Pharmaceuticals

Philippines Congestive Heart Failure Therapeutics Market Analysis

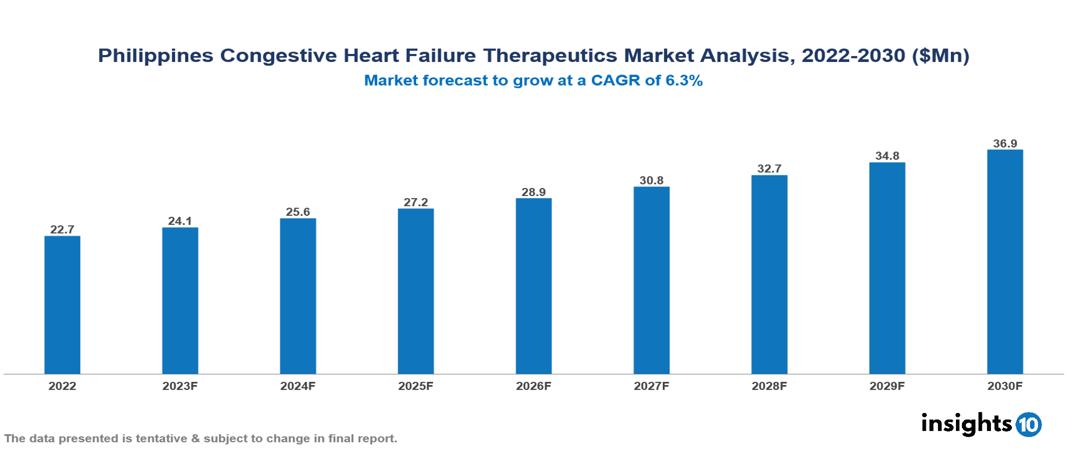

The Philippines Congestive Heart Failure Therapeutics Market is anticipated to experience a growth from $23 Mn in 2022 to $37 Mn by 2030, with a CAGR of 6.3% during the forecast period of 2022-2030. The key drivers of the market include the rising prevalence of CHF due to an aging population and increased risk factors, growing awareness and timely diagnosis leading to early intervention, and ongoing advancements in medications. The Philippines Congestive Heart Failure Therapeutics Market encompasses various key players across different therapeutic segments, including Novartis, AstraZeneca, Bayer, Abbott, Roche, Merck, Unilab, Metro Drug, Pharmaserv, Medichem, etc, among various others.

Buy Now

Philippines Congestive Heart Failure Therapeutics Market Analysis Executive Summary

The Philippines Congestive Heart Failure Therapeutics Market is anticipated to experience a growth from $23 Mn in 2022 to $37 Mn by 2030, with a CAGR of 6.3% during the forecast period of 2022-2030.

Congestive Heart Failure (CHF) is a chronic medical disorder, which is defined as the heart's inability to efficiently pump blood. This causes fluid buildup in the lungs and other tissues. This progressive illness can be caused by a variety of underlying conditions, such as coronary artery disease, hypertension, or cardiomyopathy. CHF is often either systolic heart failure, which is defined by reduced pumping function, or diastolic heart failure, which is defined by difficulties in relaxing. Treatment for CHF often includes a combination of lifestyle changes, medicines, and, in extreme situations, surgical treatments. Diuretics may be prescribed to reduce fluid retention, ACE inhibitors to lower blood pressure, and beta-blockers to improve heart function. Dietary adjustments, exercise, and weight control are common lifestyle alterations. Technological improvements have had a tremendous impact on the CHF management environment. Remote monitoring gadgets and wearable technology allow healthcare providers to remotely check vital signs and change treatment regimens. Implantable devices like pacemakers and defibrillators help regulate heart rhythm, which improves overall cardiac function.

The prevalence of CHF in the Philippines was reported to be 1.6% or 1648 instances per 100,000 individuals. Hypertension was the most prevalent cause, and there were more occurrences of systolic heart failure. The rates rise with age, making it more frequent among the elderly.

The key drivers of the market include the rising prevalence of CHF due to an aging population and increased risk factors, growing awareness and timely diagnosis leading to early intervention, and ongoing advancements in medications.

