Pharmaceuticals

Mexico Acute Lymphocytic Leukemia (ALL) Therapeutics Market Analysis

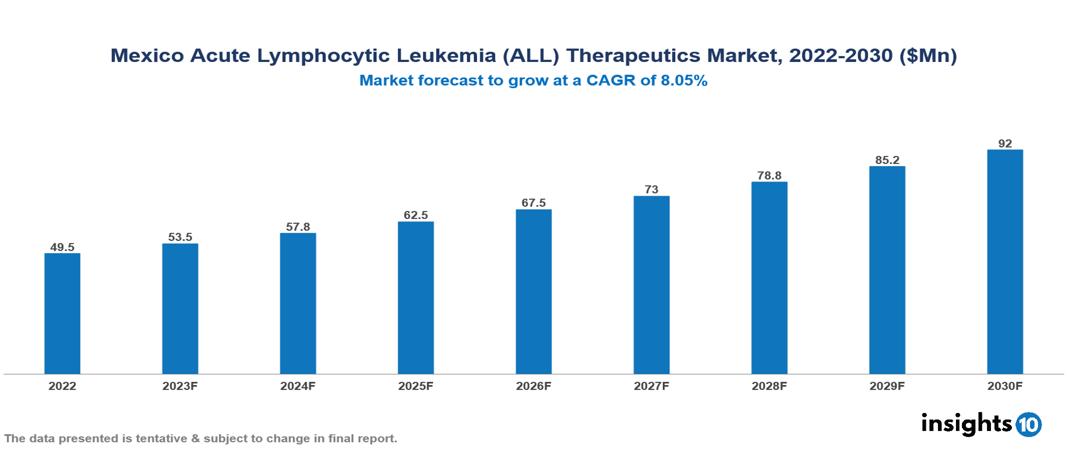

The Mexico Acute Lymphocytic Leukemia (ALL) Therapeutics Market was valued at US $50 Mn in 2022, and is predicted to grow at (CAGR) of 8.05% from 2023 to 2030, to US $92 Mn by 2030. The key drivers of this industry include a surge in the incidence of acute lymphocytic leukemia cases, rising demand for therapeutics, increased government funding initiatives, and other factors. The industry is primarily dominated by players such as Liomont, Novartis, Sanofi, Pfizer Inc, among other players.

Buy Now

Mexico Acute Lymphocytic Leukemia (ALL) Therapeutics Market Analysis

The Mexico Acute Lymphocytic Leukemia (ALL) Therapeutics Market is at around US $50 Mn in 2022 and is projected to reach US $92 Mn in 2030, exhibiting a CAGR of 8.05% during the forecast period.

Acute lymphocytic leukemia (ALL) is a blood and bone marrow cancer that impacts lymphocytes, white blood cells essential for the immune system's functioning. This condition involves the rapid development of immature lymphocytes called lymphoblasts due to a mutation, leading to an accumulation of undifferentiated lymphocytes. Common symptoms include recurring infections, respiratory issues, weight loss, bone pain, and fever, among others. Managing ALL involves a comprehensive and prolonged treatment strategy that comprises chemotherapy, targeted therapies, CAR-T cell immunotherapy, and, in rare cases, stem cell transplantation. These advancements in treatment significantly enhance the possibility of a cure, often achieving notable success rates of approximately 80% in children and adults.

Mexico is a country located in the southern part of North America, ordering the USA. In Mexico, evidence suggests that the overall incidence of ALL is around 44.05%. With improved healthcare infrastructure that allows rapid diagnosis coupled with environmental factors, genetic predisposition, and modifiable risk factors, the prevalence is anticipated to increase. The market is therefore driven by major factors like the surge in the incidence of ALL cases, rising demand for therapeutics, and increased government funding in the therapeutics industry. However, conditions such as an unstable regulatory environment, affordability, and accessibility of therapeutics, among others, hinder the growth and potential of the market.

Market Dynamics

Market Growth Drivers

Increased incidence of ALL: The Instituto Mexicano del Seguro Social (IMSS) estimates that the overall incidence of ALL in Mexico is 44.05%. According to epidemiological studies using population-based registries, the incidence rate of ALL is highest in Mexican children. These statistics indicate the rising burden of ALL, which drives the industry.

