Pharmaceuticals

Kenya Oncology Therapeutics Market Analysis

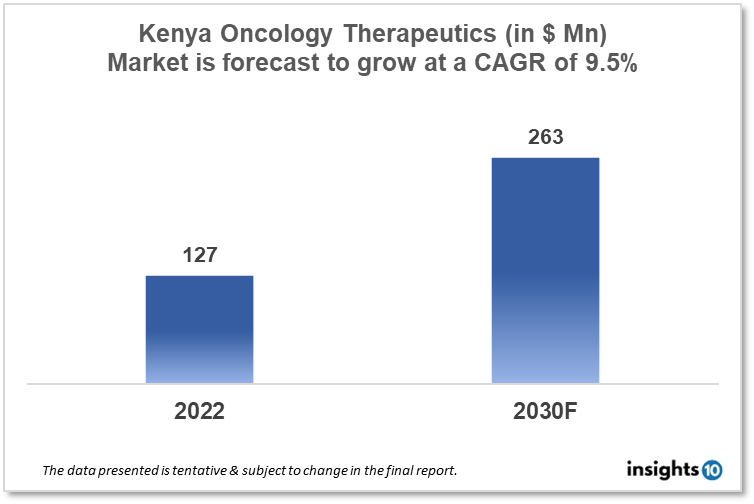

By 2030, it is anticipated that the Kenya Oncology Therapeutics Market will reach a value of $263 Mn from $127 Mn in 2022, growing at a CAGR of 9.5% during 2022-30. The Oncology Therapeutics Market in Kenya is dominated by a few domestic pharmaceutical companies such as Avenue Healthcare, The Nairobi Hospital, and Cancer Care Kenya. The Oncology Therapeutics Market in Kenya is segmented into different types of cancer and different therapy type. The major risk factors associated with cancer are diet, alcohol, tobacco, air pollution, and physical inactivity. The demand for Kenya Oncology Therapeutics is increasing on account of the rise in initiatives taken by the Government of the country.

Buy Now

Kenya Oncology Therapeutics Market Analysis Summary

By 2030, it is anticipated that the Kenya Oncology Therapeutics Market will reach a value of $263 Mn from $127 Mn in 2022, growing at a CAGR of 9.5% during 2022-30.

Kenya is a lower middle-income, developing country in Eastern Africa bordering the Indian Ocean and Lake Victoria. Although progress has been made, such as the Cancer Action Plan, which was released in 2020, basic cancer care is still not where it should be for the majority of Kenyans. The Kenyan Network of Cancer Organizations (KENCO) is the national umbrella group for approximately 45 registered cancer civil society organisations scattered across the country that are working in various elements of cancer management in Kenya and are committed to a collaborative approach to cancer control. Cancer is the third biggest cause of mortality in Kenya, trailing only infectious and cardiovascular disorders.

The Cancer Prevention and Control Act, which establishes the National Cancer Institute to coordinate and govern cancer control activities in the country, is part of the regulatory framework. In terms of reimbursement for oncology services, Kenya has a social health insurance scheme known as the National Hospital Insurance Fund (NHIF). Kenya's government spent 4.6% of its GDP on healthcare in 2020.

Market Dynamics

Market Growth Drivers Analysis

Cancer cases are increasing throughout Kenya's population. The International Agency for Research on Cancer (IARC) GLOBOCAN report for 2018 anticipated 47,887 new cancer cases per year, with 32,987 deaths. The Eldoret Cancer Registry (ECR) provides statistics and epidemiologic profiles for western Kenya. These aspects could boost Kenya's Oncology Therapeutics Market.

Market restraints

Cancer care is extremely expensive in Kenya, and many cancer patients are concerned about both their sickness and the cost of care. These cancer care inequalities can span multiple spectrums and transcend individual characteristics such as ethnicity, religion, gender, and socioeconomic background. They are exacerbated by a scarcity of cancer doctors, a scarcity of community-based cancer centres, low health insurance uptake, a complex health system, poverty and wealth index discrepancies, and climate change.

