Medical Devices

Saudi Arabia Breastfeeding Accessories Market Analysis

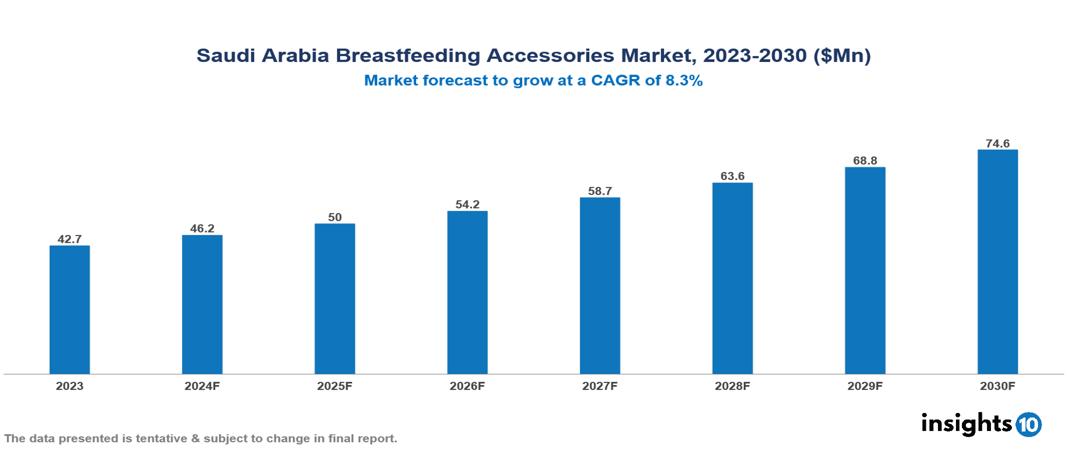

Saudi Arabia Breastfeeding Accessories Market was valued at $42.67 Mn in 2023 and is predicted to grow at a CAGR of 8.30% from 2023 to 2030, to $74.56 Mn by 2030. The key drivers of this industry include high breastfeeding initiation rates, increasing urbanization and maternal employment, and health recommendations. The industry is primarily dominated by Medala, Elvie, Willow Innovations, and Koninklijke Philips among others.

Buy Now

Saudi Arabia Breastfeeding Accessories Market Executive Summary

Saudi Arabia Breastfeeding Accessories Market was valued at $42.67 Mn in 2023 and is predicted to grow at a CAGR of 8.30% from 2023 to 2030, to $74.56 Mn by 2030.

Breastfeeding accessories are essential tools that aim to improve the overall breastfeeding experience for both mothers and babies, addressing varioSaudi Arabia needs from comfort to convenience. Key categories include manual, electric, and hospital-grade breast pumps, which cater to different pumping needs and frequencies, while nursing pads and nipple shields provide comfort by managing milk leaks and protecting sore nipples. Breast shells help collect excess milk and shield sensitive areas, and milk storage containers ensure the safe storage of expressed milk. Nursing bras and covers offer support and discreet breastfeeding options, and breastfeeding pillows provide ergonomic support to both mother and baby during feeds. Additionally, nipple creams soothe and protect against irritation. These accessories not only enhance comfort and ease for mothers but also support health by preventing infections and maintaining milk quality, ultimately contributing to a more positive, manageable, and flexible breastfeeding experience.

Breastfeeding initiation rates in Saudi Arabia are high, generally exceeding 90% in 2023, but timely initiation within the first hour is notably low, with some studies indicating rates as low as 13.9%. The prevalence of exclusive breastfeeding among Saudi mothers is also low, ranging from 0.8% to 43.9% due to inconsistent definitions and methodologies, with a specific study reporting a rate of 16.3%. Mixed feeding practices are common, with 76.1% of mothers introducing bottle-feeding by three months. The duration of breastfeeding has declined over the years, from a mean of 13.4 months in 1987 to 8.5 months in 2010.

