Pharmaceuticals

Kenya Conjunctivitis Therapeutics Market Analysis

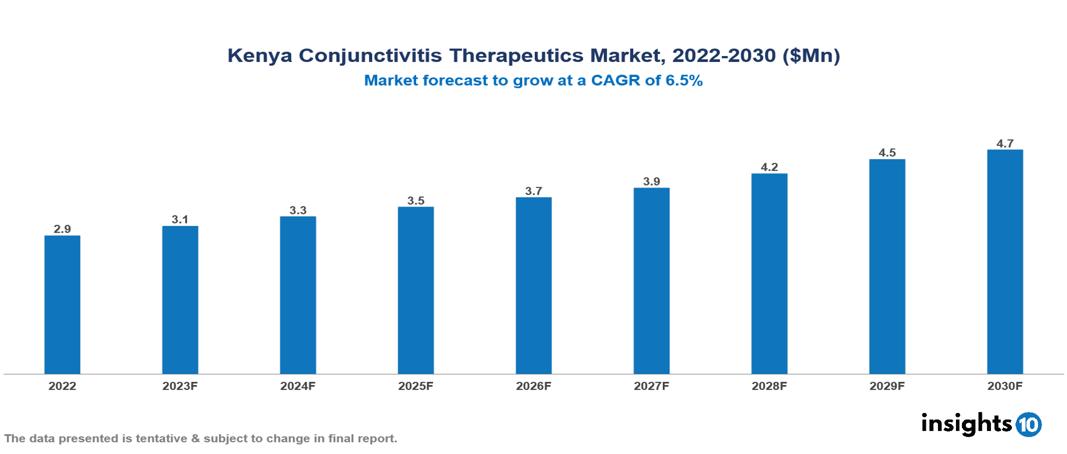

The Kenya Conjunctivitis Therapeutics Market was valued at $3 Mn in 2022 and is predicted to grow at a CAGR of 6.5% from 2023 to 2030, to $5 Mn by 2030. The key drivers of this industry include the rising prevalence of conjunctivitis, the growing pharmaceutical industry, and supportive government initiatives. The industry is primarily dominated by players such as Allergan, Novartis, Sirion, Boehringer Ingelheim, Pfizer, and others.

Buy Now

Kenya Conjunctivitis Therapeutics Market Analysis Executive Summary

The Kenya Conjunctivitis Therapeutics Market is at around $3 Mn in 2022 and is projected to reach $5 Mn in 2030, exhibiting a CAGR of 6.5% during the forecast period.

Conjunctivitis, known as pink eye, is an infection of the conjunctiva, a transparent membrane that covers the white portion of the eye. Factors like microbial infections, allergen exposure, or irritation from certain substances cause it. Viral conjunctivitis is associated with respiratory conditions, while bacterial conjunctivitis can be caused by bacteria such as Staphylococcus and Streptococcus. Allergic conjunctivitis is triggered by allergens like pollen or pet dander, provoking an immune response in the eyes. Additionally, irritants such as smoke, dust, or exposure to chemicals can also induce conjunctivitis. Common symptoms of conjunctivitis include redness, itching, tearing, and a discharge that may cause the eyelids to stick together. While viral conjunctivitis typically resolves on its own, bacterial conjunctivitis may require the use of antibiotic eye drops or ointments for treatment. Allergic conjunctivitis can be managed with antihistamines or anti-inflammatory eye drops. Over-the-counter artificial tears may provide relief in certain cases. Several pharmaceutical companies, including Novartis, Alcon, Allergan, and Bausch + Lomb, produce medications for treating conjunctivitis, offering a variety of prescription and over-the-counter options to address different causes and severity levels of the condition.

Kenya faces a considerable burden of allergic conjunctivitis which affects more than 27% of the adult population. The market growth is fuelled by major contributors such as the surge in the burden of conjunctivitis, the growing pharmaceutical industry, and supportive government initiatives. However, conditions such as limited healthcare infrastructure, affordability challenges, and the presence of counterfeit medications limit the growth and potential of the market.

