Healthcare Services

North America Patient Engagement Solutions Market Analysis

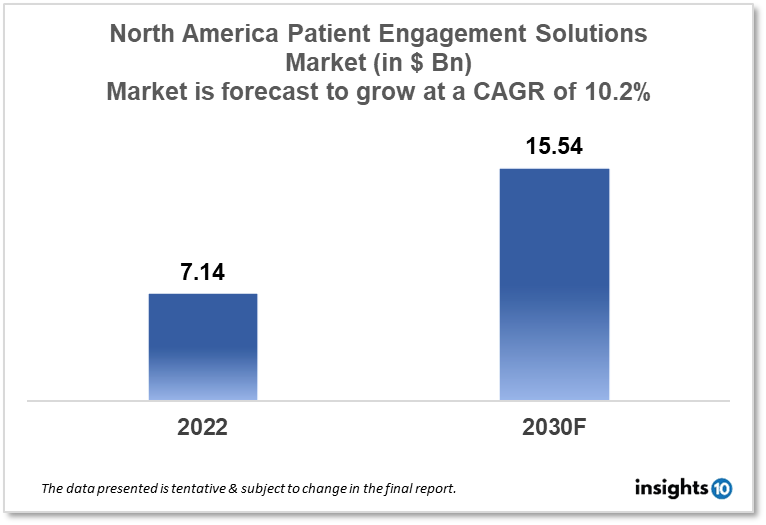

North American patient engagement solutions market is projected to grow from $7.14 Bn in 2022 to $15.54 Bn by 2030, registering a CAGR of 10.2% during the forecast period of 2022-30. The main factors driving the growth would be the rising prevalence of chronic diseases, the requirement to lower costs of healthcare for greater accessibility, government laws supporting the healthcare system, and the concentration of key market players operating in the area. The market is segmented by component, delivery mode, application, therapeutic area, functionality, and end-user. Some of the major players include Allscripts, Cerner Corporation, McKesson, Athena Health, Telus Health, and WELL Health Technologies.

Buy Now

North America Patient Engagement Solutions Market Executive Summary

North American patient engagement solutions market is projected to grow from $7.14 Bn in 2022 to $15.54 Bn by 2030, registering a CAGR of 10.2% during the forecast period of 2022-30. North America, which consists of the US and Canada, has one of the highest GDPs in the entire globe. In 2020, North America's GDP is expected to exceed $20.5 trillion, according to the World Bank. In North America, healthcare expenses vary from one country to the next, but they are typically enormous. The US spends 17.2% more on healthcare as a proportion of GDP than any other country in North America, according to the WHO. In Canada, healthcare expenditures as a share of GDP were 10.3%.

With the presence of important players, increased mHealth and EHR adoption, and growing investment in patient engagement software by the leading companies, North America held the greatest revenue share of approximately 35.0% in 2021.

The U.S. dominates the market in North America, and it is anticipated that it will show a CAGR of over 10.2 % until the end of the decade. The government's growing investment in the healthcare sector and the public's growing understanding of the importance of following medication schedules are credited with the country's improvement.

Market Dynamics

Market Growth Drivers

The rising prevalence of chronic diseases, the requirement to lower costs of healthcare for greater accessibility, government laws supporting the healthcare system, and the concentration of key market players operating in the area are the main factors propelling the market's expansion in North America.

Market Restraints

A lot of healthcare providers could be discouraged from making the required investment due to the cost of designing and implementing patient engagement solutions. The market's expansion in the region is being constrained by the high cost of patient engagement solutions.

Competitive Landscape

Key Players

- Allscripts

- Cerner Corporation

- Mckesson

- Athena Health

- Telus Health

- WELL Health Technologies

Notable Deals

August 2021: Mckesson and Merck declared a strategic partnership that would enable the two healthcare titans to harness the power of real-world evidence (RWE) for the benefit of improving patient outcomes and the standard of cancer therapy.

September 2021: Telus has completed its $1.71 Bn acquisition of LifeWorks, marking the beginning of an era of employer-focused healthcare. As a result of this transaction, Telus Health now provides corporate clients with coverage in more than 160 nations and for 50 Mn people worldwide, expanding its global reach.

Healthcare Policies and Regulatory Landscape

A complex regulatory environment for healthcare governs the market for patient engagement solutions in North America. The usage and execution of patient engagement solutions are governed by a number of laws and regulations pertaining to healthcare, including the Health Insurance Portability and Accountability Act (HIPAA) and the Affordable Care Act (ACA). HIPAA establishes national guidelines for safeguarding the security and privacy of personal health data, and it mandates that covered organisations put in place administrative, physical, and technical measures to guarantee the privacy, integrity, and accessibility of Electronic Protected Health Information (ePHI). Contrarily, the ACA advocates for patient-centred care and stresses the significance of patient engagement in enhancing health outcomes.

Reimbursement Scenario

The market for patient engagement solutions in North America is heavily influenced by reimbursement policies. CMS, which oversees government healthcare programs including Medicare and Medicaid, is primarily responsible for regulating healthcare reimbursement practises in the US. For the purpose of encouraging healthcare providers to adopt patient engagement strategies and advance value-based care, CMS has created a number of payment models and reimbursement initiatives.

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Patient Engagement Solutions Market Segmentation

By component (Revenue, USD Billion):

- Hardware

- Software

- Standalone Software

- Integrated Software

- Services

By Delivery Mode (Revenue, USD Billion):

- PREMISE Mode

- CLOUD-BASED Mode

By Application (Revenue, USD Billion):

- Health Management

- Home Health Management

- Social

- Financial Health Management

By Therapeutic area (Revenue, USD Billion):

- Chronic Diseases

- Cardiovascular Diseases (CVD)

- Diabetes

- Obesity

- Other chronic Diseases

- Women's Health

- Fitness

- Other Therapeutic Areas

By Functionality (Revenue, USD Billion):

- E-Prescribing

- Virtual Consultation

- Patient/Client Scheduling

- Document Management

By End-user (Revenue, USD Billion):

- Providers

- Payers

- Patients

- Other End users

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

The North American patient engagement solutions market is projected to grow from $7.14 Bn in 2022 to $15.54 Bn by 2030, registering a CAGR of 10.2% during the forecast period of 2022 - 2030.

The North American patient engagement solutions market is segmented by component (hardware, software, standalone software, integrated software and services), by delivery mode (premise mode and cloud-based mode), by application (health management, home health management, social health management and financial health management), by therapeutic area (chronic diseases, cardiovascular diseases, diabetes, obesity, women’s health, fitness and other therapeutic areas), by functionality (e-prescribing, virtual consultation, patient/client scheduling and document management) and by end-user (providers, payers, patients and end-user).

Some of the major players in the North American patient engagement solutions market are Allscripts, Cerner Corporation, McKesson, Athena Health, Telus Health and WELL Health Technologies.

Related reports (by category)

Healthcare Services

Malaysia In Vitro Fertilisation (IVF) Service Market Analysis

Healthcare Services

Brazil DNA Sequencing Market Analysis

Healthcare Services

China Stroke Management and Care Market Analysis

Related reports (by geography)

Medical Devices

North America Pain Management Devices Market Analysis

Pharmaceuticals