Healthcare Services

Italy Payer Service Market Analysis

Italy Payer Service Market is projected to grow from $xx Mn in 2023 to $xx Mn by 2030, registering a CAGR of xx% during the forecast period of 2023 - 2030. The Payer Service market is expanding due to rising healthcare spending and change in regulatory processes in both developed and developing nations. This demand is fueling the development of better infrastructure and procedures for payer services. Some of the key players in the global payer service Market include UnitedHealth Group, Anthem, Inc., Cigna Corporation, Aetna Inc., Humana Inc., Centene Corporation, Molina Healthcare, Inc., WellCare, Health Net, and Blue Cross Blue Shield Association (BCBS).

Buy Now

Italy Payer Service Market Executive Summary

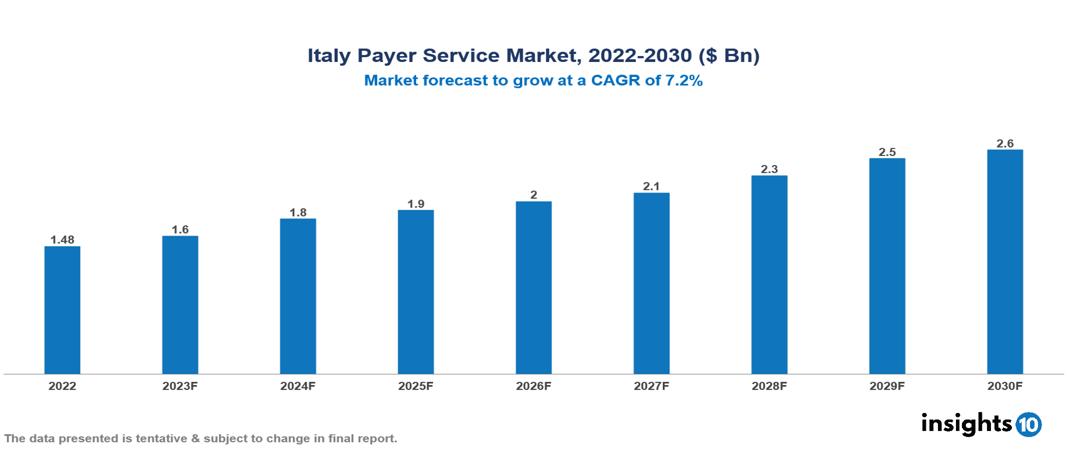

Italy Payer Service Market is valued at around $1.48 Bn in 2022 and is projected to reach $2.58 Bn by 2030, exhibiting a CAGR of 7.2% during the forecast period 2023-2030.

The Payer Service Market refers to the market for Software that helps in financial administration for insurance companies and other healthcare providers and is known as a payer solution. It includes functionality related to billing, claims administration, customer service, and other financial processes. Healthcare payer solutions are important because they help these organizations manage their finances and make sure patients are billed accurately.

Technological advancements like automation, artificial intelligence, RPA, and blockchain solutions have contributed to the growth of the global market for payer services in recent years. Digital tools like mobile applications, telehealth services, and self-service portals are integrated with payer software to improve efficiency and outcome. It has given a boost to the global payer service market.

There are many global players in the payer services market. Still, UnitedHealth Group, Anthem, Inc., Cigna Corporation, Aetna Inc., Humana Inc., Centene Corporation, Molina Healthcare, Inc., WellCare, Health Net, and Blue Cross Blue Shield Association (BCBS) are some of the major players in the market.

The demand for improved supply chain management (SCM) methods and the increase in demand for cost-effective operations are two of the major factors contributing to the growth of this market. During the forecast period, market growth will likely be driven by reducing the overall cost of healthcare supply chain BPO services. Also, as a result of inventory control, there is an increase in demand for healthcare supply chain business process outsourcing. The market is projected to grow throughout the course of the forecast period due to these factors.

