Pharmaceuticals

Italy Infectious Disease Therapeutics Market Analysis

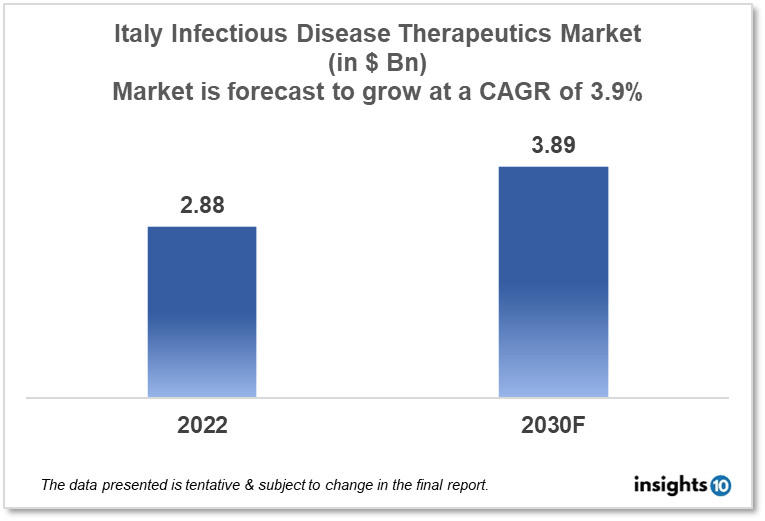

By 2030, it is anticipated that the Italy infectious disease therapeutics market will reach a value of $3.89 Bn from $2.88 Bn in 2022, growing at a CAGR of 3.9% during 2022-2030. Infectious Disease Therapeutics in Italy is dominated by a few domestic pharmaceutical companies such as Menarini, Dompé and IRBM. The infectious disease therapeutics market in Italy is segmented into different therapeutic areas and different treatment types. The major factors affecting the Italy infectious disease therapeutics market are the increasing disease burden of communicable diseases like TB, hepatitis, and COVID-19 and the amount of healthcare funding for infectious diseases treatment in various areas of Italy.

Buy Now

Italy Infectious Disease Therapeutics Analysis Summary

By 2030, it is anticipated that the Italy infectious disease therapeutics market will reach a value of $3.89 Bn from $2.88 Bn in 2022, growing at a CAGR of 3.9% during 2022-2030.

Italy is a high-income, developed country located in Southern Europe comprising the boot-shaped Italian peninsula and a number of islands including Sicily and Sardinia. According to the World Health Organization, approximately 3,000 cases of tuberculosis were reported in Italy in 2019. The conventional TB treatment includes a cocktail of medications such as isoniazid, rifampicin, ethambutol, and pyrazinamide. According to WHO, the effective treatment coverage for tuberculosis in Italy was at 82 %.

With an average of 28.1 defined daily doses (DDD) per 1,000 inhabitants per day in 2019, Italy has one of the highest antibiotic usage rates in Europe. This is higher than the average for the European Union of 20.3 DDD per 1,000 population per day. Italy's government spends 9.6 % of its GDP on healthcare in 2020.

Market Dynamics

Market Growth Drivers Analysis

With the ongoing COVID-19 pandemic, there is a heightened interest in the development of antiviral treatments to treat and prevent the spread of viral illnesses. This includes COVID-19 as well as other viral illnesses like influenza, hepatitis B and C, and HIV. Tuberculosis (TB) is growing more widespread in Italy, particularly among high-risk groups such as refugees and people with compromised immune systems. In Italy, the manufacturing industry is still highly valued. These characteristics could enhance Italy infectious diseases therapeutics market.

Market Restraints

In recent years, Italy has suffered economic issues, which may have an impact on patients' capacity to receive and buy infectious illness medicines. This may limit the potential market for these treatments and make income generation challenging for pharmaceutical corporations. Infectious disease therapies face intense competition from other pharmaceutical companies as well as other therapy options such as vaccines and antibiotics. The prevalence of tiny, low-productivity businesses (more than 90 % of firms have 10 employees or less). These factors may deter new entrants into the Italy infectious disease therapeutics market.

Competitive Landscape

Key Players

- IRBM: IRBM is a research organization, specializes in drug discovery and development, with a focus on infectious diseases. IRBM is currently working on a COVID-19 vaccine

- Menarini: Menarini is a multinational pharmaceutical company based in Florence, Italy. The company develops and manufactures drugs for various diseases, including infectious diseases

- Dompé: Dompé is a biopharmaceutical company based in Milan, Italy. The company specializes in the development of drugs for rare diseases and infectious diseases, including COVID-19

- MolMed: MolMed is a biotechnology company based in Milan, Italy. The company focuses on the development of cell and gene therapies for various diseases, including infectious diseases

- VisMederi: VisMederi is a contract research organization based in Siena, Italy. The company specializes in the development and validation of assays for the evaluation of vaccines and drugs for infectious diseases

Recent Notable Updates

January 2022: Dompé farmaceutici ("Dompé"), a biopharmaceutical company, announced a strategic collaboration and investment in Engitix Ltd 'Engitix,' a biopharmaceutical company with a pioneering and proprietary human extracellular matrix (ECM) drug target discovery platform, as part of Engitix's $54 Mn Series A financing.

Healthcare Policies and Reimbursement Scenarios

The Italian Medicines Agency (AIFA) is in charge of regulating infectious illness treatments in Italy. Preclinical testing, clinical trials, and marketing authorisation are all stages of the approval procedure for infectious disease treatments in Italy. Other regulatory agencies in Italy, in addition to AIFA, may be involved in the regulation of infectious disease medicines. The National Institute of Health (ISS), for example, is in charge of determining the safety and efficacy of vaccinations and other biological products.

The reimbursement of infectious illness treatments in Italy is mostly governed by the National Health Service (Servizio Sanitario Nazionale, SSN). The SSN, which is sponsored by the government and regional authorities, provides universal healthcare coverage to all citizens and legal residents.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Infectious Disease Therapeutics Segmentation

By Mode of Treatment (Revenue, USD Billion):

- Vaccines

- Drugs

By Applications (Revenue, USD Billion):

- HIV/AIDS

- Influenza

- Hepatitis

- Malaria

- Tuberculosis

- Others

By Disease Type (Revenue, USD Billion):

- Viral Diseases

- Bacterial Diseases

- Fungal Diseases

- Parasitic Diseases

- Others

By Target Organism (Revenue, USD Billion):

- Antibiotics

- Antivirals

- Antifungals

- Anti-Parasitic

- Others

By End User (Revenue, USD Billion):

- Hospitals and Clinics

- Ambulatory Care Centers

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

The Italian Medicines Agency (AIFA) is in charge of regulating infectious illness treatments in Italy.

The reimbursement of infectious illness treatments in Italy is mostly governed by the National Health Service (Servizio Sanitario Nazionale, SSN).

Infectious Disease Therapeutics in Italy is dominated by domestic pharmaceutical companies such as Menarini, Dompé and IRBM.

Related reports (by category)

Pharmaceuticals

Middle East Lung Cancer Therapeutics Market Analysis

Pharmaceuticals

Russia Infectious Disease Therapeutics Market Analysis

Pharmaceuticals

Italy Infectious Disease Therapeutics Market Analysis

Related reports (by geography)

Healthcare Services

Italy Cholesterol Testing Service Market Analysis

Medical Devices

Italy 3D Printing Medical Devices Market Analysis

Rare Diseases

Italy Adrenoleukodystrophy (ALD) Drugs Market Analysis

Healthcare Services