil Company (ARAMCO), and the Ministry of Interior). These aspects could boost Saudi Arabia's Oncology Therapeutics Market.

Market restraints

Over the previous two years, Saudi Arabia's chemotherapy scarcity has worsened. As a result of the limited cancer drug supply, a Mexican court issued an injunction to the Attorney General's Office in July 2021. The country's new public healthcare system of integration has delayed patients' access to timely diagnosis and treatment. Patients registered in INSABI receive only partial government assistance; families must pay for drugs such as cytarabine, cyclophosphamide, etoposide, and doxorubicin, among others, that are unavailable. These factors may deter new entrants into the Saudi Arabia Oncology Therapeutics Market.

Competitive Landscape

Key Players

- Tabuk Pharmaceuticals: Tabuk Pharmaceuticals is a Saudi Arabian pharmaceutical company that develops and manufactures a wide range of drugs, including oncology therapeutics. The company's oncology portfolio includes treatments for breast cancer, colorectal cancer, and lung cancer, among others

- Jamjoom Pharma: Jamjoom Pharma is a Saudi Arabian pharmaceutical company that specializes in the development and commercialization of generic drugs, including oncology therapeutics. The company's oncology portfolio includes treatments for breast cancer, colorectal cancer, and prostate cancer, among others

- SPIMACO: SPIMACO is a Saudi Arabian pharmaceutical company that develops and manufactures a range of drugs, including oncology therapeutics. The company's oncology portfolio includes treatments for breast cancer, lung cancer, and colorectal cancer, among others

- Tabuk Oncology: Tabuk Oncology is a subsidiary of Tabuk Pharmaceuticals that focuses on the development and commercialization of oncology therapeutics. The company's oncology portfolio includes treatments for breast cancer, lung cancer, and colorectal cancer, among others

- National Company for Pharmaceutical Industry: The National Company for Pharmaceutical Industry is a Saudi Arabian pharmaceutical company that develops and manufactures a range of drugs, including oncology therapeutics

Notable Recent Deals

October 2022: In conjunction with Saudi Telecom Company, the Kingdom's Ministry of Health established the Middle East's first oncology e-platform at the Seha Virtual Hospital's headquarters. The purpose is to improve the quality of healthcare given to patients in accordance with Vision 2030 aims. The platform will be governed by a council of Saudi specialists who will convene to discuss patients with cancers.

Healthcare Policies and Reimbursement Scenarios

The Ministry of Health (MOH) regulates the Saudi healthcare system, and oncology services are available in a variety of public and private facilities around the kingdom. Aside from these rules, the Saudi Food and Drug Authority (SFDA) is in charge of overseeing the approval and usage of cancer medications and therapies in the nation. Individuals and businesses in Saudi Arabia can get health insurance through the Saudi Arabian Cooperative Insurance Company (SAICO). Nongovernmental charitable organisations assist with costs that the government may not cover. These non-profit organisations and groups should be recognised for their contributions to improving the quality of life for lung cancer sufferers. King Faisal Specialist Hospitals and Research Centers (KFSH&RC) have locations in Riyadh, Jeddah, and a new branch in Kuwait. All cancer care facilities are freely accessible to citizens.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Oncology Therapeutics Segmentation

By Application (Revenue, USD Billion):

- Blood Cancer

- ?Colorectal Cancer

- Gastrointestinal Cancer

- Gynaecologic Cancer

- Breast Cancer

- Lung Cancer

- Prostate Cancer

- ?Others

By Drugs (Revenue, USD Billion):

- Revlimid

- Avastin

- Herceptin

- Rituxan

- Opdivo

- Gleevec

- Velcade

- Imbruvica

- Ibrance

- Zytiga

- Alimta

- Xtandi

- Tarceva

- Perjeta

- Temodar

- Others

By Therapy (Revenue, USD Billion):

- Chemotherapy

- Targeted Therapy

- Immunotherapy

- Hormonal Therapy

- Others

By Route of Administration (Revenue, USD Billion):

- Oral

- Parenteral

- Others

By Distribution Channel (Revenue, USD Billion):

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- ?Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

By 2030, it is anticipated that the Saudi Arabia Oncology Therapeutics market will reach a value of $6.6 Bn from $3.3 Bn in 2022, growing at a CAGR of 9.9% during 2022-2030.

In Saudi Arabia, the healthcare system is regulated by the Ministry of Health (MOH). The Saudi Arabian Cooperative Insurance Company (SAICO) provides health insurance to individuals and companies in the country.

The Oncology Therapeutics Market in Saudi Arabia is dominated by a few domestic pharmaceutical companies such as Tabuk Pharmaceuticals, Jamjoom Pharma, and SPIMACO.

Related reports (by category)

Pharmaceuticals

UAE Lymphoma Therapeutics Market Analysis

Pharmaceuticals

Mexico Enzyme Inhibitors Market Analysis

Pharmaceuticals

Kenya Human Insulin Drugs Market Analysis

Related reports (by geography)

Medical Devices

Saudi Arabia MRI Market Analysis

Medical Devices

Saudi Arabia Bio-Implant Market Analysis

Pharmaceuticals