Healthcare Services

Saudi Arabia Healthcare Insurance Market Analysis

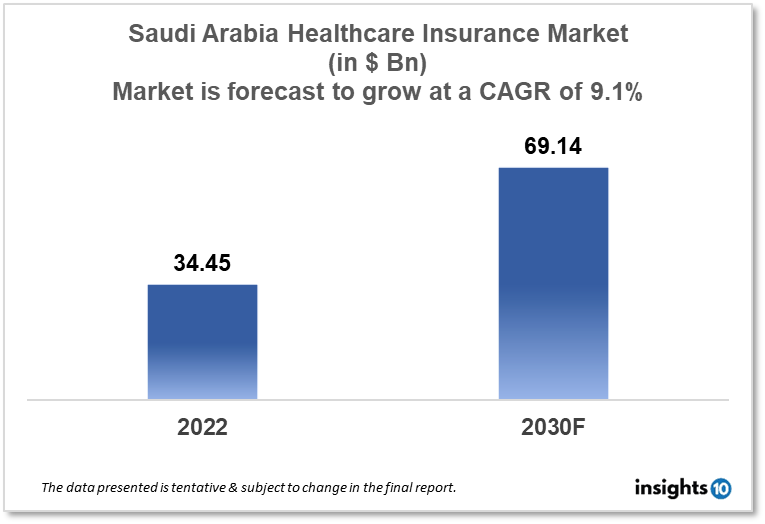

Saudi Arabia's healthcare insurance market is projected to grow from $34.45 Bn in 2022 to $69.14 Bn by 2030, registering a CAGR of 9.1% during the forecast period of 2022-30. The main factors driving the growth would be mandatory health insurance schemes, growing healthcare infrastructure, increasing prevalence of non-communicable diseases, and government support. The market is segmented by component, provider, coverage, by health insurance plans and end-user. Some of the major players include Tawuniya, MedGulf, Saudi Arabian Cooperative Insurance Company (SAICO), Al Rajhi Takaful and Bupa Arabia.

Buy Now

Saudi Arabia Healthcare Insurance Market Executive Summary

Saudi Arabia's healthcare insurance market is projected to grow from $34.45 Bn in 2022 to $69.14 Bn by 2030, registering a CAGR of 9.1% during the forecast period of 2022-30. Saudi Arabia spent $1,316.26, or 5.69% of its GDP, on public healthcare in 2019. The Saudi government continues to place a strong priority on healthcare, and there are numerous prospects for expansion in this high-potential area.

The healthcare system in Saudi Arabia is well-developed and includes both governmental and private healthcare providers. Yet, a growing population, shifting demographics, and an increase in the burden of non-communicable diseases are all contributing to an increase in the need for high-quality healthcare services.

In Saudi Arabia, health insurance is designed to lessen the financial strain that comes with having to pay high medical expenditures as a result of an unplanned illness or injury. The Saudi Arabian government also requires that all citizens and foreigners have access to health care. The government began adopting the required unified health insurance policy in July 2016, with the system totally in place since 2017. All private sector businesses are required to offer health insurance to their employees and their dependents, which includes their spouses, male children below the age of 25 and unmarried daughters.

Market Dynamics

Market Growth Drivers

The Saudi Arabia healthcare Insurance market is expected to be driven by factors such as:

- Mandatory health insurance scheme- The country's health insurance penetration has expanded dramatically as a result of the mandatory health insurance program for foreigners employed in the private sector and their dependents. The need for health insurance in Saudi Arabia is anticipated to increase further as the country's population continues to expand

- Growing healthcare infrastructure- The Saudi Arabian government has made considerable expenditures on the country's healthcare infrastructure, building new hospitals and clinics and enlarging already-existing ones. As a result, there are now more high-quality healthcare services available, which is likely to raise demand for health insurance

- Increasing prevalence of non-communicable diseases- The prevalence of chronic conditions like cancer, diabetes and heart disease in Saudi Arabia is rising. Some disorders require continuous therapy and care, which can be costly. Families and individuals can manage the financial burden of chronic conditions with the support of healthcare insurance

- Government support- The government of Saudi Arabia has launched many efforts to promote the expansion of the health insurance market, including the national e-health plan, which aims to improve access to healthcare services and encourage the use of technology in the delivery of healthcare services. The country's healthcare insurance sector is expected to increase with the government support

