Pharmaceuticals

Kenya Autosomal Dominant Polycystic Kidney Disease Therapeutics Market Analysis

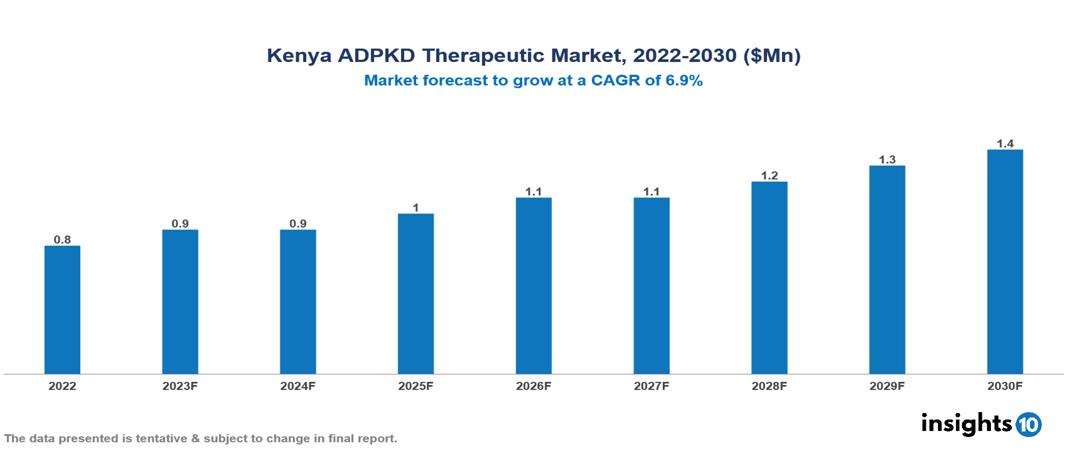

The Kenya Autosomal Dominant Polycystic Kidney Disease Therapeutics Market was valued at US $0.8 Mn in 2022, and is predicted to grow at (CAGR) of 6.9% from 2023 to 2030, to US $1.4 Mn by 2030. The key drivers of this industry include the several government initiatives and policies to support rare diseases and increased awareness among the population regarding the condition. The industry is primarily dominated by players such as Otsuka Pharmaceutical, AceLink Therapeutics, Palladio Biosciences, Reata Pharmaceutica, Xortx, Regulus Therapeutics, Galapagos NV among others

Buy Now

Kenya Autosomal Dominant Polycystic Kidney Disease Therapeutics Market Analysis

The Kenya Autosomal Dominant Polycystic Kidney Disease Therapeutics Market is at around US $0.8 Mn in 2022 and is projected to reach US $1.4 Mn in 2030, exhibiting a CAGR of 6.9% during the forecast period.

Autosomal dominant polycystic kidney disease (ADPKD) is a hereditary disorder that affects several systems and is caused by mutations in the PKD1 and PKD2 genes. It is characterized by the formation of many cysts within the kidneys, resulting in renomegaly, and most patients progress to end-stage kidney disease (ESKD). While there is no cure for ADPKD currently, there are a few therapeutic options available for the management of symptoms and disease progression. Tolvaptan (Jinarc), a drug developed by Otsuka Pharmaceutical Co. Ltd., is approved in many countries and belongs to the class of vasopressin V2 receptor antagonists (V2RAs). Tolvaptan has been shown to slow the rate of cyst formation and the decline in kidney function in some patients with ADPKD. Other therapeutic options include pain management and lifestyle modifications.

The prevalence of ADPKD in Kenya is presumably low as compared to other countries, and the exact prevalence estimate remains unknown. The market is therefore driven by major factors like government initiatives towards making ADPKD a priority condition and increased awareness about the condition in the population. However, conditions such as the non-availability of diagnostic modalities that lead to underdiagnosis in several cases, financial barriers to accessing expensive treatment, and other factors hinder the growth and potential of the market.

Market Dynamics

Market Growth Drivers

Government initiatives: The Kenyan government has started focusing its attention on diseases like ADPKD and has considered it a priority. It is working towards several policies that support rare disorders, reimbursement programs, and taxation for pharmaceuticals looking to enter the market, fostering expansion of the market.

Increased awareness: The Kenyan market for ADPKD treatments is seeing growth due to the proactive efforts of both governments, such as the Kenya Renal Association, and global market developments. They advocate for increased research funding, improved healthcare access, and public education. This drives market expansion by promoting early detection, appropriate treatment options, and complete disease management measures.

Market Restraints

Limited knowledge on prevalence: The prevalence of ADPKD is considered to be presumably low as compared to all countries due to the limited availability of data about the condition. There are no clear statistics available to estimate the overall prevalence, which can therefore delay the growth of the therapeutics market.

Underdiagnosis: The knowledge regarding the disease among professionals as well as the general population in Kenya is limited, resulting in delayed diagnosis and treatment of suspected patients. Diagnostic services, including ultrasonography and genetic testing for confirmed diagnosis, are limitedly available in public sector centres. This results in missed opportunities for case detection and hinders market growth.

Financial barriers: Existing treatment for ADPKD which is Tolvaptan, can be costly, causing a considerable financial burden on both Kenyan patients and the healthcare system. A considerable segment of the Kenyan population lives below the poverty line and does not have secured insurance options, which further limits their access to expensive treatments. Affordability concerns result in treatment non-adherence in many patients, which digresses from the growth of the market.

Healthcare Policies and Regulatory Landscape

Kenya's healthcare policy and regulatory structure are complex, with several governing organizations and licensing systems. As the primary authority, the Ministry of Health (MoH) establishes healthcare policies, rules, and benchmarks. The Ministry of Health governs healthcare establishments, licenses healthcare practitioners, and regulates drugs and medical equipment. The Kenya Medical Supplies Authority is in charge of acquiring and distributing essential medicines and medical supplies to public health facilities across the country. It is critical to guaranteeing the affordability and accessibility of basic healthcare services.

The Pharmacy and Poisons Board (PPB) regulates pharmaceuticals, medical equipment, and cosmetics, as well as ensuring their efficacy and safety. It issues licenses for the manufacture, importation, sale, and distribution of various items. The country's governmental and private healthcare industries both provide multiple opportunities for healthcare-related organizations.

Competitive Landscape

Key Players

- Otsuka Pharmaceutical Co. Ltd

- Regulus Therapeutics

- Palladio Biosciences

- Reata Pharmaceuticals

- Galapagos NV

- Exelixis Inc

- AceLink Therapeutics, Inc

- Sanofi

- Xortx Therapeutics

- Pano Therapeutics

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Kenya Autosomal Dominant Polycystic Kidney Disease Therapeutics Market Segmentation

By Treatment

- Pain & Inflammation Treatment

- Kidney Stone Treatment

- Urinary Tract Infection Treatment

- Kidney Failure Treatment

By Route of Administration

- Oral

- Parenteral

- Others

By End User

- Hospitals

- Speciality Clinics

- Surgical Centres

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Portugal Cardiovascular Diseases Therapeutics Market Analysis

Pharmaceuticals

Mexico Inflammatory Bowel Disease (IBD) Drugs Market Analysis

Pharmaceuticals

Netherlands Oncology Therapeutics Market Analysis

Related reports (by geography)

Pharmaceuticals

Kenya Opioid Use Disorder Market Analysis

Pharmaceuticals

Kenya Varicella Vaccine Market Analysis

Pharmaceuticals