Healthcare Services

Italy Influenza Diagnostic Market Analysis

Italy Influenza Diagnostic Market is projected to grow from $xx Mn in 2023 to $xx Mn by 2030, registering a CAGR of xx% during the forecast period of 2023 - 2030. The market for Influenza diagnostics is expanding as a result of rising healthcare spending in both developed and developing nations. This demand is fueling the development of better diagnostic tools and methods for the early detection and accurate diagnosis of Influenza. Some of the key players in the global Influenza Diagnostics Market include 3M; Abbott Laboratories, Inc.; Becton, Dickinson, and Company (BD); Meridian Bioscience, Inc.; Quidel Corporation; F. Hoffmann-LA Roche AG; SA Scientific; Sekisui Diagnostics; Thermo Fisher Scientific, Inc.; Hologic, Inc.

Buy Now

Italy Influenza Diagnostic Market Executive Summary

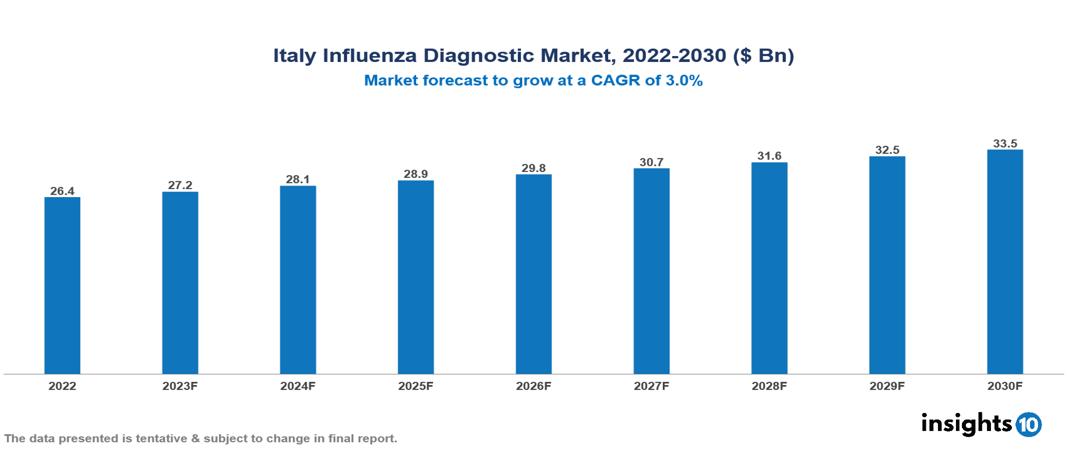

Italy Influenza Diagnostic Market is valued at around $26.4 Bn in 2022 and is projected to reach $33.4 Bn by 2030, exhibiting a CAGR of 3% during the forecast period 2023-2030.

Influenza Diagnostic Market refers to the market for tests and methods used to diagnose Influenza disease, which is a highly infectious respiratory disease with symptoms of fever, cough, sore throat, runny nose, body aches, headache, and fatigue. The market includes different types of tests and devices which are analyzed for the diagnosis of different strains of the Influenza virus.

The prevalence of Influenza is increasing globally, according to WHO around 304 Mn to 656 Mn people suffer from influenza. WHO estimates that around 4,00,000 to 9,00,000 people died from influenza in 2022 and the highest burden of influenza is in adults over 65 years of age.

There are many global players in the Influenza Diagnostic market but 3M; Abbott Laboratories, Inc.; Becton, Dickinson, and Company (BD); Meridian Bioscience, Inc.; Quidel Corporation; F. Hoffmann-LA Roche AG; SA Scientific; Sekisui Diagnostics; Thermo Fisher Scientific, Inc.; and Hologic, Inc. are some of the major players in Influenza Diagnostic Market.

Influenza is diagnosed using a variety of diagnostic procedures and tests, including rapid antigen tests, molecular assays, viral cultures, serological tests, next-generation sequencing (NGS), and rapid molecular assay testing. All these techniques are used according to requirements and availability of the resources for the diagnosis of Influenza.

The increasing prevalence of Influenza, aging global population and increasing co-morbidities, technological advancements, and increasing demand for Point-of-Care testing is projected to fuel the Influenza diagnostic market in coming years. The market still has many difficulties like complex regulatory procedures, limited reimbursement coverage, high cost of advanced diagnostic procedures, and lack of accuracy of rapid antigen tests.

