Pharmaceuticals

Kenya Acute Lymphocytic Leukemia (ALL) Therapeutics Market Analysis

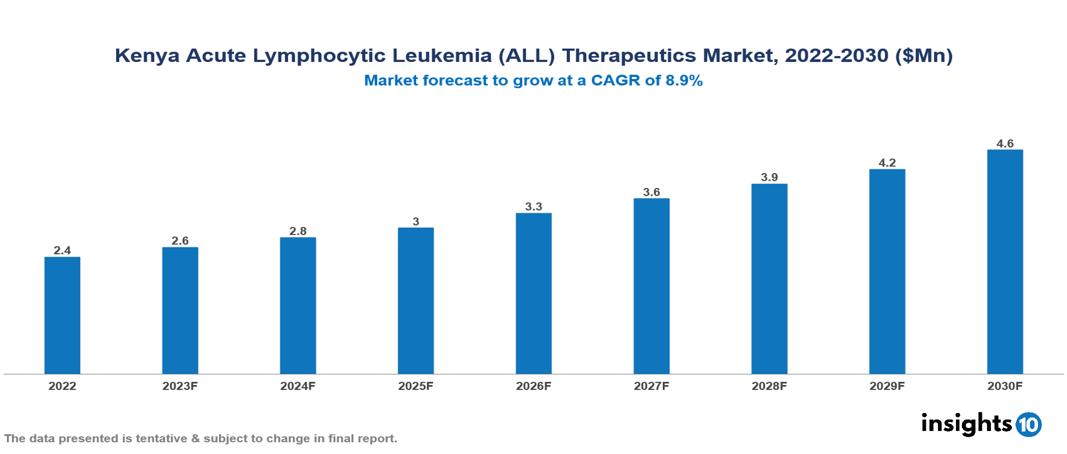

The Kenya Acute Lymphocytic Leukemia (ALL) Therapeutics Market was valued at US $2 Mn in 2022, and is predicted to grow at (CAGR) of 8.9% from 2023 to 2030, to US $5 Mn by 2030. The key drivers of this industry include a surge in the incidence of acute lymphocytic leukemia cases, high unmet needs, increased government initiatives, and other factors. The industry is primarily dominated by players such as Universal Corporation, Bio-Ken, Toxin, Avenue Healthcare, and Novartis among other players

Buy Now

Kenya Acute Lymphocytic Leukemia (ALL) Therapeutics Market Analysis

The Kenya Acute Lymphocytic Leukemia (ALL) Therapeutics Market is at around US $2 Mn in 2022 and is projected to reach US $5 Mn in 2030, exhibiting a CAGR of 8.9% during the forecast period.

Acute lymphocytic leukemia (ALL) is a blood and bone marrow cancer impacting lymphocytes, essential white blood cells for infection defence. In this condition, immature lymphocytes rapidly multiply, overwhelming healthy blood cells and disrupting their normal functions. Symptoms comprise recurring infections, weight loss, fever, and other associated indications. Managing ALL necessitates an extensive and prolonged treatment regimen incorporating therapies like chemotherapy, targeted treatments, CAR-T cell immunotherapy, and, in severe cases, stem cell transplantation. These advancements substantially increase the chances of a cure, often achieving substantial success rates of around 80%.

Estimates report that ALL accounts for up to 14.9% of childhood malignancies in Kenya in the ages of 0 and 15. In Kenya, the incidence of ALL is 4.8/1,000,000 males and 4.5/1,000,000 females. The market is therefore driven by major factors like the surge in incidence of ALL cases, the high unmet needs of diseased individuals, and increased government initiatives in the therapeutics industry. However, conditions such as high costs of treatment, treatment non-compliance, and others hinder the growth and potential of the market.

Market Dynamics

Market Growth Drivers

Increased cases of ALL: The incidence trends of ALL in Kenya are 4.8/1,00,000 males and 4.5/1,00,000 females. ALL accounts for 14.9% of childhood cancers affecting children between the ages of 0 and 15 years. The proportion of ALL has increased and is anticipated to increase further in the forecasted period.

High unmet need: Owing to the huge population of Kenya suffering from ALL, there is a rising demand for lifesaving and advanced treatment options for these patients due to an imbalance between patient demand and supply. This creates opportunities that allow market growth.

