Pharmaceuticals

Saudi Arabia Adult Malignant Glioma Therapeutics Market Analysis

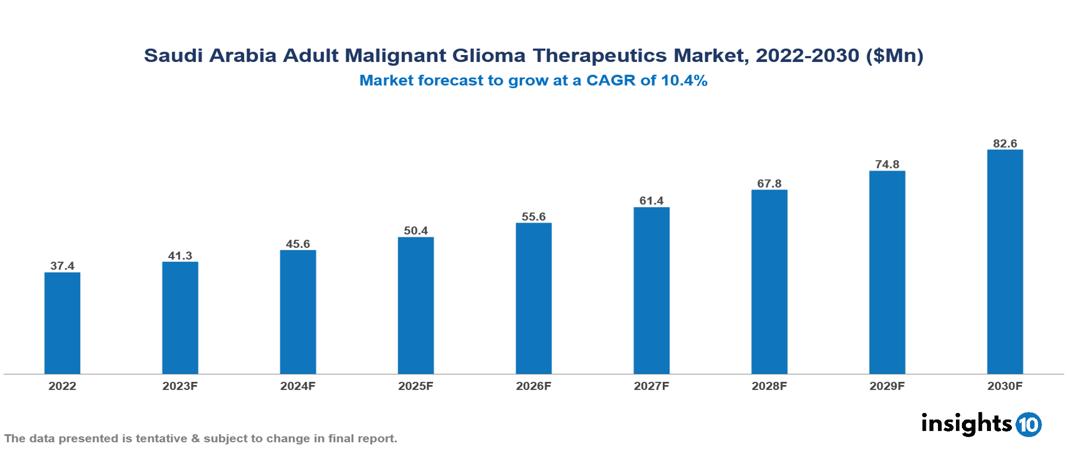

The Saudi Arabia Adult Glioma Therapeutics Market is valued at around $37 Mn in 2022 and is projected to reach $83 Mn by 2030, exhibiting a CAGR of 10.4% during the forecast period. An upsurge in the market is being driven by factors such as increased general awareness, tailored medication preferences, increased government backing, and demographic and urbanisation shifts. Key players in the Saudi Arabia Adult Malignant Glioma Therapeutics Market include companies like Mylan N.V., Teva Pharmaceuticals, Sanofi, Pfizer, GlaxoSmithKline plc., Novartis, Bayer, Merck & Co, etc.

Buy Now

Saudi Arabia Adult Malignant Glioma Therapeutics Market Executive Summary

The Saudi Arabia Adult Glioma Therapeutics Market is valued at around $37 Mn in 2022 and is projected to reach $83 Mn by 2030, exhibiting a CAGR of 10.4% during the forecast period.

Adult malignant glioma is a kind of cancer that starts in the brain and is distinguished by the presence of malignant (cancerous) glial cells. In the central nervous system, glial cells surround and support neurons. Gliomas are tumours that develop from glial cells. Malignant gliomas are especially aggressive and can spread to neighbouring brain structures. Gliomas are brain tumours that develop from glial cells, which are supporting cells in the central nervous system. Gliomas are characterized according to the individual glial cell from which they arise and the degree of malignancy. Astrocytomas, Oligodendrogliomas, and Ependymomas are among the several types. Glioblastoma Multiforme (GBM), a kind of astrocytoma, is a fairly common condition among all gliomas. Treatment is specific to each patient, and a multidisciplinary approach is taken.

In Saudi Arabia, malignant primary brain tumours are infrequent, accounting for 2–3% of all adult malignancies. Among all Adult Malignant Glioma types, glioblastoma (54.52%) was the most frequent kind of adult glioma (46.49%) among the population.

An upsurge in Saudi Arabia Adult Glioma Therapeutics Market is being driven by factors such as increased general awareness, tailored medication preferences, increased government backing, and demographic and urbanisation shifts.

Key players in the Saudi Arabia Adult Malignant Glioma Therapeutics Market include companies like Mylan N.V., Teva Pharmaceuticals, Sanofi, Pfizer, GlaxoSmithKline plc., Novartis, Bayer, Merck & Co, etc.

Market Dynamics

Market Growth Drivers

As the potential benefits of sophisticated and targeted therapies beyond basic chemotherapy and radiation become more widely known, demand for them grows. Personalized medicine techniques that analyse individual tumour traits are gaining acceptance, which might lead to more successful treatment options. Clinical trials and early access programs for new glioma therapies held in Saudi Arabia provide patients with cutting-edge treatment choices.