Market Dynamics

Market Growth Drivers

Rising prevalence of conjunctivitis: Allergic conjunctivitis affects more than 27% of the Kenyan population. The climate in Kenya, characterized by elevated temperatures and dust, provides conducive conditions for the occurrence of bacterial and viral conjunctivitis. Poor sanitation and hygiene help to transmit infection. The increasing urbanization and widespread use of digital devices, which leads to prolonged screen time, causes symptoms such as dry eye, raising the risk of conjunctivitis.

Growing pharmaceutical industry: The Kenyan government prioritizes healthcare access and reduced costs, which benefits the pharmaceutical industry. Increased production of conjunctivitis treatments reduces costs while improving availability, which contributes to market growth. Growing foreign investment in Kenya's pharmaceutical sector promotes the development of new technology and treatments, hence driving market expansion.

Supportive government initiatives: The Kenyan government has taken several initiatives to enhance eye health, including the National Eye Health Policy and the Vision Impact program. These initiatives increase investment in the market for conjunctivitis treatments and promote market growth

Market Restraints

Limited healthcare infrastructure: In Kenya, resource constraints result in limited healthcare facilities, equipment, and staff, hindering access to early diagnosis and treatment, particularly in rural areas. Furthermore, a lack of awareness among the community about conjunctivitis and treatment modalities slows down market growth.

Affordability challenges: A large percentage of the population cannot afford medical treatment due to the high cost of imported medicines and a lack of generic alternatives. Out-of-pocket healthcare costs are a constraint for patients with financial barriers.

Presence of counterfeit medications: The presence of counterfeit drugs on the market constitutes a serious risk to public health as they may be ineffective. Inadequate quality control systems provide barriers to ensuring the safety and efficacy of available drugs.

Healthcare Policies and Regulatory Landscape

The Pharmacy and Poisons Board (PPB) is Kenya's major regulatory authority in charge of medication and pharmaceutical registration and licensing. The PPB is a government institution within the Ministry of Health that ensures the safety, efficacy, and quality of pharmaceuticals in the country.

To get medication and pharmaceutical licenses, companies have to submit applications to the PPB that include data on the product's efficacy and quality. The PPB reviews these submissions with international standards and post-approval, a product is granted a marketing authorization, allowing it to be marketed and distributed legally in Kenya.

For new entrants into the healthcare sector, navigating the regulatory environment in Kenya necessitates a deep understanding of the PPB's requirements and procedures. Inspections of production facilities, submission of clinical trial data, and adherence to good manufacturing practices are all possible steps in this procedure.

Competitive Landscape

Key Players

- Alcon

- Sirion Therapeutics

- Regeneron Pharmaceuticals

- Auven Therapeutics

- Bausch & Lomb

- Boeringer Ingelheim

- Sanofi

- Pfizer

- Allergan

- Novartis

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Kenya Conjunctivitis Therapeutics Market Segmentation

By Drug Class

- Antibiotics

- Antiviral

- Antiallergic

- Others

By Treatment

- Mast Cell Stabilizers

- Decongestant

- Immunotherapy

- Antihistamines

- Non-steroidal anti-inflammatory drugs

- Olopatadine

- Epinastine

- Others

By Disease Type

- Bacterial

- Chemical

- Viral

- Allergic

By Formulation

- Ointment

- Drops

- Drugs

By End Users

- Hospitals and clinics

- Online Pharmacies

- Retail Pharmacies

- Drug Stores

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Poland HIV Therapeutics Market Analysis

Pharmaceuticals

Philippines Pharmaceutical Market Analysis

Pharmaceuticals

Global Antifungal Drugs Market Analysis

Related reports (by geography)

Pharmaceuticals

Kenya Glutathione Market Analysis

Pharmaceuticals

Kenya Optogenetics Market Analysis

Digital Health

Kenya Mental Health Apps Market Analysis

Pharmaceuticals