Increased government initiatives: The government introduced Universal Health Coverage (UHC) in 2018, which strives to offer fundamental healthcare coverage to all Kenyan citizens, encompassing accessibility to vital cancer treatments such as ALL chemotherapy. It has also launched the National Cancer Control Strategy, aiming at a holistic approach to ALL treatments, fueling market expansion.

Market Restraints

Side effects of drugs: The primary reason for event-free survival n children and adults in Kenya is premature death from therapeutic-related complications, including drugs and surgery. This can explain the growth of the market.

Treatment non-adherence: The incidence of ALL in Kenya is exponentially rising; however, there are lower survival rates and poor clinical outcomes due to treatment non-adherence. Cultural views and a lack of proper knowledge may contribute to patient non-compliance or treatment interruptions, which could have an impact on the continuation of ALL therapy.

High cost: There are challenges concerning the accessibility and affordability of laboratory tests. Numerous families face difficulties affording the required laboratory studies necessary for optimal risk-oriented therapy, potentially surpassing the financial means of many patients and the limits of their healthcare coverage.

Limited local expertise: Kenya’s dependence on imported ALL therapeutics subjects it to global market dynamics and pricing structures. The absence of local manufacturing capacities for vital medications or engaging in partnerships with neighbouring regions drives up the cost of the therapeutic market. Additionally, the absence of specialised treatment centres and expert hematologists and oncologists can restrict market growth.

Healthcare Policies and Regulatory Landscape

Kenya's healthcare policy and regulatory structure are intricate, comprising multiple governing bodies and procedures for acquiring licenses. The Ministry of Health (MoH) serves as the primary authority; it establishes healthcare policies, regulations, and benchmarks. The MoH supervises healthcare establishments, licenses healthcare practitioners, and oversees the regulation of pharmaceuticals and medical equipment. Kenya Medical Supplies Authority is responsible for procuring and disseminating vital medicines and medical supplies across public health facilities nationwide. It plays a pivotal role in ensuring the affordability and accessibility of fundamental healthcare services.

Pharmaceuticals, medical equipment, and cosmetics are regulated by the Pharmacy and Poisons Board (PPB), which also ensures their efficacy and safety. It grants licenses for the production, importing, selling, and distribution of various goods. Prior to marketing or utilization in Kenya, companies are obligated to register their products with the PPB. This registration procedure entails comprehensive documentation, clinical trial data submission, and scrutiny by PPB specialists. Additionally, adherence to Good Manufacturing Practices (GMP) and Good Clinical Practice (GCP) regulations is imperative for these companies.

Both the public and private healthcare sectors in the country offer diverse opportunities for companies operating within the healthcare industry.

Competitive Landscape

Key Players

- Tonix Pharmaceuticals

- Bio-Ken

- Avenue Healthcare

- Medisel Kenya

- Universal Corporation

- Kenya Vaccines and Immunizations Institute

- Sanofi-Aventis

- Novartis

- Pfizer

- Merck & Co

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Kenya Acute Lymphocytic Leukemia (ALL) Therapeutics Market Segmentation

By Type

- Paediatrics

- Adults

By Drug

- Hyper CVAD regimen

- Linker Regimen

- Nucleoside Metabolic Inhibitors

- Targeted drugs and Immunotherapy

- CALGB 811 Regimen

By Cell

- B Cell ALL

- T Cell ALL

- Philadelphia Chromosome

By Therapy

- Chemotherapy

- Targeted therapy

- Radiation therapy

- Stem Cell Transplantation

By Distribution channel

- Hospital Pharmacy

- Retail Pharmacy

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Japan Infection Control Supplies Market Analysis

Pharmaceuticals

Malaysia Cardiovascular Drugs Market Analysis

Pharmaceuticals

Switzerland Anti Aging Therapeutics Market Analysis

Related reports (by geography)

Medical Devices

Kenya Cardiac Surgery Instruments Market Analysis

Pharmaceuticals

Kenya Paracetamol Market Analysis

Pharmaceuticals

Kenya Anticoagulants Market Analysis

Pharmaceuticals