Healthcare Services

Mexico Genomic Diagnostics Market Analysis

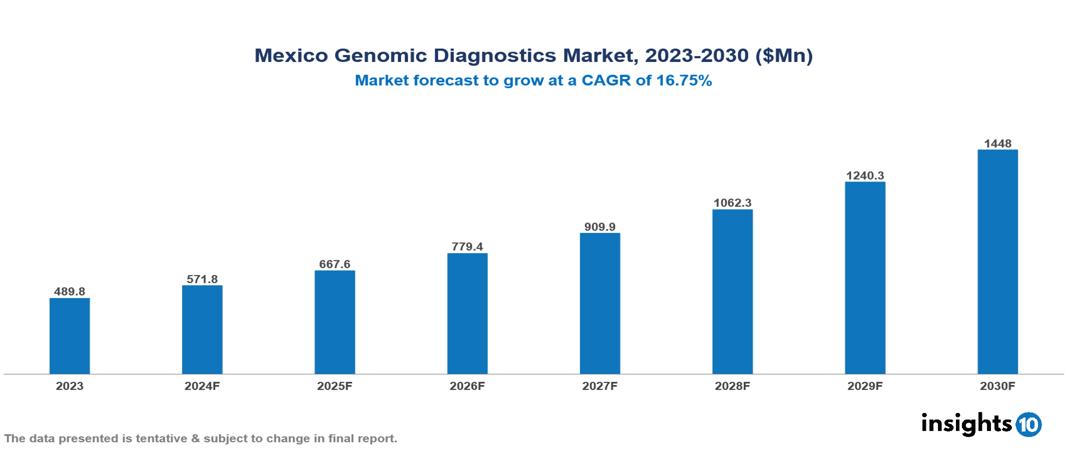

Mexico Genomic Diagnostics Market was valued at $489.75 Mn in 2023 and is predicted to grow at a CAGR of 16.75% from 2023 to 2030, to $1,448.01 Mn by 2030. The key drivers of this industry include increasing demand for personalized medicine, government initiatives, and technological advancements. The industry is primarily dominated by Illumina, 23andMe, Myriad Genetics, and Amgen among others.

Buy Now

Mexico Genomic Diagnostics Market Executive Summary

Mexico Genomic Diagnostics Market was valued at $489.75 Mn in 2023 and is predicted to grow at a CAGR of 16.75% from 2023 to 2030, to $1,448.01 Mn by 2030.

Genomic diagnostics is a rapidly evolving field that uses an individual's genetic information to diagnose diseases, assess predisposition to future health problems, and guide treatment plans by analyzing DNA or RNA for disease-linked variations. This includes karyotyping to examine chromosome abnormalities, targeted mutation analysis for specific disease-related genes, and next-generation sequencing (NGS) for a comprehensive genetic analysis. Applications encompass disease diagnosis, carrier testing for informed family planning, predictive testing for disease risk assessment, and pharmacogenomics for personalized medication treatments. The benefits of genomic diagnostics include early disease detection, personalized medicine, and improved disease management and prognosis.

The prevalence of chronic diseases in Mexico is high and increasing, with diabetes, hypertension, obesity, and chronic kidney disease being among the most common and costly conditions. Diabetes, the leading cause of death in Mexico, saw a significant rise in prevalence of 11% in 2021 among adults aged 20 and older. Chronic kidney disease is the most expensive condition, with annual costs of approximately $9,000 per patient. Four chronic diseases (chronic kidney disease, hypertension, type 2 diabetes, and chronic ischemic heart disease) account for the majority of the financial burden in both the Ministry of Health and the Mexican Social Security Institute (IMSS).

Market is therefore driven by significant factors like increasing demand for personalized medicine, government initiatives, and technological advancements. However, ethical and privacy concerns, high costs, and infrastructure and skilled workforce challenges restrict the growth and potential of the market.

