Medical Devices

Saudi Arabia ECG Equipments Market Analysis

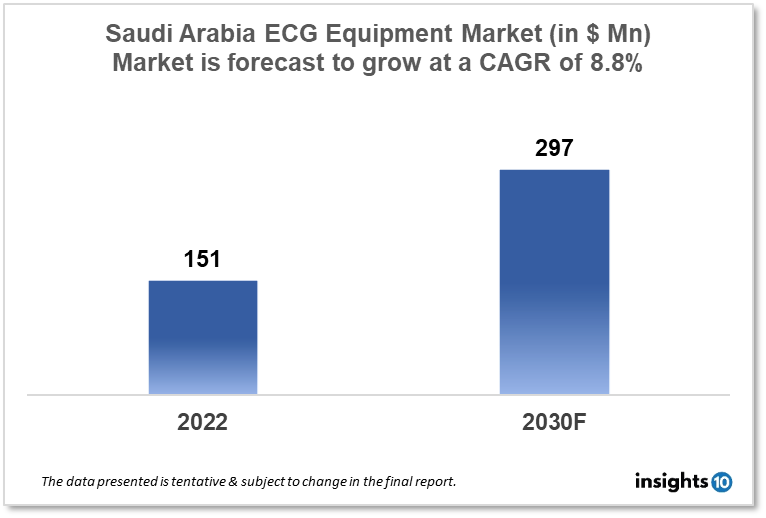

Saudi Arabia's ECG Equipment Market is expected to witness growth from $151 Mn in 2022 to $297 Mn in 2030 with a CAGR of 8.80% for the forecasted year 2022-30. The elderly population in Saudi Arabia is expanding and is more likely to develop heart disease and other chronic ailments, the growing geriatric population is predicted to raise demand for ECG equipment in the nation. The market is segmented by product type and by end user. Some key players in this market include Al Madar Medical, Aljeel Medical, Alhammad Medical, Johnson & Johnson, Philipps Healthcare, Medtronic, GE Healthcare, and Nihon Kohden.

Buy Now

Saudi Arabia ECG Equipment Healthcare Market Executive Analysis

Saudi Arabia's ECG Equipment Market is expected to witness growth from $151 Mn in 2022 to $297 Mn in 2030 with a CAGR of 8.80% for the forecasted year 2022-30. The budget for Saudi Arabia in 2023 is going to spend 4.5% less on healthcare than it did in 2022. Health expenditures will account for 5.5% of GDP in 2023. Men can anticipate living to an average age of 75.33 in Saudi Arabia, while women can anticipate living to an average age of 78.56. In 2020, out-of-pocket costs as a percentage of total health spending in Saudi Arabia were 16.5%.

In Saudi Arabia, cardiovascular disease accounts for 46% of fatalities. This is greater than the 31% average for the entire world. According to the Saudi Ministry of Health, there were 43,809 hospital admissions for heart attacks in the kingdom in 2021. 9.2 heart attacks occur in Saudi Arabian citizens for every 1,000 people. In Saudi Arabia, ECG equipment is frequently used to identify and track a variety of heart problems. A non-invasive medical gadget called an ECG records the electrical activity of the heart, giving important details about the rhythm and operation of the heart. To track changes in heart function and spot potential issues, healthcare experts utilize ECG equipment to continuously monitor the heart's activity. Patients who already have heart issues should pay particular attention to this. Before undergoing surgery, a patient's heart function is assessed using ECG equipment. This aids medical practitioners in determining the likelihood that the patient will experience difficulties during or following the surgery.

Market Dynamics

Market Growth Drivers

The elderly population in Saudi Arabia is expanding and is more likely to develop heart disease and other chronic ailments. Since healthcare providers need trustworthy diagnostic tools to identify and track heart issues in this population, the growing geriatric population is predicted to raise the demand for ECG equipment in the nation. Saudi Arabia has recently made significant investments in its healthcare system. Building additional hospitals and clinics, hiring more medical experts, and implementing new medical technologies are just a few of the steps the nation has started to increase access to healthcare. The need for ECG equipment is anticipated to rise as a result of the expanding healthcare infrastructure.

Market Restraints

In Saudi Arabia, the market for ECG equipment is already dominated by a number of well-known brands. It could be challenging for new rivals to get traction and expand their market share. ECG equipment can be expensive, especially for modern models that offer extra features and functionalities. This could limit the market for ECG equipment since certain healthcare providers would not be able to buy the most advanced devices.

Competitive Landscape

Key Players

- Al Madar Medical (SA)

- Aljeel Medical (SA)

- Alhammad medical (SA)

- Johnson & Johnson

- Medtronic

- Philipps Healthcare

- GE Healthcare

- Nihon Kohden

Recent Notable Deals

2022: Leading medical equipment manufacturer Mindray inked a contract in 2022 to provide the Saudi German Hospital (SGH) in Riyadh with its BeneHeart C Series ECG equipment. With this agreement, SGH would receive cutting-edge ECG technology to bolster its cardiac care offerings.

Healthcare Policies and Regulatory Landscape

In Saudi Arabia, The Saudi Food and Drug Authority (SFDA) is the regulatory body in charge of overseeing ECG equipment. It is in charge of registering and approving ECG devices for national use. All medical devices marketed and distributed in Saudi Arabia are required to register with the SFDA and abide by its rules. To control the import, production, and distribution of medical devices in the nation, the SFDA introduced the Medical Devices Interim Regulation (MDIR) in 2011. The MDIR outlines specifications for the labelling, licencing, and registration of ECG equipment.

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

ECG Equipment Market Segmentation

By Product Type (Revenue, USD Billion):

- Holter Monitors

- Resting ECG Machines

- Stress ECG Machines

- Event Monitoring Systems

- ECG Management Systems

- Cardiopulmonary Stress Testing Systems

By End User (Revenue, USD Billion):

- Hospitals and Clinics

- Diagnostic Centres

- Ambulatory Services

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

Morocco ECG Equipments Market Analysis

Medical Devices

Malaysia Contraceptive Devices Market Analysis

Medical Devices

Mexico Breastfeeding Accessories Market Analysis

Related reports (by geography)

Medical Devices

Saudi Arabia Breast Pump Market Report

Medical Devices

Saudi Arabia Neurology Devices Market Analysis

Pharmaceuticals

Saudi Arabia Rheumatology Drugs Market Analysis

Pharmaceuticals