Healthcare Services

Middle East Cancer Pain Management Market Analysis

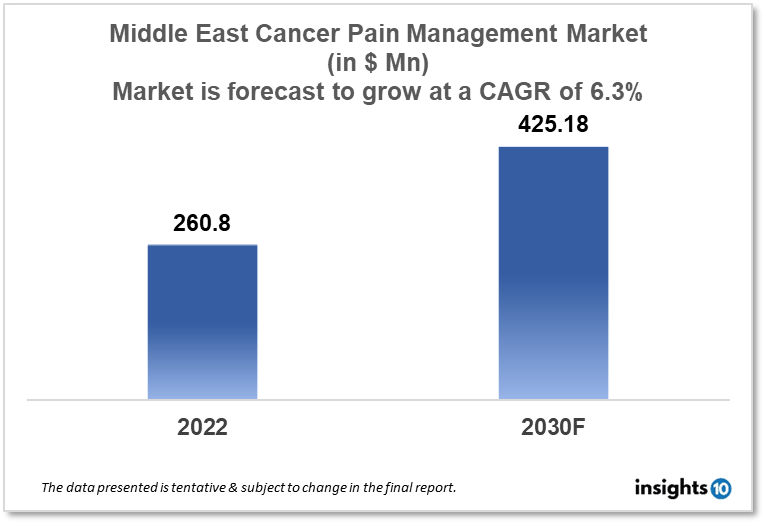

Middle East Cancer Pain Management market is projected to grow from $260.8 Mn in 2022 to $425.18 Mn by 2030, registering a CAGR of 6.3% during the forecast period of 2022-30. The main factors driving the growth would be the rise in cancer incidence, technological advancements in pain relief, and the expansion of the healthcare industry. The market is segmented by drug type and by disease. Some of the major players include NewBridge Pharmaceuticals, Neopharma, Abbott, Pfizer, Johnson & Johnson, and Sanofi.

Buy Now

Middle East Cancer Pain Management Market Executive Summary

Middle East Cancer Pain Management market is projected to grow from $260.8 Mn in 2022 to $425.18 Mn by 2030, registering a CAGR of 6.3% during the forecast period of 2022-30. The GDP and healthcare spending of countries in the Middle East vary substantially. Qatar and the United Arab Emirates are two Middle Eastern countries with high GDPs and significant healthcare expenditures. Others with smaller GDPs and lower healthcare spending include Yemen and Syria.

The majority of chronic pain is brought on by cancer, while the majority of acute pain is brought on by therapy or diagnostic procedures related to cancer. Uncomfortable side effects from chemotherapy and radiotherapy may persist for a long time following the course of treatment. The location and stage of the tumor have the most effects on whether or not there is discomfort. Patients with malignant cancer have pain constantly, and two-thirds of those with advanced illness experience it to the point that it interferes with their sleep, emotions, social interactions, and daily activities.

The Middle East has the greatest and lowest rates of cancer, with Egypt and Lebanon reporting 159.4 and 165.8 cases per 100,000 persons, respectively, and Saudi Arabia and Sudan reporting 96.4 and 95.7 cases, respectively.

Market Dynamics

Market Growth Drivers

The Middle East cancer pain management market is fueled by a number of reasons, including the rise in cancer incidence, technological advancements in pain relief, and the expansion of the healthcare industry. The prevalence of cancer is increasing in the Middle East, and lifestyle-related malignancies like breast, lung, and colorectal cancers are becoming more common. Cancer pain management services and therapies are in high demand as a result of the rise in cancer diagnoses. Furthermore, improvements in pain management technologies and therapies are enhancing the efficacy of pain management for cancer patients and producing more favorable results.

Market Restraints

The Middle East cancer pain management market is constrained by a number of issues, including poor insurance coverage, a lack of healthcare resources, and high pricing for treatments and services. Patients may find it challenging to receive these services due to the Middle East's limited supply of pain management services, particularly in rural and outlying areas. Additionally, there are differences in the Middle East regarding insurance coverage for cancer pain management services, with some nations providing complete coverage while others do not. Patients in nations with limited insurance coverage or payment rules may have fewer access options for pain treatment services as a result.

Competitive Landscape

Key Players

- NewBridge Pharmaceuticals

- Neopharma

- Abbott

- Pfizer

- Johnson & Johnson

- Sanofi

Notable Recent Deals

December 2022: Sanofi and Innate Pharma announced the expansion of their collaboration with the licensing of an NK cell engager program from Innate's ANKETTM (Antibody-based NK Cell Engager Therapeutics) technology that targets B7H3. Sanofi will also have the option of adding up to two more ANKETTM targets. Following candidate selection, Sanofi will be in charge of all development, manufacturing, and marketing.

Healthcare Policies and Regulatory Landscape

Governmental policies and healthcare laws have an impact on the Middle East cancer pain management market's regulatory environment. The introduction of new pain management medications and treatments is delayed by the region's normally strict and stretched drug approval process.

In UAE, the Ministry of Health and Prevention (MOH), the primary healthcare regulatory authority, is in charge of drafting the rules and policies governing the management of cancer pain. According to the MOH, all medical facilities, including those providing cancer pain management therapies, must have the proper licenses and registrations.

In Saudi Arabia, the Saudi Food and Drug Authority (SFDA) and the Ministry of Health (MOH) are primarily in charge of governing healthcare regulations and the management of cancer pain. The MOH sets standards and guidelines for the provision of medical services, including the management of pain in cancer patients. Drugs used to manage pain must be supervised and approved by the SFDA.

Reimbursement Scenario

The Middle East cancer pain management market's reimbursement landscape is complicated and differs from nation to nation. For instance, there is extensive insurance coverage for cancer treatments and pain management services in nations like the UAE and Saudi Arabia, including reimbursement for prescription medications, medical procedures, and other related charges. On the other hand, patients may have to pay a sizeable percentage of the cost of cancer pain management therapies out-of-pocket in nations like Yemen and Iraq where insurance coverage is scarce.

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Cancer Pain Management Market Segmentation

By Drug Type (Revenue, USD Billion):

Non-steroidal anti-inflammatory medicines relieve pain at the site of injury by blocking the cyclooxygenase enzyme, which prevents prostaglandin formation. NSAIDs are a class of medications that includes medications with analgesic, antipyretic, and, at higher doses, anti-inflammatory properties.

- Opioids

- Morphine

- Fentanyl

- Others

- Non-Opioids

- Acetaminophen

- Non-Steroidal Anti-Inflammatory Drugs (NSAIDs)

- Nerve Blockers

By Disease Indication (Revenue, USD Billion):

Based on disease Indication the market is segmented into:

- Lung Cancer

- Colorectal cancer

- Breast cancer

- Prostate cancer

- Blood cancer

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

Canada Preventive Healthcare Technologies and service Market Analysis

Healthcare Services

France Bispecific Antibody Market Analysis

Healthcare Services

US Oxygen Flow Meters Market Analysis

Related reports (by geography)

Pharmaceuticals

Mexico Inflammatory Bowel Disease (IBD) Drugs Market Analysis

Digital Health

Middle East Digital Health Market Analysis

Pharmaceuticals

Mexico SGLT2 Inhibitor Market Analysis

Clinical Trials