Mexico Cardiac Arrhythmia Therapeutics Market Analysis

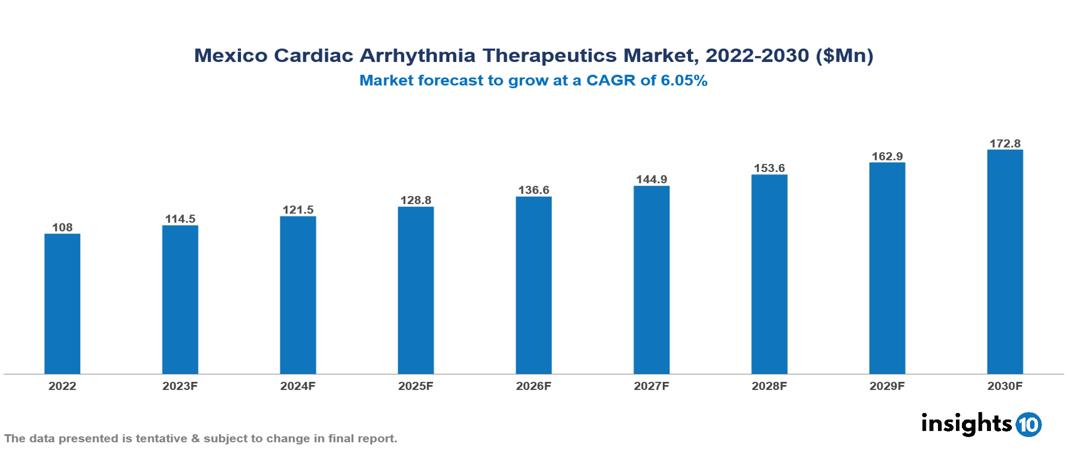

Mexico Cardiac Arrhythmia Therapeutics Market valued at $108 Mn in 2022, projected to reach $173 Mn by 2030 with a 6.05% CAGR. The key drivers of this industry include the increasing prevalence of cardiac conditions, technological advancements, and expanding healthcare infrastructure. The industry is primarily dominated by players such as Abbott, Medtronic, Biotronik, Philips, GE, Johnson & Johnson, and Boston Scientific among others.

Buy Now

Mexico Cardiac Arrhythmia Therapeutics Market Analysis: Executive Summary

Mexico Cardiac Arrhythmia Therapeutics Market valued at $108 Mn in 2022, projected to reach $173 Mn by 2030 with a 6.05% CAGR.

Cardiac arrhythmia, commonly referred to as an irregular heartbeat, is a condition characterized by abnormal heart rhythms, leading to the heart beating too quickly, too slowly, or irregularly. This irregularity can manifest as fluttering, pounding, or racing heartbeats, causing a range of symptoms. Various factors, including heart disease, high blood pressure, diabetes, smoking, excessive alcohol or caffeine consumption, stress, and certain medications, can contribute to the development of arrhythmias. Treatment options for cardiac arrhythmia include medication, cardioversion, catheter ablation, pulmonary vein isolation, and implantable devices like pacemakers and defibrillators. In some cases, surgical intervention may be necessary. Companies such as Abbott, Medtronic, Philips, Hillrom, Nuubo, and others manufacture these treatments. The cardiac arrhythmia therapeutics market is on the rise, driven by the growth of innovative pharmaceuticals and non-invasive therapeutic methods.

The approximate prevalence of atrial fibrillation is about 2% affecting around 0.5 Mn individuals in Mexico. The market is being propelled by important factors such as the increasing burden of cardiovascular diseases, technological advancements in the therapeutics industry, and expanding healthcare infrastructure. However, conditions such as limited accessibility, limited coverage, and lack of awareness limit the growth and potential of the market.

Market Dynamics

Market Growth Drivers

Increase in prevalence of CVDs: Mexico is struggling with an increasing prevalence of CVDs, particularly heart disease, which stands as the primary cause of mortality. Arrhythmias emerge as a complication of CVDs, amplifying both their morbidity and mortality rates. This trend is exacerbated by an aging population and the escalating prevalence of risk factors such as obesity, diabetes, and hypertension. The estimated prevalence of atrial fibrillation is about 2% affecting around 0.5 Mn Mexicans. Unhealthy lifestyle practices, including smoking, excessive alcohol intake, and sedentary behavior, are also becoming more widespread, contributing significantly to the growing incidence of arrhythmias.