The market is therefore driven by significant factors like high breastfeeding initiation rates, increasing urbanization and maternal employment, and health recommendations. However, the high cost of accessories, cultural barriers, and work-life balance challenges restrict the growth and potential of the market.

A prominent player in this field is Medala, in 2024, Medela AG launched a new line of breast pumps with smart technology for real-time tracking and personalized support, enhancing milk production and breastfeeding practices. Similarly, Elvie introduced an updated wearable breast pump featuring improved suction technology and longer battery life, offering greater comfort and efficiency based on user feedback. Other contributors include Willow Innovations, and Koninklijke Philips among others.

Market Dynamics

Market Growth Drivers

High Breastfeeding Initiation Rates: In Saudi Arabia, a significant proportion of mothers initiate breastfeeding, with rates estimated to be around 94%. This high initiation rate fuels the demand for breastfeeding accessories to support and facilitate breastfeeding practices.

Increasing Urbanization and Maternal Employment: With more women joining the workforce and living in urban areas, there is a growing need for convenient breastfeeding solutions. Accessories like breast pumps allow working mothers to continue breastfeeding while managing their professional responsibilities.

Health Recommendations by Government: Saudi health authorities recommend exclusive breastfeeding for the first six months, aligning with global health guidelines. This recommendation drives the demand for products that support sustained and effective breastfeeding according to Saudi Ministry of Health, 2023.

Market Restraints

High Cost of Accessories: The high prices of quality breastfeeding accessories can be a significant barrier for many families in Saudi Arabia. This financial burden may limit the accessibility and widespread adoption of these products.

Cultural Barriers: Cultural norms and misconceptions about breastfeeding and the use of accessories can hinder their acceptance. Traditional views on breastfeeding might reduce the perceived need for modern breastfeeding tools.

Work-Life Balance Challenges: Balancing work and breastfeeding remains a challenge for many mothers in Saudi Arabia. The lack of supportive workplace policies and facilities can limit the effective use of breastfeeding accessories

Regulatory Landscape and Reimbursement Scenario

In Saudi Arabia, the Ministry of Health is the primary regulatory body overseeing medical devices, including breastfeeding accessories. The country likely aligns with international standards and regulations, such as those set by the FDA or the European Union, to ensure the safety and efficacy of these products. The regulatory framework is focused on maintaining high standards for breastfeeding accessories to protect consumers and promote effective breastfeeding practices.

Regarding reimbursement, public health insurance in Saudi Arabia may cover certain breastfeeding accessories, particularly for low-income families or those with specific medical needs, reflecting the government's commitment to healthcare accessibility. Private health insurance plans offer varying levels of coverage based on the specific policy, while consumers might still incur some out-of-pocket expenses for these products.

Competitive Landscape

Key Players

Here are some of the major key players in the Saudi Arabia Breastfeeding Accessories

- Medela AG

- Ameda, Inc.

- Willow Innovations, Inc.

- Koninklijke Philips N.V.

- Elvie (Chiaro Technology)

- Freemie

- NUK USA LLC

- Linco Baby

- Mayborn Group Limited

- Pigeon Corporation

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Saudi Arabia Breastfeeding Accessories Market Segmentation

By Product Type

- Nipple Care Products

- Breast Pumps

- Breast Shells

- Breastmilk Storage & Feeding Products

- Others

By Distribution Channel

- Online retail

- Offline retail

- Hospital pharmacies

By End User

- Hospitals

- Clinics

- Homecare Settings

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

Egypt Biomaterials in Healthcare Market Analysis

Medical Devices

Mexico Contact Lenses Market Analysis

Medical Devices

Russia Cardiac Monitoring Devices Market Analysis

Related reports (by geography)

Pharmaceuticals

Saudi Arabia Biological Safety Testing Market Analysis

Digital Health

Saudi Arabia Mental Health Apps Market Analysis

Pharmaceuticals

Saudi Arabia Proliferative Diabetic Retinopathy Market Analysis

Clinical Trials