Pharmaceuticals

Kenya Central Nervous System (CNS) Therapeutics Market Analysis

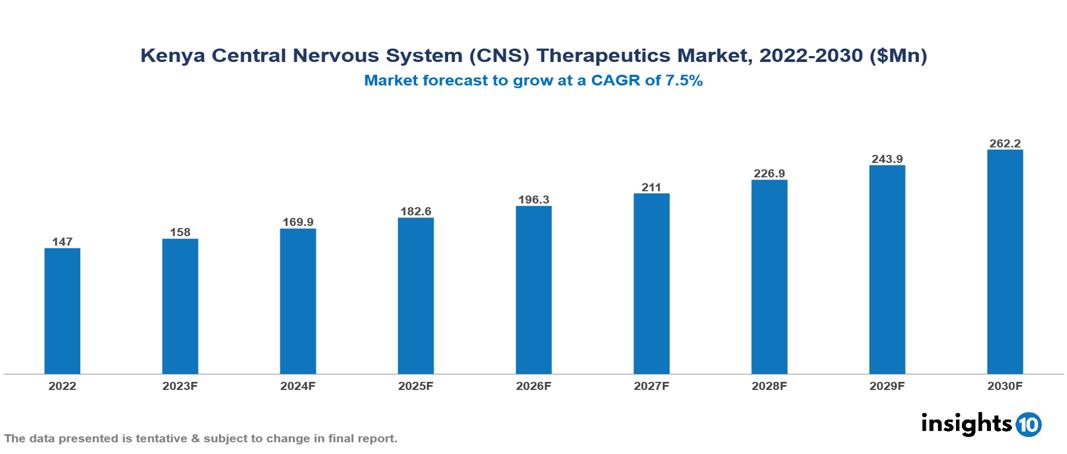

The Kenya Central Nervous System (CNS) Therapeutics Market was valued at $147 Mn in 2022 and is predicted to grow at a CAGR of 7.5% from 2023 to 2030, to $262 Mn by 2030. The key drivers of this industry include the increasing prevalence of CNS disorders, increasing government investments, and technological advancements. The industry is primarily dominated by players such as Afinus, Novartis, Sanofi, AstraZeneca, Dinlas, Pfizer, and Roche among others.

Buy Now

Kenya Central Nervous System (CNS) Therapeutics Market Analysis

The Kenya Central Nervous System (CNS)Therapeutics Market is at around $147 Mn in 2022 and is projected to reach $262 Mn in 2030, exhibiting a CAGR of 7.5% during the forecast period.

Diseases affecting the Central Nervous System (CNS) comprise a broad spectrum of medical conditions that disrupt the normal functioning of the brain and spinal cord. These disorders are categorized into various groups, such as neurodegenerative diseases like Alzheimer's and Parkinson's, psychological conditions including depression and schizophrenia, and neurological disorders like epilepsy and multiple sclerosis. The causes of CNS disorders are diverse, encompassing genetic factors, environmental influences, infections, injuries, or autoimmune responses. Symptoms of CNS disorders vary based on the specific condition but often involve changes in cognitive function, motor skills, mood, or sensory perception. Current treatments for these conditions aim to alleviate symptoms, slow disease progression, or manage complications. Treatment options include medication, psychotherapy, and, in certain cases, surgery. Major pharmaceutical companies, including Pfizer, Eli Lilly, and Johnson & Johnson, play an active role in producing medications for CNS disorders. For example, Pfizer is involved in manufacturing medications for Alzheimer's disease, and Eli Lilly is recognized for its contributions to psychiatric medications.

Kenya faces a substantial health burden due to neurological disorders with an estimated prevalence of more than 19% for conditions like depression. The market therefore is propelled by significant factors like a surge in the prevalence of CNS disorder, increasing government investments, and technological advancements. However, affordability challenges, socioeconomic challenges, and lack of awareness limit the growth and potential of the market.

Market Dynamics

Market Growth Drivers

Increasing prevalence of neurological diseases: Kenya is struggling with a rising incidence of mental health conditions, including widespread cases of depression, anxiety, substance abuse, epilepsy, stroke, and dementia with an estimated prevalence of more than 19%. Factors such as an aging population, evolving lifestyles, and limited access to preventative healthcare are contributing to this trend, necessitating the development of more treatment options. Furthermore, non-communicable diseases like diabetes and hypertension can give rise to complications in the central nervous system, intensifying the need for CNS therapeutics in Kenya.