A prominent player in this field is Illumina, which has partnered with AstraZeneca to leverage genomics and AI for faster drug development by identifying new therapeutic targets and biomarkers, 23andMe acquired Lemonaid Health to enhance its personalized healthcare offerings through telehealth and prescription drug delivery services based on genetic information. Other contributors include Myriad Genetics, and Amgen among others.

Market Dynamics

Market Growth Drivers

Increasing Demand for Personalized Medicine: There is a rising demand for personalized medicine, which heavily relies on genomics. Advances in technology and a deeper understanding of genetic disorders have led to more tailored treatment options, enhancing patient care.

Government Initiatives: Enhanced government funding and support for genomics projects significantly drive the field forward. These initiatives aim to boost research capabilities and improve healthcare delivery through advanced diagnostic methods.

Technological Advancements: Rapid advancements in sequencing technologies, particularly next-generation sequencing (NGS), have dramatically reduced costs and increased accessibility. The cost of whole genome sequencing has dropped from around $10,000 in 2011 to approximately $1,000 in 2018, making widespread clinical use more feasible.

Market Restraints

Ethical and Privacy Concerns: Concerns about data privacy and security of sensitive genomics data deter people from undergoing genomic testing. Robust data protection regulations are essential to build public trust.

High Costs: Despite the decreasing costs of sequencing, the initial investment required for genomic infrastructure and technology remains high, potentially deterring smaller healthcare facilities from adopting these advancements.

Infrastructure and Skilled Workforce Challenges: Genomics diagnostics industry requires specialized infrastructure and skilled professionals. Developing healthcare infrastructure and a shortage of trained genomics experts pose challenges to market growth.

Regulatory Landscape and Reimbursement Scenario

Mexico's regulatory landscape for genomics features a mix of federal and state-level oversight, with key regulatory bodies playing crucial roles. COFEPRIS (Comisión Federal para la Protección contra Riesgos Sanitarios) is the primary agency responsible for regulating health products and services, including medical devices and in vitro diagnostics, ensuring the safety and efficacy of new genomic tests. The Ministry of Health (Secretaría de Salud or SSa) oversees public health and healthcare policies, defining the role of genomics in the healthcare system. Additionally, state-level health authorities may impose additional regulations or requirements for healthcare providers and laboratories.

Reimbursement for genomic diagnostics in Mexico is influenced by various factors, creating a complex scenario. The public healthcare system offers universal health insurance, but access to services, including genomic tests, varies significantly, with coverage primarily focused on high-impact conditions with clear clinical utility. Private health insurance plans provide varying levels of coverage, with some plans covering certain tests and others imposing limitations or exclusions. Many patients rely on out-of-pocket payments for healthcare, including genomic diagnostics, which can impose a significant financial burden.

Competitive Landscape

Key Players

Here are some of the major key players in the Mexico Genomic Diagnostics

- Illumina, Inc.

- Myriad Genetics, Inc.

- Amgen, Inc.

- 23andMe

- AncestryDNA

- Helix OpCo LLC

- F. Hoffmann-La Roche AG

- Abbott Laboratories

- Danaher Corporation

- Bio-Rad Laboratories Inc.

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Mexico Genomic Diagnostics Market Segmentation

By Technology

- Next Generation Sequencing

- Array Technology

- PCR-based Testing

- FISH

- Others

By Application

- Ancestry & Ethnicity

- Traits Screening

- Genetic Disease Carrier Status

- New Baby Screening

- Health and Wellness-Predisposition/Risk/Tendency

By Product

- Consumables

- Equipment

- Software & Services

By End-user

- Hospitals & Clinics

- Diagnostic Laboratories

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

Indonesia Clinical Diagnostics Market Analysis

Healthcare Services

Senegal Palliative Care Market Analysis

Healthcare Services

Malaysia Patient Adherence Programs Market Analysis

Related reports (by geography)

Pharmaceuticals

Mexico Liver Disease Drugs Market Analysis

Medical Devices

Mexico Cardiac Monitoring Devices Market Analysis

Pharmaceuticals

Mexico Cardiac Arrhythmia Therapeutics Market Analysis

Clinical Trials