Despite the fact that tertiary public hospitals serve more than 80% of cancer patients in the country, almost all of whom are in Nairobi, patient volumes and a lack of modern cancer machines cause treatment interruption and long waiting times, resulting in distress as well as time and financial toxicity. Kenya has 0.2 radiation machines per 1,000 cancer patients. These factors may deter new entrants into the Kenya Oncology Therapeutics Market.

Competitive Landscape

Key Players

- Avenue Healthcare: This is a private healthcare provider that offers a range of services, including oncology. They provide cancer screening, diagnosis, and treatment options such as chemotherapy and radiation therapy

- The Nairobi Hospital: This is a leading private hospital in Kenya that offers comprehensive oncology services. They have a dedicated oncology centre that provides cancer screening, diagnosis, and treatment

- Aga Khan University Hospital: This is a private hospital that provides oncology services, including cancer screening, diagnosis, and treatment. They have a team of experienced oncologists who provide personalized treatment plans for each patient

- Cancer Care Kenya: This is a non-profit organization that provides cancer screening, diagnosis, and treatment services to underserved communities in Kenya. They work with a team of oncologists and healthcare providers to provide affordable and accessible cancer care

- Kenyatta National Hospital: This is the largest public hospital in Kenya and provides oncology services, including cancer screening, diagnosis, and treatment. They have a dedicated cancer centre that provides chemotherapy and radiation therapy

Recent Notable Updates

April 2023: Moderna, a renowned pharmaceutical company, stated that it is convinced that vaccinations for cancer, cardiovascular and autoimmune illnesses, and other conditions will be available in Kenya by 2030.

February 2023: In February 2023, the Kenyan government will organise the first-ever National Cancer Summit 2023, concluding in the commemoration of World Cancer Day. This reflects the need for a more coordinated and multi-sectoral response to Kenya's expanding cancer burden.

June 2022: Janssen Kenya, NHIF Sign an agreement to improve access to Prostrate Cancer Drugs. Following the signing of a joint Memorandum of Understanding (MoU) between NHIF and Johnson & Johnson Middle East FZ-LLC (Janssen Kenya), the prescription drug Abiraterone Acetate, which is used to treat advanced prostate cancer, will be made available to NHIF members as part of their current benefits package.

Healthcare Policies and Reimbursement Scenarios

The National Cancer Institute of Kenya was founded in accordance with the Cancer Prevention and Control Act No. 15 of 2012. In Kenya, oncology services are regulated by the Ministry of Health through the National Cancer Control Program (NCCP). The NCCP is responsible for policy formulation, planning, and implementation of cancer control programs, including oncology services. Health care is not publicly funded in Kenya. Most patients pay for health care through insurance schemes or via expensive out-of-pocket costs. According to the National Health Insurance Fund, the leading government-owned insurance company, only 25% of the Kenyan population is insured, not to mention the limited remittances of cancer treatment costs and bureaucratic pre-authorisation hoops.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Oncology Therapeutics Segmentation

By Application (Revenue, USD Billion):

- Blood Cancer

- ?Colorectal Cancer

- Gastrointestinal Cancer

- Gynaecologic Cancer

- Breast Cancer

- Lung Cancer

- Prostate Cancer

- ?Others

By Drugs (Revenue, USD Billion):

- Revlimid

- Avastin

- Herceptin

- Rituxan

- Opdivo

- Gleevec

- Velcade

- Imbruvica

- Ibrance

- Zytiga

- Alimta

- Xtandi

- Tarceva

- Perjeta

- Temodar

- Others

By Therapy (Revenue, USD Billion):

- Chemotherapy

- Targeted Therapy

- Immunotherapy

- Hormonal Therapy

- Others

By Route of Administration (Revenue, USD Billion):

- Oral

- Parenteral

- Others

By Distribution Channel (Revenue, USD Billion):

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- ?Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

US Hypersomnia Therapeutics Market Analysis

Pharmaceuticals

Poland Antifungal Drugs Market Analysis

Pharmaceuticals

Bulgaria Antiviral Drugs Market Analysis

Related reports (by geography)

Digital Health

Kenya 3D Imaging Market Analysis

Pharmaceuticals

Kenya Herceptin Biosimilar Market Analysis

Medical Devices

Kenya Coronary Stents Market Analysis

Pharmaceuticals