Pharmaceuticals

Japan Alzheimer’s Therapeutics Market Analysis

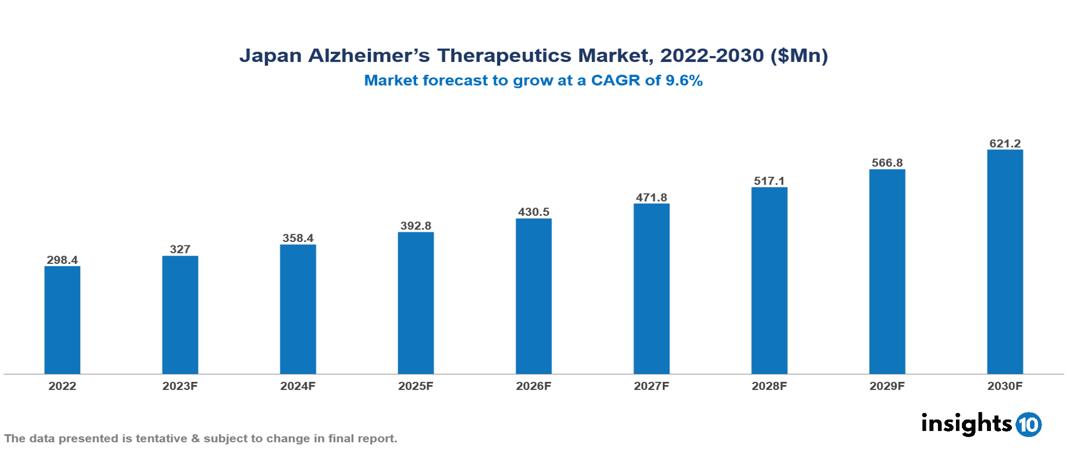

Japan alzheimer’s therapeutics market valued at $298 Mn in 2022, projected to reach $621 Mn by 2030 with a 9.6% CAGR. The growing prevalence of Alzheimer's disease, which is fuelled by an aging population, is one major factor driving the market for drugs used to treat the condition. The leading pharmaceutical companies currently operating in the market are Eisai, Otsuka Holdings Co., Astellas Pharma Inc., Mitsubishi Tanabe Pharma Corporation, Sumitomo Dainippon Pharma Co., Takeda Pharmaceutical Company, Roche Holding, Novartis, Pfizer, and Lundbec.

Buy Now

Japan Alzheimer’s Therapeutics Market Executive Summary

Japan alzheimer’s therapeutics market valued at $298 Mn in 2022, projected to reach $621 Mn by 2030 with a 9.6% CAGR.

Alzheimer's disease is a neurological disorder that affects memory, behavior, and mental health. Usually, it begins gradually, worsens over time, and makes it more difficult for the affected individual to do everyday duties. In Alzheimer's disease, aberrant brain changes such as plaque and tangle formation cause nerve cells to die. There is presently no treatment for Alzheimer's disease. On the other hand, some medications can improve quality of life and aid with symptom management. These drugs alter certain neurotransmitters in the brain to treat memory and cognitive problems. Donepezil, rivastigmine, and memantine are a few of these drugs. Maintaining a healthy lifestyle, participating in social and cognitive activities, and creating a supportive environment are examples of non-pharmacological strategies that may enhance overall illness management.

Over 4.6 Mn people in Japan suffer from dementia, accounting for about 7% of those 65 and older. Alzheimer's disease (AD) is the most common type of dementia. Forecasts suggest a worrying increase: by 2025, there will be more than 5.3 Mn dementia sufferers worldwide, and by 2060, that figure will jump to 8.1 Mn. Age is a key factor in prevalence; 10% of people 75 years of age and beyond are thought to have dementia. Regional differences are also apparent, with incidence rates higher in rural than in urban settings, which can be linked to things like restricted access to diagnostic resources and healthcare. The growing prevalence of Alzheimer's disease presents serious obstacles for families, social care providers, and healthcare systems. Underscoring the need for prompt detection and intervention, current research initiatives in Japan and around the world seek to create novel diagnostic techniques, efficacious therapies, and, in the end, a cure for Alzheimer's disease.

LDP-002/GS-9657, a promising Alzheimer's treatment candidate from Otsuka, is presently completing Phase III clinical trials. Results are expected later this year, and the drug is intended to target Tau protein aggregation.

