OTC & Nutraceuticals

Saudi Arabia Herbal Supplements Market Report

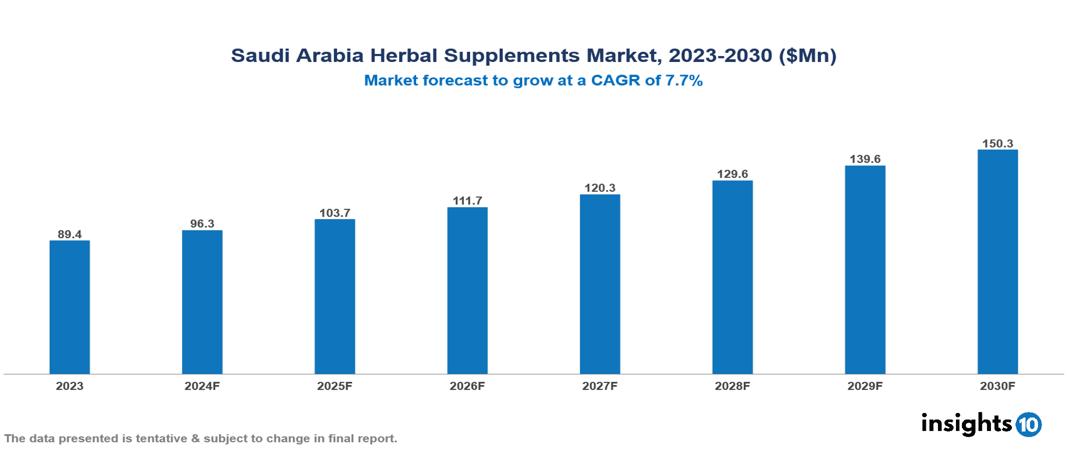

The Saudi Arabia Herbal Supplements Market was valued at $89.42 Mn in 2023 and is predicted to grow at a CAGR of 7.7% from 2023 to 2030, to $150.30 Mn by 2030. The key drivers of this industry include health consciousness, preventive healthcare trends, and the young population. The industry is primarily dominated by players such as Himalaya Wellness, NOW Foods, Botanic Supplements, and Dabur among others.

Buy Now

Saudi Arabia Herbal Supplements Market Executive Summary

The Saudi Arabia Herbal Supplements Market was valued at $89.42 Mn in 2023 and is predicted to grow at a CAGR of 7.7% from 2023 to 2030, to $150.30 Mn by 2030.

Herbal supplements, also known as botanicals, are dietary supplements that contain one or more herbs. These products, which include herbal, botanical, or phytomedicines, are derived from plants or botanicals to promote health or treat illnesses. Herbal supplements are intended specifically for internal use and are commonly available in solid forms such as capsules, pills, tablets, and lozenges, but can also be found in liquid or powder forms. Some popular herbal supplements include Echinacea, Garlic, Ginkgo, Ginseng, St. John's Wort, Saw Palmetto, and Valerian.

In Saudi Arabia, the use of herbal medicine is quite prevalent, with studies indicating a range from 10.3% to 75.0%. About 15% of Saudi students reported using herbal medicine to prevent respiratory infections, and 55.5% of students agreed to use foods and herbs as supplements to prevent infections and boost immunity in 2022. The market is driven by significant factors like health consciousness, preventive healthcare trends, and the growing young population. However, quality and safety concerns, cost issues, and lack of scientific evidence restrict the growth and potential of the market.

Prominent players in this field include Himalaya Wellness, NOW Foods, Botanic Supplements, and Dabur among others.

Market Dynamics

Market Growth Drivers

Health Consciousness: Rising awareness and focus on health and wellness among the Saudi population are boosting the demand for natural and herbal supplements. This trend drives market growth as more consumers seek healthier, natural alternatives to support their well-being.

Preventive Healthcare Trend: A substantial segment of the population, including 55.5% of students, utilizes foods and herbs as supplements to prevent infections and boost immunity. This highlights a growing trend towards preventive healthcare, driving demand for herbal supplements in Saudi Arabia.

Growing Young Population: In 2023, Saudi Arabia's population reached 32.2 Mn, with 42% being foreign nationals and 63% of Saudis under the age of 30. This youthful and diverse demographic drives demand for herbal supplements, as younger generations are more inclined to adopt health trends and natural wellness products.

Market Restraints

Quality and Safety Concerns: Maintaining consistent quality and authenticity of herbal supplements can be difficult, which may result in consumer skepticism and potential health risks. This challenge restrains market growth in Saudi Arabia by undermining consumer confidence in herbal products.

Cost Issues: Most people find expensive herbal supplements unaffordable, which hampers market growth. This financial barrier limits the widespread adoption and expansion of the herbal supplement market in Saudi Arabia.

Lack of Scientific Evidence: The scarcity of clinical research and scientific validation for many herbal supplements can discourage healthcare professionals and consumers from fully embracing these products. This lack of evidence acts as a restraint on the herbal supplement market in Saudi Arabia by reducing confidence in their effectiveness and safety.

Regulatory Landscape and Reimbursement Scenario

The Saudi Food and Drug Authority (SFDA) oversees the regulation of herbal and health products in Saudi Arabia. All herbal products must undergo registration with the SFDA before they can be sold in the country. The SFDA sets out detailed guidelines and requirements for the registration process, which include specific data requirements for submitting product information. As of now, the Saudi Arabian government has not established a formal policy for reimbursing herbal supplements. The existing regulatory framework in Saudi Arabia does not include provisions for reimbursing the costs of herbal supplements.

Competitive Landscape

Key Players

Here are some of the major key players in the Saudi Arabia Herbal Supplement Market:

- Himalaya Wellness

- NOW Foods

- Botanic Supplements

- Dabur

- Hishimo Pharmaceuticals Pvt. Ltd

1. Executive Summary

1.1 Product Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Government Regulation in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel and Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

6. Methodology and Scope

Saudi Arabia Herbal Supplements Market Segmentation

By Product Form

- Tablet

- Capsule

- Powder

- Others

By Application

- Immunity

- General Wellness

- Specific Health Condition

By Distribution Channel

- Pharmacies

- Supermarket/Hypermarket

- Online

- Specialty Stores

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

OTC & Nutraceuticals

Lebanon Over The Counter (OTC) Pharmaceuticals Market Analysis

OTC & Nutraceuticals

Finland Over The Counter (OTC) Analgesics Market Analysis

OTC & Nutraceuticals

Lebanon Over The Counter (OTC) Analgesics Market Analysis

Related reports (by geography)

Pharmaceuticals

Saudi Arabia Sarcoma Drugs Market Analysis

Pharmaceuticals