The Saudi government's enormous investment in healthcare infrastructure and research offers a favourable environment for market expansion. Policies aimed at improving healthcare access and cost may increase the number of patients seeking treatment for gliomas. Rising disposable incomes and greater insurance coverage in Saudi Arabia enable more patients to receive costly glioma therapy. The Saudi government has set aside $5 billion in 2023 exclusively for cancer treatment programs, including extending access to glioma treatments.

The World Health Organization anticipates a 20% increase in Saudi Arabia's population over 50 years old by 2030, potentially leading to a 35% increase in glioma incidence. The aging population raises the likelihood of acquiring glioma, which naturally leads to a larger patient pool for therapies. Urbanization trends may also aid to market expansion as access to specialist glioma care becomes more concentrated in metropolitan areas.

Market Restraints

There are certain barriers that limit the market growth of Saudi Arabia to a certain extent. Some factors, like the cultural stigma associated with cancer, particularly brain tumours, might deter patients from obtaining prompt diagnosis and treatment. Patients who lack awareness about modern glioma therapy choices, particularly in rural locations, may get ineffective or outmoded treatments. Lack of awareness about less invasive or novel treatment methods lowers the market’s growth opportunity.

Malignant primary brain tumours, including glioblastoma, are relatively uncommon, accounting for just 2–3% of all adult malignancies in Saudi Arabia. The low market size may limit the possibility for considerable expansion in the therapeutics sector. The presence of existing global players in the market will increase the completion rate, and due to the smaller market size, barriers to entry are comparatively higher.

While Saudi Arabia has comprehensive cancer centres, some localities may have limited access to specialist facilities and trained healthcare personnel. This might affect the delivery of modern glioma therapy, limiting market development. Appropriate infrastructure and investments are necessary before all the facilities can be made available in these regions.

Notable Recent Updates

January 2023, The King Faisal Specialist Hospital and Research Centre launched a comprehensive glioma genomic profiling program, with other centres following suit.

July 2023, A total of $5 Bn cancer treatment budget allocation was announced and is being distributed across various initiatives.

Healthcare Policies and Regulatory Landscape

Saudi Arabia's healthcare system is experiencing major transformations. While obstacles exist, the government's commitment to universal coverage and ongoing progress bode well for the future of healthcare in the country. All Saudi nationals and residents who have valid residency permits are eligible for free healthcare, which includes preventative, primary, secondary, and tertiary treatment. This is primarily funded by the government, with around 15–17% of the total budget set aside for healthcare and social development. Saudi Arabia's major therapeutic and governing organization is the Saudi Food and Drugs Administration (SFDA). The SFDA maintains tight drug approval requirements to ensure high levels of safety and efficacy. Trials are conducted following a rigorous R&D procedure, and an application is submitted to the SFDA together with the relevant safety and effectiveness information. The specialists meticulously review the provided data to verify that the treatment fulfils safety, effectiveness, and quality requirements before issuing a market authorization, which allows the therapy to be promoted and sold in Saudi Arabia.

Competitive Landscape

Key Players

- Mylan N.V.

- Teva Pharmaceuticals

- Sanofi

- Pfizer

- GlaxoSmithKline plc.

- Novartis

- Bayer

- Merck & Co.

- Allergan

- AstraZeneca

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Saudi Arabia Adult Malignant Glioma Therapeutics Market Segmentation

By Disease Type

- Glioblastoma Multiforme

- Anaplastic Astrocytoma

- Anaplastic Oligodendroglioma

- Anaplastic Oligoastrocytoma

- Other Types

By Treatment Type

- Chemotherapy

- Targeted Drug Therapy

- Radiation Therapy

- Surgery

- Gene Therapy

- Immunotherapy

- Vaccines

By Distribution Channel

- Hospital Pharmacies

- Drug Stores & Retail Pharmacies

- Online Pharmacies

By Disease Stage

- Early-Stage Tumour

- Late-Stage Tumour

- Palliative Care

By Route of Administration

- Oral

- Parenteral

- Others

By End User

- Hospitals

- Speciality Clinics

- Chemotherapy Centres

- Radiotherapy Centres

- Homecare

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Saudi Arabia Head and Neck Cancer Therapeutics Market Analysis

Pharmaceuticals

Romania HIV Therapeutics Market Analysis

Pharmaceuticals

China Mammography Device Market Analysis

Related reports (by geography)

Pharmaceuticals

Saudi Arabia Kidney Cancer Therapeutics Market Analysis

Pharmaceuticals

Saudi Arabia Infectious Wound Care Management Market Analysis

Pharmaceuticals

Saudi Arabia Ophthalmic Drugs Market Analysis

Pharmaceuticals