Aiming to lower amyloid-beta and Tau aggregation, Eisai and Sumitomo Dainippon Pharma are now conducting Phase II trials for their respective experimental medications. Apart from this, a multitude of other pharmaceutical businesses operating in Japan are leading the way in the advancement of early-stage clinical trials for possible Alzheimer's medications. Together, these companies add to the ever-changing field of Alzheimer's disease research and treatment development in Japan.

Market Dynamics

Market Growth Drivers

Rising Aging Population: With more than 28% of its population over 65, Japan has the oldest population in the world. Given that the prevalence of Alzheimer's increases with age, this demographic shift immediately translates into an increased risk of the illness.

Growing Awareness and Diagnosis: The stigma associated with Alzheimer's disease is progressively fading, resulting in heightened consciousness and prompt diagnosis. This trend is further supported by easier access to medical facilities and diagnostic technologies like brain scans.

Unaddressed Medical Demand and Changing Treatment Scenario: Alzheimer's disease does not currently have a recognized cure; current treatments only deal with the symptoms. The market for the creation of new, possibly more effective medications is substantial because there are few readily available medical treatments. Better tau-targeting drug development and therapy combinations, together with recent developments with anti-amyloid antibodies like lecanemab, all portend well for more potent treatments in the years to come.

Market Restraints

High Costs: Pharmaceuticals such as Leqembi can cost more than $0.02 million annually, which puts a heavy financial strain on patients and their families. This presents issues with pricing and accessibility, which may restrict drug use and market expansion. The affordability problem is made worse by limited insurance coverage for chronic illnesses like Alzheimer's, which forces patients to pay a large portion of their treatment out of the source.

Limited Access to Specialists: The majority of neurologists and other experts in the treatment of Alzheimer's disease reside in cities. Due to this, rural communities have less access to appropriate diagnosis, care, and follow-up, which hinders patient benefits and market penetration.

Lack of Awareness and Stigma: Despite the increasing number of awareness initiatives, many people are unable to receive a diagnosis and treatment for dementia and Alzheimer's disease due to the ongoing cultural stigma around these conditions. This stigma is one of the primary obstacles keeping the market from reaching a wider range of consumers.

Healthcare Policies and Regulatory Landscape

The Ministry of Health, Labour, and Welfare (MHLW) and the Pharmaceuticals and Medical Devices Agency (PMDA) in Japan collaborate to manage therapeutic drug regulations and healthcare policy. As the main regulatory agency, the PMDA carefully assesses and approves medications by going over clinical trial data, production procedures, and quality control protocols in detail. The PMDA works closely with peers abroad to standardize regulatory requirements. In addition to developing healthcare policy, the MHLW also assists in the development of drug pricing and reimbursement plans, which are supervised by the Central Social Insurance Medical Council (Chuikyo). Preclinical and clinical data are scrutinized closely during the clearance process, and post-marketing surveillance guarantees ongoing safety oversight.

Competitive Landscape

Key Players

- Eisai

- Otsuka Holdings Co.

- Astellas Pharma Inc.

- Mitsubishi Tanabe Pharma Corporation

- Sumitomo Dainippon Pharma Co.

- Takeda Pharmaceutical Company

- Roche Holding

- Novartis

- Pfizer

- Lundbec.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Japan Alzheimer’s Therapeutics Market Segmentation

By Drug Name

- Early-Onset Alzheimer's

- Late-Onset Alzheimer's

- Familial Alzheimer's disease

By Drug Name

- Donepezil

- Rivastigmine

- Memantine

- Galantamine

- Manufactured a combination of memantine and donepezil

By Drug Class

- Cholinesterase Inhibitors

- NMDA Receptor Antagonists

- Manufactured Combination

By End-Users

- Hospitals

- Specialty Clinics

- Homecare

- Others

By Distribution Channel

- Hospital pharmacies

- Drug stores

- Retail pharmacies

- Online pharmacies

- Other distribution channel

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Saudi Arabia Urothelial Carcinoma Market Analysis

Pharmaceuticals

Argentina Orphan Diseases Drugs Market Analysis

Pharmaceuticals

Egypt Anti-Venom Market Analysis

Related reports (by geography)

Pharmaceuticals

Japan Anemia Therapeutics Market Analysis

Pharmaceuticals

Japan Anti-Aging Drugs Market Analysis

Pharmaceuticals