Rising demand for therapeutics: The increasing prevalence of ALL in the city and the need for innovative and cost-effective therapeutic treatments are drivers of market growth.

Increased government funding: Mexico runs several initiatives to fund the healthcare needs of the population. The healthcare sector in Mexico has received considerable financing from the government and private players, which is anticipated to propel the growth of the ALL-therapeutics market in the country.

Technological Innovation: Innovation in the therapeutic market is significantly influenced by the expanding leadership of biotechnology in the Mexican health sector, including the use of genetic engineering and biopharmaceuticals. This technical innovation has the potential to contribute to the growth of ALL therapeutics market.

Market Restraints

Access and affordability: Advanced treatments such as CAR-T cell therapy and newer targeted medications are excessively costly for numerous Mexican patients, restricting their access to state-of-the-art treatment alternatives. In addition, the inequity in access of therapeutics acts as a hindrance.

Regulatory landscape: Mexico has a complex regulatory process that can delay its availability to end users.

Healthcare Infrastructure: Inadequate healthcare infrastructure in specific regions, shortages of qualified healthcare professionals, and limited availability of facilities that can provide advanced treatment produce inefficiencies in the system and may impede the availability and use of advanced ALL therapies across Mexico.

Notable updates

February 2023, COFEPRIS, Mexico's regulatory agency, granted approval for the use of Blinatumomab (Blincyto) CAR-T cell therapy in paediatric patients with relapsed or refractory B-cell ALL.

November 2022, COFEPRIS granted approval to Inotuzumab ozogamicin (IOGA), an antibody-drug conjugate for treating relapsed or refractory B-cell ALL in children and adolescents.

Healthcare Policies and Regulatory Landscape

In Mexico, various significant authorities and agencies manage the healthcare policies and regulatory framework. The primary entity overseeing healthcare products, including pharmaceuticals, is the Federal Commission for Protection against Sanitary Risk (COFEPRIS). COFEPRIS holds responsibility for regulating, supervising, and authorizing health-related products, encompassing all therapeutics.

Besides COFEPRIS, the Mexican healthcare system involves a blend of public and private healthcare provisions. The public healthcare sector is managed by the Ministry of Health (Secretaría de Salud), entrusted with the responsibility of delivering healthcare services to the population.

Compliance with COFEPRIS requirements is a prerequisite for obtaining a license in Mexico. Before commercializing therapeutics, companies are required to get registration and marketing licenses from COFEPRIS. Technical and scientific data proving the product's efficacy, safety, and quality must be submitted as part of the registration process.

Mexico has a strong regulatory framework and a resilient healthcare system, creating an advantageous setting for businesses to function effectively. Additionally, its geographical proximity to the United States provides favourable market access, allowing companies to reach and engage with North American markets.

Competitive Landscape

Key Players

- Laboratorios Pisa

- Grupo Biotoscana

- Liomont

- Sanofi

- Pfizer Inc.

- AstraZeneca PLC

- Roche

- Johnson and Johnson

- Vitalmex

- Merck Co & Inc

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Mexico Acute Lymphocytic Leukemia (ALL) Therapeutics Market Segmentation

By Type

- Paediatrics

- Adults

By Drug

- Hyper CVAD regimen

- Linker Regimen

- Nucleoside Metabolic Inhibitors

- Targeted drugs and Immunotherapy

- CALGB 811 Regimen

By Cell

- B Cell ALL

- T Cell ALL

- Philadelphia Chromosome

By Therapy

- Chemotherapy

- Targeted therapy

- Radiation therapy

- Stem Cell Transplantation

By Distribution channel

- Hospital Pharmacy

- Retail Pharmacy

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

UK Antiepileptics Drugs Market Analysis

Pharmaceuticals

Ukraine Cardiovascular Drugs Market Analysis

Pharmaceuticals

US Bone Disease Therapeutics Market

Related reports (by geography)

Medical Devices

Mexico Dental Endodontics Market Analysis

Digital Health

Mexico eHealth Market Analysis

Pharmaceuticals

Mexico Retail Pharmacy Market Analysis

Pharmaceuticals