Medical Devices

Saudi Arabia Diabetes Devices Market Analysis

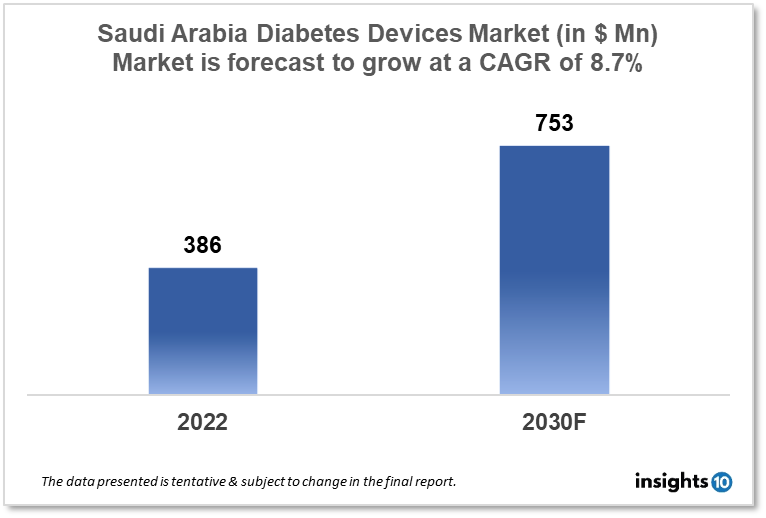

Saudi Arabia's Diabetes Devices Market is expected to witness growth from $386 Mn in 2022 to $753 Mn in 2030 with a CAGR of 8.70% for the forecasted year 2022-30. One of the greatest rates of diabetes is found in Saudi Arabia. As more individuals need access to blood glucose monitors, insulin pumps, and other diabetes management tools, this expands the market for diabetes devices. The market is segmented by type and by the end user. Some key players in this market include Aljeel Medical, Alhammad Medical, Medyssey, Johnson & Johnson, Philipps Healthcare, Medtronic, Roche, and Dexcom.

Buy Now

Saudi Arabia Diabetes Devices Healthcare Market Executive Analysis

Saudi Arabia's Diabetes Devices Market is expected to witness growth from $386 Mn in 2022 to $753 Mn in 2030 with a CAGR of 8.70% for the forecasted year 2022-30. The general funding for healthcare in Saudi Arabia for 2023 is 4.5% less than it was for 2022. In 2023, healthcare costs will amount to 5.5% of GDP. In Saudi Arabia, men are projected to live to an average age of 75.33 while women can expect to live to an average age of 78.56. Out-of-pocket costs as a percentage of total healthcare spending in Saudi Arabia in 2020 were 16.5%.

One of the greatest rates of diabetes is found in Saudi Arabia. As of 2021, there were 4.2 million adults in Saudi Arabia (20-79 years) who had diabetes, or 17.3% of the adult population. The prevalence of the disease may be even higher because it is believed that there are about 561,000 unrecognized cases of diabetes in Saudi Arabia. Diabetes devices like blood glucose meters and continuous glucose monitoring systems enable diabetics to routinely check their blood glucose levels. They can better control their diabetes, prevent complications, and modify their therapy as necessary thanks to this. Insulin pumps and insulin pens are diabetes tools that make it easier and more precise for individuals with diabetes to administer insulin. By doing so, complications can be avoided and blood glucose regulation can be improved.

Market Dynamics

Market Growth Drivers

One of the greatest rates of diabetes is found in Saudi Arabia. As more individuals need access to blood glucose monitors, insulin pumps, and other diabetes management tools, this expands the market for diabetes devices. With novel capabilities like continuous glucose monitoring, insulin pumps with closed-loop systems, and smartphone connectivity, diabetes devices are becoming more and more sophisticated. As individuals look for more sophisticated tools for managing their diabetes, technological advancements are predicted to increase the demand for diabetes devices in Saudi Arabia. In Saudi Arabia, where diabetes is an elevated risk factor, an elevated rate of obesity is expanding. Demand for diabetes devices is expected to increase as more individuals require to have access to insulin pumps, blood glucose monitors, and other devices for managing diabetes.

Market Restraints

Some Saudi Arabian diabetic patients may find it difficult to afford the high expense of diabetes devices. The cost of these devices may be prohibitive for many diabetics, which may restrain market expansion. With new players joining the Saudi Arabian diabetes device market and established firms extending their product lines, the market is becoming more and more competitive. Manufacturers may find it challenging to differentiate themselves and capture market share as a result.

Competitive Landscape

Key Players

- Salehiya Medical W/H (SA)

- Aljeel Medical (SA)

- Alhammad Medical (SA)

- Johnson & Johnson

- Medtronic

- Philipps Healthcare

- Dexcom

- Ascensia Diabetes Care

Healthcare Policies and Regulatory Landscape

The regulatory structure and healthcare policies in Saudi Arabia have an immense effect on the market for diabetes devices. The Saudi Arabian government has put in place an abundance of rules and regulations aimed at ensuring both the safety and efficacy of devices, which include those used in the treatment of diabetes. The Saudi Food and Drug Authority (SFDA) is one of the main bodies in Saudi Arabia in terms of regulation. The SFDA is entrusted with handling the regulation of diabetes devices and making sure they abide by global safety and effectiveness standards. The licensing, import, and dissemination of diabetes devices in Saudi Arabia are controlled by rules given forth by the SFDA.

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Diabetes Devices Market Segmentation

By Type (Revenue, USD Billion):

The market is divided into blood glucose monitoring systems, insulin delivery systems, and mobile applications for managing diabetes within the type segment. Due to its convenience, ease of use, and usefulness in providing patients and healthcare professionals with real-time insights regarding diabetic conditions for integrated diabetes management, the segment for diabetes management mobile applications is anticipated to grow at the highest rate during the forecast period. Bare-metal Stents

- Blood glucose monitoring systems

- Self-monitoring blood glucose monitoring systems

- Continuous glucose monitoring systems

- Test strips/Test papers

- Lancets/Lancing Devices

- Insulin delivery Devices

- Insulin pumps

- Insulin pens

- Insulin syringes and needles

- Diabetes management mobile applications

By End User (Revenue, USD Billion):

The diabetes market is divided into hospitals & specialty clinics and self & home care, based on the end user.

- Hospitals & Specialty Clinics

- Self & Home Care

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

Hong Kong Neurology Devices Market Analysis

Medical Devices

India Contact Lenses Market Analysis

Medical Devices

Kenya Physiotherapy Equipment Market Analysis

Related reports (by geography)

Pharmaceuticals

Saudi Arabia Cold Pain Therapy Market Analysis

Pharmaceuticals

Saudi Arabia Interactive Wound Dressing Market Analysis

Pharmaceuticals

Saudi Arabia Inhaled Nitric Oxide Market Analysis

Pharmaceuticals