Expanding healthcare infrastructure: The government of Mexico is dedicating resources to enhancing healthcare infrastructure and broadening the availability of medical services, particularly in underserved regions. This initiative is contributing to improved access to diagnosis and treatment for arrhythmia among a larger segment of the population. The growing accessibility of health insurance, both from public and private sources, is playing a pivotal role in alleviating the financial strain associated with arrhythmia treatment, thereby fostering the expansion of the market.

Technological advancements: Pharmaceutical firms are consistently innovating by creating novel and enhanced medications to address diverse forms of arrhythmias. These progressions provide more efficient and tailored treatment choices, contributing to the expansion of the market. The rising acceptance of minimally invasive techniques, such as catheter ablation for arrhythmias, is on the upswing owing to their reduced risk and quicker recovery periods. This trend is attracting a larger patient base and bolstering market growth.

Market Restraints

Limited accessibility: A considerable segment of the Mexican populace, especially in rural regions, faces challenges in accessing specialized healthcare facilities and proficient cardiologists. This hampers the timely identification and treatment of cardiac arrhythmias, thereby impeding the growth of the market. Elevated medication costs also contribute to this issue. Although generic alternatives are on the rise, innovative branded therapies for cardiac arrhythmias can be costly, particularly in comparison to the average income. This financial barrier adversely affects a significant portion of the population, limiting the market's reach and penetration.

Limited coverage: Government-backed insurance programs may not comprehensively cover the expenses associated with advanced diagnostics and treatments, resulting in substantial out-of-pocket costs for patients. This lack of comprehensive coverage can dissuade some individuals from pursuing essential healthcare, thereby impacting the potential of the market.

Lack of awareness: Limited public awareness regarding cardiac arrhythmias and their symptoms may result in delayed diagnosis and treatment, impeding the market's potential for growth in both preventive and therapeutic interventions.

Healthcare Policies and Regulatory Landscape

In Mexico, the regulatory authority responsible for overseeing therapeutics, including pharmaceuticals and medical devices, is the Federal Commission for the Protection against Sanitary Risk (Comisión Federal para la Protección contra Riesgos Sanitarios or COFEPRIS). COFEPRIS operates under the jurisdiction of the Ministry of Health and plays a crucial role in ensuring the safety, efficacy, and quality of therapeutic products available in the Mexican market. To obtain licensure for therapeutics, manufacturers must submit comprehensive applications to COFEPRIS, including data on product safety, efficacy, and quality. Once COFEPRIS approves the application, the therapeutic product is granted marketing authorization, allowing it to be legally distributed and sold in Mexico.

The environment for new entrants in the Mexican therapeutic market can be challenging due to stringent regulatory requirements. Navigating the regulatory process can be time-consuming and costly, requiring substantial investments in research, development, and compliance. Despite these challenges, the Mexican healthcare market presents opportunities for companies to address the growing demand for innovative therapeutic solutions.

Competitive Landscape

Key Players

- Abbott

- Medtronic

- GE Healthcare

- Johnson & Johnson

- Koninklijke Philips NV

- Siemens Healthineers

- Biotronik

- Boston Scientific Corporation

- Bayer

- Merck

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Mexico Cardiac Arrhythmia Therapeutics Market Segmentation

By Test Equipment

- Electrocardiogram (ECG)

- Holter monitor

- Others

By Site of Origin

- Atrial Fibrillation

- Sinus Bradycardia

- Atrial Tachycardia

- Atrial Flutter

- Premature Atrial Contractions (PACS)

- Others

By Type

- Supraventricular Tachycardias

- Ventricular Arrhythmias

- Bradyarrhythmia’s

By Drug Type

- Antiarrhythmic drugs

- Calcium channel blockers

- Beta blockers

- Anticoagulants

- Others

By Mode of Administration

- Injectable

- Oral

- Others

By Distribution channel

- Hospital pharmacies

- Retail pharmacies

- Online pharmacies

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Turkey Antiviral Drugs Market Analysis

Brazil Axial Spondyloarthritis (axSpA) Market Analysis

Vietnam Dengue Vaccines Market Analysis

Related reports (by geography)

Mexico Clinical Nutrition Market Analysis

Mexico Coronary Stents Market Analysis

Mexico Women Health Diagnostic Market Analysis