Market Restraints

The following factors are expected to limit the growth of the healthcare insurance market in Saudi Arabia:

- Limited access to healthcare services- Saudi Arabia has made improvements in its healthcare infrastructure, however, some regions of the country still have inadequate access to healthcare services. This may discourage people from purchasing health insurance in these regions since they may not understand the benefit of paying for a service they cannot use

- Limited regulation- The Saudi Arabian healthcare insurance sector is still in its early phases of growth and is only loosely regulated. The market's potential expansion may be constrained as a result of varied pricing, coverage, and benefits among insurance companies

- Limited coverage and benefits- Several Saudi Arabian healthcare insurance plans have restricted benefits and coverage, which may make them less alluring to individuals and families. For lower-income populations, who might not be able to buy more comprehensive insurance, this is especially the case

Competitive Landscape

Key Players

- Tawuniya (SAU)- Healthcare insurance is one of the several insurance products offered by Tawuniya, a Saudi Arabian insurance provider. Individual, family, and corporate health insurance plans are all available through the organisation

- MedGulf (SAU)- One of the biggest insurance providers in the Kingdom is MEDGULF, which offers a wide range of cooperative services for health, auto, property, and other insurance and reinsurance

- Saudi Arabian Cooperative Insurance Company (SAICO)(SAU)- In Saudi Arabia, SAICO was the first insurance provider to provide health insurance. The business offers people, families, and employers a variety of health insurance options

- Al Rajhi Takaful (SAU)- Al Rajhi Takaful is transforming the way one experience insurance in Saudi Arabia. It is founded on the fundamental ideals of ethics and justice, and they forbid unjustified commercial enrichment at the expense of clients. These concepts are what make Al Rajhi Takaful the best option for all facets of Saudi Arabian society

- Bupa Arabia- Bupa Arabia is a partnership between the Nazer Group, a Saudi Arabian business, and Bupa, a UK-based healthcare service. The business offers people, families, and employers a variety of health insurance options

Notable Deals

April 2019- Tawuniya has struck the first deal of its kind in the Saudi insurance sector with Vitality Group, the worldwide leader in integrating wellness benefits with insurance products. With the help of this partnership, Tawuniya will pioneer Shared-Value Insurance across the Middle East and North Africa.

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Healthcare Insurance Market Segmentation

By Provider (Revenue, USD Billion):

It mainly includes healthcare insurance that provides safety against the increasing cost of medical treatments and in case of health emergencies such as critical illnesses. Hence, it is the best way to safeguard medical expenses.

- Public

- Private

By Coverage Type (Revenue, USD Billion):

In terms of sales and market share, it is anticipated to rule the market over the projection period. This is explained by a number of benefits provided by life insurance, including guaranteed death payout and permanent coverage. Additionally, investing in these kinds of plans enables working professionals to save taxes

- Life Insurance

- Term Insurance

By Health Insurance Plans (Revenue, USD Billion):

- Health Maintenance Organization (HMO)

- Preferred Provider Organization (PPO)

- Exclusive Provider Organization (EPO)

- Point of Service (POS)

- High Deductible Health Plan (HDHP)

By Demographics (Revenue, USD Billion):

- Minors

- Adults

- Seniors

There is a high prevalence of lifestyle disease in the adult population that can increase health risks in the future. The population is more prone to cardiac and other diseases that require hospitalization. Healthcare insurance plans for seniors are more of a necessity, especially in the case of retirement. Also, it carries various advantages such as no medical screening before buying plans, includes coverage of the outpatient department, and provides the benefit of fee annual checkups along with lifetime renewability.

By End-user (Revenue, USD Billion):

- Individuals

- ?Corporates

A large number of people buy individual health plans as they are also customizable. Also, it gives more control over deductibles, co-pays, and benefits limits and is not dependent on employment status.

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

Thailand Cancer Pain Management Market Analysis

Healthcare Services

Thailand Patient Support Programs (PSP) Market Analysis

Healthcare Services

India Healthcare Reimbursement Market Analysis

Related reports (by geography)

Medical Devices

Saudi Arabia Dental Caries Detectors Market Analysis

Pharmaceuticals

Saudi Arabia Coenzyme Q10 Market Analysis

Pharmaceuticals

Saudi Arabia Asthma Drugs Market Analysis

Pharmaceuticals