The growing demand for healthcare payer services and digitization of the healthcare sector is projected to fuel the market for payer services in the coming years. The market still has difficulties with regard to obtaining regulatory permission, complicated policies and reimbursement processes, as well as data privacy and security concerns.

Market Dynamics

Drivers of Italy Payer Service Market:

Growing demand for healthcare payer service: The market for healthcare payer solutions is expected to grow during the projected period as a result of the rising need for cost-cutting measures and the expansion of healthcare payer service providers. Healthcare payer services that are outsourced are less expensive compared to those that are provided internally. The demand is rising as a result of scientific innovations, increased adoption of healthcare analytics, and an increase in the number of people choosing health insurance. All of these elements are projected to fuel the market for healthcare payer solutions during the forecasted period.

Digitization: Digitization was rapidly adopted by medical practitioners and healthcare providers. A lot of data is being gathered daily about the patients who get services. To effectively coordinate, administer, and carry out plans, health services need an adequate system. Increasing demand for adequate systems has boosted the growth of the payer service market.

Rising Duplicate Insurance Claims: The usage of software improves communication across different hospital domains and subdomains. The program controls patient data and information about their treatment while applying cutting-edge techniques to enable seamless interoperability between insurance companies and hospitals. According to reports, insurance companies deny around one out of every five claims due to similar claims and a lack of transparency. As a result, the utilization of cutting-edge techniques and interoperability between these hospital sectors would help to cut down on the number of false claims. It has increased the demand for payer services and will boost the growth of the market.

Restraints of Italy Payer Service Market:

Data Safety and Privacy: As cybercrime has increased over the past few years, issues about the security of a patient's medical history and other personal information have increased. Some factors limiting market expansion are malware, phishing, Man in the Middle attacks, Trojans, and other emerging cyber threats.

The complexity of the Healthcare System: The healthcare system involves multiple stakeholders, different reimbursement policies, and regulatory models according to different case scenarios. It can be challenging for payer service providers as it requires deep domain expertise, excellent knowledge of regulatory frameworks, and the ability to adapt to changes in these policies. It can hinder the growth of the market for payer services.

Notable Deals in Payers Service Market

In January 2022, the Centers for Medicare and Medicaid Services (CMS) declared that it will increase the application of value-based buying (VBP) in Medicare. With the VBP payment model, healthcare providers are rewarded for offering effective, high-quality care. The delivery of healthcare in the United States is anticipated to change as a result of the growth of VBP.

in March 2022, UnitedHealth Group announced that it would buy Change Healthcare for $17.5 billion. The acquisition is anticipated to assist UnitedHealth Group in growing its payer services business and strengthening its capacity to control healthcare costs.

In April 2022, Humana announced that it would buy Kindred Healthcare for $8.1 billion. The purchase is expected to support Humana in growing its post-acute care business and enhancing its capacity to offer all-inclusive care to its members.

Key players

National Institute for Insurance against Accidents at Work (INAIL) National Health Service (SSN) Generali Allianz Italia UnipolSai Assicurazioni Poste Italiane Cattolica Assicurazioni Reale Mutua Assicurazioni Assicurazioni Generali Lloyd's of London (Italy)1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Market Segmentations For Italy Payer Service Market

By Service:

- BPO Services

- ITO Services

- KPO Services

By Application:

- Claims Management Services

- Integrated Front Office Service and Back Office Operations

- Member Management Services

- Provider Management Services

- Billing And Accounts Management Services

- Analytics And Fraud Management Services

- HR Services

By End-User:

- Private Payers

- Public Payers

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

Egypt Soft Tissue Repair Market Analysis

Healthcare Services

Spain In Vitro Fertilisation (IVF) Service Market Analysis

Healthcare Services

UAE Revenue Cycle Management Software Market Analysis

Related reports (by geography)

Rare Diseases

Italy Wilson's Disease Drugs Market Analysis

Healthcare Services

Italy Prenatal Testing & Newborn Screening Market Analysis

Rare Diseases

Italy CDKL5 deficiency disorder (CDD) market Analysis

Pharmaceuticals