Market Dynamics

Drivers of Italy Influenza Diagnostics Market:

Growing Prevalence of Influenza: Influenza is a highly contagious respiratory disease and its prevalence is also higher which is growing each year. According to WHO in the year 2022, There were around 304 Mn to 656 Mn cases of influenza globally. Increasing prevalence is leading to substantial demand for accurate and timely diagnosis of influenza.

Increasing Geriatric Population and Co-Morbidities: With the increasing age of individuals their immunity decreases and their chances of getting infected with the influenza virus also increase. The highest burden of influenza is in adults aged over 65. People with chronic illnesses like cardiovascular disease, diabetes mellitus, and lung disorders are more prone to contracting influenza infection. All these factors influence the diagnostic market of Influenza.

Technological Advancements in Diagnostic Tests: There have been advancements in tests like rapid antigen tests, molecular assays, and PCR-based tests which have improved the efficiency and accuracy of diagnosis of Influenza.

Government measures and support: Governments throughout the world are supporting research to create efficient diagnostic tools and techniques and taking measures to increase awareness of Influenza, which is also propelling the growth of the Influenza Diagnostics Market.

Increasing Demand for Point-of-Care Testing: It helps in rapid and convenient diagnosis which leads to immediate treatment decisions. Demand for Point-of-Care Test kits is increasing in primary health care setups, emergency departments, and rural areas which provides quick results and helps in reducing transmission of disease to larger communities. This demand for rapid testing is driving the diagnostic market for Influenza.

Restraints in Influenza Diagnostics Market:

Seasonal Nature of Influenza: Influenza is a seasonal disease and has a relative duration, with outbreaks occurring during specific time periods. After that duration incidence of Influenza is very low which can fluctuate the growth of the Influenza Diagnostic Market.

Limited Accuracy of Rapid Antigen Test: It gives quick results but in terms of accuracy it is very low compared to molecular assay tests like PCR. Sensitivity and specificity also as it give false-negative and false-positive results. It impacts the reliability of tests leading to misdiagnosis or delayed diagnosis of influenza.

Cost Constraints and Reimbursements Issues: Some tests like advanced molecular assays are more costly compared to rapid antigen tests, which can limit the adoption of these diagnostic tests. Reimbursement policies for the diagnosis of Influenza have very limited coverage which also hampers the growth of the diagnostics market for influenza.

Regulatory Challenges: For the development and commercialization of diagnostic tests, regulatory processes are complex and time taking. Certain standards for safety, efficacy, and quality assurance are very stringent and it requires a lot of time and money to complete all the procedures. All these factors can hamper the growth of the Influenza Diagnostic Market.

Key players

Roche Diagnostics S.p.A. Abbott Diagnostics Italy S.r.l. Thermo Fisher Scientific Italy S.p.A. Quidel Italy S.r.l. Hologic Italy S.r.l. BD (Becton, Dickinson and Company) Italy Luminex Corporation Italy S.r.l. DiaSorin S.p.A. Cepheid Italy S.r.l. Sekisui Diagnostics Italy S.r.l.1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Market Segmentations For Italy Influenza Diagnostic Market

By Product:

- Test Kit and Reagents

- Instruments

- Other Products

By Test Type:

- Molecular Diagnostic Tests

- Transcription-Mediated Amplification-Based Assay

- Loop-Mediated Isothermal Amplification-Based Assay

- Nucleic Acid Sequence-Based Amplification Tests

- Other Isothermal Nucleic Acid Amplification Tests

- Traditional Diagnostic Tests

By End-User:

- Diagnostic Laboratories

- Hospitals and Clinics

- Other End-Users

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

India HIV Diagnostic Market Analysis

Healthcare Services

Germany Retirement Communities Market Analysis

Healthcare Services

Japan Gene Editing Market Analysis

Related reports (by geography)

Healthcare Services

Italy Plastic Healthcare Packaging Market Analysis

Healthcare Services

Italy Liquid Biopsy Market Analysis

Healthcare Services

Italy Body Fat Reduction Market Analysis

Healthcare Services