Global pharmaceuticals like Pfizer, Novartis, Merck, etc have the biggest market share, extensive drug portfolios, and strong brand recognition due to their worldwide presence. They are closely followed by AstraZeneca and Abbott, both well-established companies with slightly different segments. Unilab is the largest domestic pharmaceutical company, providing many medications for cardiovascular problems. It has a significant brand awareness because of its broad distribution network.

Market Dynamics

Market Growth Drivers

Increasing Prevalence: The rising prevalence of CHF stands as a significant driver for market growth, fueled by an aging population and an increasing burden of risk factors such as obesity, diabetes, and hypertension. As these conditions become more prevalent, the overall incidence of CHF is expected to rise, creating a heightened demand for effective treatments.

Increasing Awareness and Diagnosis: With a growing understanding of CHF symptoms and associated risk factors, more individuals are undergoing timely diagnosis. This heightened awareness not only leads to early intervention but also significantly contributes to an increased demand for treatment options.

Development of New and Improved Treatments: Ongoing research efforts are resulting in the introduction of advanced medications and devices for CHF treatment. These innovations not only enhance the efficacy of treatment but also contribute to improving the overall quality of life for CHF patients.

Market Restraints

High Cost Associated: The financial burden of CHF treatments can be a significant barrier to access, particularly in developing countries like the Philippines. Economic challenges and income disparities further exacerbate this issue, limiting the reach of these treatments to a broader population.

Lack of Reimbursement: Not all treatments are covered by insurance, and this can restrict access for patients seeking specific, often newer, treatments. This financial barrier may impede the adoption of advanced therapies, impacting both patients and the market.

Limited Access to Healthcare Services: Inadequate healthcare infrastructure makes it difficult for individuals to receive timely and appropriate treatment. This limitation in healthcare accessibility poses a considerable challenge for addressing the growing prevalence of CHF and providing effective care to those in need.

Healthcare Policies and Regulatory Landscape

Healthcare policies in the Philippines play a vital role in the nation's commitment to providing accessible, affordable, and high-quality healthcare services for its citizens. The Department of Health (DOH) serves as the key governmental body tasked with formulating and implementing these policies. The policies cover a broad spectrum, including disease prevention, the development of healthcare infrastructure, and the regulation of pharmaceuticals. Ensuring the safety and efficacy of pharmaceuticals is a critical aspect of healthcare regulation, overseen by the Food and Drug Administration (FDA) of the Philippines. Operating under the DOH, the FDA serves as the primary regulatory authority responsible for approving, monitoring, and conducting post-market surveillance of drugs. This involves stringent assessments to guarantee that pharmaceutical products meet rigorous standards before they are introduced to the Philippine market. The FDA's responsibilities extend to comprehensive evaluations, licensing processes, and inspections of manufacturing facilities, all aimed at ensuring that pharmaceutical products adhere to strict quality standards. By implementing a robust regulatory framework, the FDA significantly contributes to upholding a high standard of healthcare in the Philippines.

Competitive Landscape

Key Players:

- Novartis

- AstraZeneca

- Bayer

- Abbott

- Roche

- Merck

- Unilab

- Metro Drug

- Pharmaserv

- Medichem

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Philippines Congestive Heart Failure Therapeutics Market Segmentation

By Stage of Heart Failure

- Acute Heart Failure

- Chronic Heart Failure

By Drug Class

- ACE Inhibitors

- Beta Blockers

- Angiotensin 2 Receptor Blockers

- Diuretics

- Aldosterone Antagonists

- Others

By Route of Administration

- Oral

- Parenteral

By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

By End User

- Hospitals

- Speciality Clinics

- Homecare

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Philippines Exosome Research Market Analysis

Pharmaceuticals

Germany Ophthalmic Drugs Market Analysis

Pharmaceuticals

Indonesia Dental Fluoride Treatment Market Analysis

Related reports (by geography)

Pharmaceuticals

Philippines Paracetamol Market Analysis

Pharmaceuticals

Philippines Compounding Pharmacies Market Analysis

OTC & Nutraceuticals