Digital Health

Russia Artificial Intelligence (AI) in Diagnostics Market Analysis

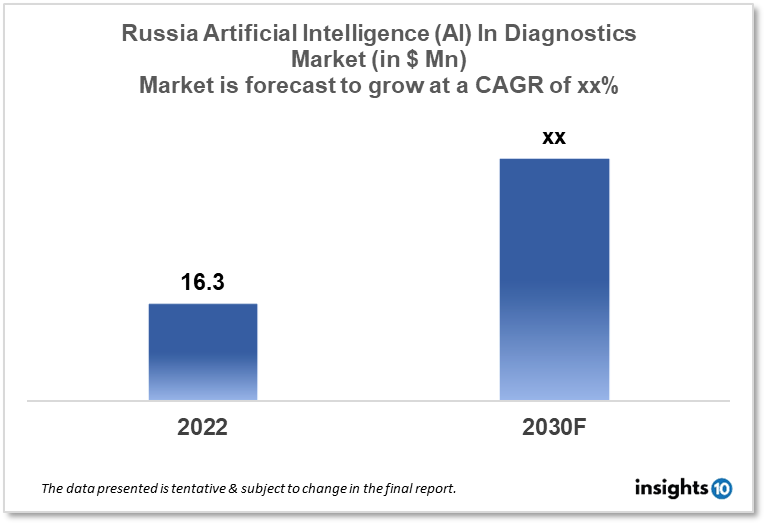

Russia's Artificial Intelligence (AI) in the diagnostics market is projected to grow from $16.3 Mn in 2022 to $xx Mn by 2030, registering a CAGR of xx% during the forecast period of 2022-30. The market will be driven by encouraging government efforts & a strong focus on technical innovation. The market is segmented by component & by diagnosis. Some of the major players include IBM Watson Health, Siemens Healthineers & TeleMD.

Buy Now

Russia Artificial Intelligence (AI) in Diagnostics Market Executive Summary

The Russia Artificial Intelligence (AI) in the diagnostics market is projected to grow from $16.3 Mn in 2022 to $xx Mn by 2030, registering a CAGR of xx% during the forecast period of 2022 - 2030. Cardiovascular disorders, cancer, and HIV are the most common illnesses in Russia, fuelling the need for diagnostic interventions. High rates of smoking and alcohol intake also have a significant role in sickness. According to a WHO survey, 39.1% of Russians smoke, compared to 22.7% globally and 27.3% in Europe.

Medical imaging and patient data may be scanned by AI-powered diagnostic tools to discover early warning signs of ailments such as cancer and heart disease. AI may be used to improve diagnostic accuracy by analyzing medical imaging such as CT scans, MRI scans, and X-rays. AI-powered imaging technologies can also help radiologists examine images more quickly and precisely. AI may be used to monitor patients with chronic illnesses such as diabetes and heart disease. While artificial intelligence in diagnostics is still in its early stages in Russia, there is significant potential for its use in improving healthcare outcomes and cutting costs.

A pilot project to deploy a clinical decision support system in Kirov Region was finished in July 2020. The research was carried out in collaboration with the Medical Information and Analysis Center and a number of regional medical institutions, including the Kirov Clinical Diagnostic Center, the Center for Oncology and Medical Radiology, and the Center for Cardiology and Neurology. With cooperation from Russia's Ministry of Health, the Republic of Sakha developed a pilot initiative called 'ONKOPOISKSAKHA.RF' (onco-search Sakha). AI solutions for oncopathologies are being considered by the developers for application in preventative medicine.

Market Dynamics

Market Growth Drivers

Russia is a home for various AI-based startups such as Neiry, Botkin.AI, Webiomed, Semantic Hub & TeleMD which are set to further expand the market in Russia. The Russian Federation's Ministry of Health sponsored the establishment of guidelines for the use of artificial intelligence in health care in July 2020. The organization stated that developing a regulatory framework will aid in the development of standard ways to assess the safety and dependability of AI-based systems. The effort aims to increase trust in the use of medical technology. According to the agency, the Digital Diagnosis initiative was established with the cooperation of Russia's Ministry of Health.

The Ministry of Health had begun a project with Rostec Corporation to establish a platform that will provide information assistance to AI solution developers in the field of medicine. The result was the creation of the first edition of the government AI platform in July 2021.

Market Restraints

The use of artificial intelligence (AI) in diagnostics has the potential to revolutionize Russian healthcare. Yet, a number of impediments are impeding its widespread adoption. These challenges include legal uncertainty, as the regulatory landscape for AI in healthcare is complex. In Russia, the scenario is still evolving, creating uncertainty for developers and investors, concerns over data reliability and confidentiality, functionality to integrate with existing healthcare systems with electronic medical records, resistance to change by certain professionals, and limited access to technology because of high costs or a lack of skills.

Competitive Landscape

Key Players

- IBM Watson Health

- Siemens Healthineers

- Philips Healthcare

- GE Healthcare

- Google Health

- AliveCor, Inc.

- Riverain Technologies

- Neiry (RUS)

- Webiomed (RUS)

- TeleMD (RUS)

- iBinom (RUS)

Notable Deals

- February 2023, GE HealthCare to Acquire Caption Health The acquisition adds AI-enabled image guiding to the ultrasound device portfolios of GE HealthCare's $3 billion Ultrasound division

- In May 2022, GE Healthcare inked an arrangement with Alliance Medical, a radiology services firm. The firms agreed to work together to create a digital health solution using powerful AI and data analytics

Healthcare Policies and Regulatory Landscape and Reimbursement Scenario

Russia, as a member of the Eurasian Economic Union (the "EAEU"), abides by the EAEU laws governing the establishment of a Common Market for pharmaceuticals and medical equipment. The legal framework for medical device authorisation, pricing, and reimbursement comprises the Law on Basic Healthcare Principles, the contents of which are reinforced by regulations approved by the Russian Federation's Government and Minzdrav.

1. Executive Summary

1.1 Digital Health Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Digital Health Policy in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Artificial Intelligence (AI) in Diagnostics Market Segmentation

- By Component Outlook Type (Revenue, USD Billion):

- Software

- Hardware

- Services

- By Diagnosis Outlook Type (Revenue, USD Billion):

- Cardiology

- Oncology

- Pathology

- Radiology

- Chest and Lung

- Neurology

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Digital Health

Australia 3D Imaging Market Analysis

Digital Health

Singapore 3D Imaging Market Analysis

Related reports (by geography)

OTC & Nutraceuticals

Russia Nutritional Supplements Market Analysis

Pharmaceuticals

Russia Sleep Disorders Market Analysis

Pharmaceuticals