Medical Devices

Kenya ENT Devices Market Analysis

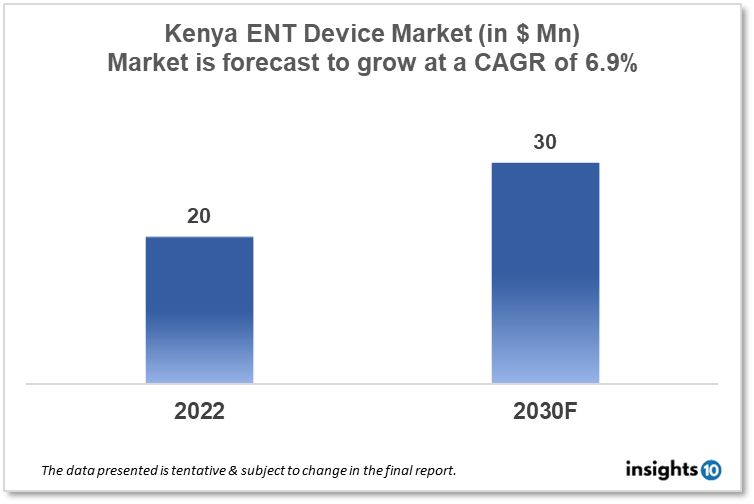

Kenya's ENT Devices Market is projected to grow from $20 Mn in 2022 to $30 Mn by 2030, registering a CAGR of 6.9% during the forecast period of 2022-30. The rising prevalence of ENT disorders, such as hearing loss, sinusitis, and tonsillitis, is a major driver of the ENT device market. The market is highly competitive, with a large number of players operating in the space, ranging from small, specialized companies to large multinational corporations. The domestic key players in the Kenya ENT devices market include Phoenix Equipment, Toda Medical Supplies, and Megascope Healthcare.

Buy Now

Kenya ENT Devices Market Analysis Summary

Kenya's ENT Devices Market is projected to grow from $20 Mn in 2022 to $30 Mn by 2030, registering a CAGR of 6.9% during the forecast period of 2022-30.

Kenya is a lower middle-income, developing country in Eastern Africa bordering the Indian Ocean and Lake Victoria. Kenya's medical device market will increase at an 8.9% CAGR in local currency over the next five years. Leading Kenyan private sector hospital companies invest in cutting-edge technology. Kenya's government spent 4.6% of its GDP on healthcare in 2020.

Market Dynamics

Market Growth Drivers Analysis

Kenya is a promising market for medical equipment, and it is one of the fastest-growing markets in Sub-Saharan Africa. The development of new and advanced ENT devices is moving the Kenyan market ahead. These devices are becoming increasingly complicated, efficient, and cost-effective, allowing them to become more generally available. The public sector, through the Ministry of Health (MOH) and other government-funded agencies, provides over 70% of Kenya's healthcare services. These aspects could boost Kenya's ENT Devices Market.

Market restrains.

Lack of access to healthcare, particularly in rural areas, is one of the major barriers to ENT devices in Kenya. Due to inadequate manufacturing infrastructure and technical capacity, as well as a lack of access to raw materials, the medical device business is primarily reliant on imports, with limited domestic production. These factors may deter new entrants into the Kenya ENT Devices Market.

Competitive Landscape

Key Players

- Megascope Healthcare: Megascope Healthcare is widely recognised as the most reliable supplier of quality medical equipment in Kenya, offering a wide selection of quality and affordable medical equipment

- Phoenix Equipment: The company is registered in Kenya as a supplier of medical equipment and solutions for the hospital field and homecare use with efficient distribution channels to supply efficiently across Eastern Africa

- Toda Medical Supplies: Toda Ltd is regionally recognised as a distributor of medical equipment and devices for Intervention radiology, ENT, neurosurgery, cardiovascular, urology and general surgery

- Medmax

- Angelica Medical Supplies

- Promech Enterprise

Healthcare Policies and Reimbursement Scenarios

In Kenya, medical devices, including ENT devices, are regulated by the Pharmacy and Poisons Board (PPB) under the Ministry of Health. The PPB is in charge of medical device registration, licencing, and regulation in the country. Manufacturers must obtain PPB approval before they can market and sell their devices in Kenya. In the public sector, the reimbursement of ENT devices is determined by the policies of the National Hospital Insurance Fund (NHIF), which is a government agency that provides social health insurance coverage to Kenyan citizens. The country’s Universal Healthcare Coverage (UHC) program prioritizes broadening access to services, strengthening primary healthcare, increasing medical staff and medical supplies, digitizing health operations, and scaling up the National Health Insurance Fund (NHIF).

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

ENT Device Market Segmentation

The ENT Device Market is segmented as mentioned below:

By Product Type (Revenue, USD Billion):

- Diagnostic Devices

- Surgical Devices

- Hearing Aids

- Hearing Implants

- Co2 Lasers

- Image-Guided Surgery Systems

By Diagnostic Devices (Revenue, USD Billion):

- Endocsopes

- Hearing Screening Devices

By Surgical Device (Revenue, USD Billion):

- Powered Surgical Instruments

- Radiofrequency (RF) Handpieces

- Handheld Instruments

- Balloon Sinus Dilation Devices

- ENT Supplies

- Ear Tubes

- Voice Prosthesis Devices

By End Users (Revenue, USD Billion):

- Hospitals and Ambulatory Settings

- Home Use

- ENT Clinics

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

South Africa Bariatric Surgery Devices Market Analysis

Medical Devices

North America Neurology Devices Market Analysis

Medical Devices

Brazil Hemodialysis Equipment Market Analysis

Related reports (by geography)

Pharmaceuticals

Kenya Rabies Vaccine Market Analysis

Pharmaceuticals

Kenya Hypersomnia Therapeutics Market Analysis

Pharmaceuticals

Kenya Ophthalmic Drugs Market Analysis

Pharmaceuticals