Increasing government initiatives and investments: The Kenyan government is increasing its investment in healthcare, specifically targeting mental health and neurological disorders. This involves the construction of treatment facilities, the training of healthcare professionals, and the subsidization of medication expenses. Mental health policies, such as the Mental Health Policy 2015 and the National Mental Health Strategy 2019-2024, emphasize the importance of ensuring access to mental healthcare services and medications, thereby promoting market expansion. Collaborations with international entities like the World Health Organization (WHO) and UNICEF are also playing a crucial role in bringing resources and expertise to enhance access to CNS therapeutics.

Technological advances: Pharmaceutical firms are actively engaged in the exploration and creation of novel, improved, and cost-effective medications for CNS disorders, providing optimism for individuals with previously untreatable conditions. Progress in genetics is facilitating the emergence of personalized medicine, customizing treatments based on individual patient characteristics for enhanced outcomes.

Market Restraints

Lack of awareness and social stigma: In Kenyan society, mental health issues frequently face stigma, resulting in underdiagnosis and postponed pursuit of treatment. A considerable number of Kenyans lack a fundamental understanding of CNS disorders, their symptoms, and the treatment options accessible. The limited public awareness regarding mental health conditions and available treatments exacerbates the stigma and obstructs individuals from seeking help promptly.

Affordability challenges: Kenya's per capita healthcare expenditure is comparatively modest when compared to that of developed nations, restricting the accessibility of costly CNS treatments. The high prices of imported CNS drugs pose a significant challenge, surpassing the financial means of numerous Kenyan individuals. Additionally, the uneven distribution of healthcare facilities results in limited access to specialized healthcare providers and medications in rural areas, exacerbating the marginalization of vulnerable populations.

Healthcare Policies and Regulatory Landscape

In Kenya, the main regulatory body overseeing the registration and licensure of drugs and pharmaceuticals is the Pharmacy and Poisons Board (PPB). The PPB operates under the Ministry of Health and is responsible for ensuring the quality, safety, and efficacy of pharmaceutical products in the country.

The registration process for obtaining licensure for drugs involves rigorous evaluation of the product's documentation, including information on its manufacturing, quality control, and clinical trials. The PPB assesses whether the drug meets the required standards and complies with regulatory guidelines before granting approval for marketing and distribution.

The regulatory environment for new entrants in the pharmaceutical industry in Kenya is characterized by a commitment to safeguard public health. Companies seeking to introduce new drugs or pharmaceuticals must adhere to stringent regulatory requirements set by the PPB. This includes providing comprehensive data on the product's formulation, manufacturing processes, and evidence of its safety and efficacy. The PPB ensures compliance with international standards, and successful registration is a prerequisite for market entry.

Competitive Landscape

Key Players

- Novartis

- Roche

- Pfizer

- Boehringer Ingelheim

- Eli Lilly

- Dinlas Pharmaceuticals

- AstraZeneca

- Afinus Pharmaceuticals

- Sanofi

- GSK plc

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Kenya Central Nervous System (CNS) Therapeutics Market Segmentation

By Drug

- Biologics

- Non-Biologics

By Drug Class

- Antidepressants

- Analgesics

- Immunomodulators

- Interferons

- Decarboxylase Inhibitors

- Others

By Disease

- Neurovascular Disease

- Degenerative Disease

- Infectious Disease

- Mental Health

- CNS Cancer

- Others

By Distribution Channel

- Hospital based pharmacies

- Retail pharmacies

- Online pharmacies

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

US Central Nervous System (CNS) Therapeutics Market Analysis

Pharmaceuticals

France Neurology Drugs Market Analysis

Pharmaceuticals

Brazil Interstitial Cystitis Drugs Market Analysis

Related reports (by geography)

Pharmaceuticals

Kenya Dermatology Drugs Market Analysis

Clinical Trials

Kenya Clinical Trials Support Service Market Analysis

Pharmaceuticals

Kenya Liver Cancer Drugs Market Analysis

Healthcare Services