Pharmaceuticals

Italy Diabetes Therapeutics Market Analysis

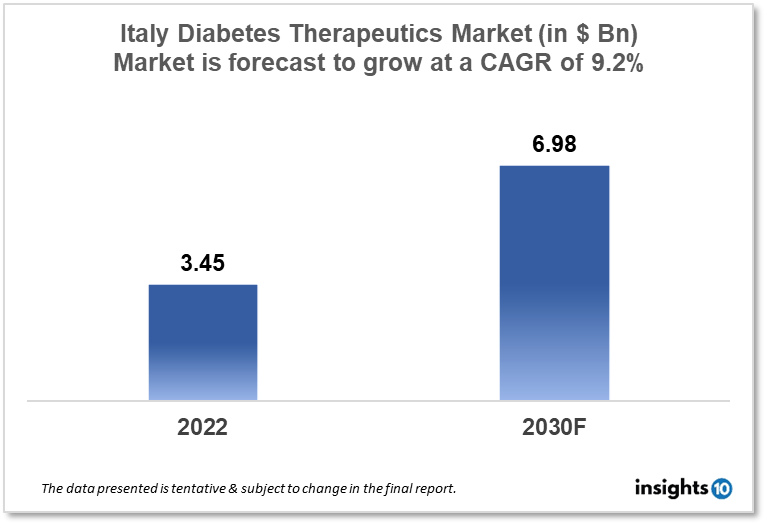

Italy's diabetes therapeutics market is expected to grow from $3.45 Bn in 2022 to $6.98 Bn in 2030 with a CAGR of 9.2% for the forecasted year 2022-30. The rise in the geriatric population in Italy as well as the development of new technological advancements in diabetes care are the main growth drivers in the market. The Italy diabetes therapeutics market is segmented by type, application, drug, route of administration, and distribution channel. Icrom, AmypoPharma, and Farmaka are the major players in the Italy diabetes therapeutics market.

Buy Now

Italy Diabetes Therapeutics Market Executive Analysis

Italy's diabetes therapeutics market is expected to grow from $3.45 Bn in 2022 to $6.98 Bn in 2030 with a CAGR of 9.2% for the forecasted year 2022-30. The Italian government has allocated €125 Bn to the national health system due to staff gaps and lengthy treatment wait lists. Healthcare facilities across Italy suffer from a severe staffing shortage, particularly in emergency rooms, which has resulted in long waiting lines for patients seeking treatment. In Italy, state healthcare spending peaked during the pandemic at 7.5% of GDP, while private healthcare spending peaked at 2.3% of GDP in 2021. Healthcare costs are projected to increase by 6.4% in 2024.

In Italy, 5.3% of the population, or more than 3 Mn 200 thousand individuals, reported having diabetes (16.5% of those 65 and older). In the past thirty years, the frequency of self-reported diabetes has nearly doubled. A number of new anti-diabetic medications (ADs) have entered the market over the past ten years with different clinical efficacy, profiles, and costs, allowing doctors to customize treatment for each patient. With numerous studies demonstrating a shift in specific drug utilization patterns and an increase in Type 2 Diabetes (T2DM) prescribing over time, the prevalence of T2DM has been steadily rising, and the availability of these new medications has led to increased AD utilization and associated costs in Italy.

Metformin and sulfonylureas (53% of patients) and metformin and sitagliptin (12.6%) were the two medications fixedly given for diabetes in Italy. Metformin and sulfonylureas were used as the first component of free combination treatment by about 50% of patients, with metformin and repaglinide as the second component in 15% of cases. The last family of anti-diabetic medications to receive FDA and EMA approval is known as SGLT-2 (sodium-glucose cotransporter-2) inhibitors, which can be used regardless of the stage of T2DM. SGLT-2 inhibitors are appropriate for patients with long-standing diabetes and -cell function impairment because they reduce the renal threshold for glucose excretion and inhibit renal glucose reabsorption through insulin-independent mechanisms. Beyond glycemic control, SGLT-2 inhibitors may help lower blood pressure due to their osmotic diuretic impact and have the ability to help people lose weight due to the calories lost through glycosuria.

Market Dynamics

Market Growth Drivers

The rise in Italy's geriatric population is responsible for the expansion of the Italy diabetes therapeutics market. As people get older, they are more likely to develop diabetes, especially type 2. Significant technological advancements are being observed in the diabetes therapeutics market, including the development of novel insulin delivery systems, continuous glucose monitoring systems, and other cutting-edge therapies. The market in Italy is anticipated to expand as a result of these developments. The introduction of diabetes screening programs and increased financing for diabetes research are just two of the initiatives the Italian government has put in place in order to enhance the nation's diabetes care. By raising awareness of the condition and the available choices for treatment, these initiatives are anticipated to spur Italy's diabetes therapeutics market expansion.

Market Restraints

Drug patent expirations during the forecast period are expected to have an impact on the market growth for diabetes therapies. The process of developing new drugs is heavily funded by pharmaceutical firms. In contrast to the original brand of the drug, the prices of the generic versions are affordable. This has a detrimental effect on the market's total value growth. Diabetes therapy can be costly, and many Italian patients might not be able to cover the price of innovative treatments. This might restrict the use of novel therapies and prevent Italy's diabetes therapeutics market expansion.

Competitive Landscape

Key Players

- Medexport (ITA)

- Mipharm (ITA)

- Icrom (ITA)

- AmypoPharma (ITA)

- Farmaka

- Astrazeneca

- Boehringer Ingelheim

- Eli Lilly

- Glaxosmithkline

- Novartis

- Novo Nordisk

Healthcare Policies and Regulatory Landscape

The state organization in charge of drug regulation in Italy since 2004 is the Italian Medicines Agency (Agenzia Italiana del Farmaco, or AIFA). It is a public organization that operates independently, openly, and in accordance with cost-effectiveness standards, under the supervision of the Ministry of Health and the Ministry of Economy. The objective is to establish fair pharmaceutical policies and ensure their consistent national application, promoting good health through medication, regulating the value and expense of medications, and encouraging the advancement of pharmaceutical research. The relationship with the organizations of other Member States, the European Medicines Agency (EMA), and other international entities is enforced while encouraging investments in research and development in Italy. It interacts with the patient group, scientific medicine, pharmaceutical firms, and distributors. In order to make sure that medicines approved for use in Italy adhere to European Union guidelines for safety and efficacy, AIFA also closely collaborates with the European Medicines Agency (EMA).

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Diabetes Therapeutics Segmentation

By Type (Revenue, USD Billion):

- Diabetes 1

- Diabetes 2

By Application (Revenue, USD Billion):

- Preventive

- Prediabetes

- Nutrition

- Obesity

- Lifestyle Management

- Treatment/Care

- Diabetes

- Smoking Cessation

- Musculoskeletal Disorders

- Central Nervous System Disorders

- Cardiovascular Disease

- Medication Adherence

- Chronic Respiratory Disorders

- Gastrointestinal Disorders

- Rehabilitation

- Substance Use Disorders & Addiction Management

By Drug (Revenue, USD Billion):

- Oral Anti-diabetic Drugs

- Insulin

- Non-insulin Injectable Drug

- Combination Drug

By Route of Administration (Revenue, USD Billion):

- Oral

- Subcutaneous

- Intravenous

By Distribution Channel (Revenue, USD Billion):

- Online Pharmacies

- Hospital Pharmacies

- Retail Pharmacies

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Icrom, AmypoPharma, and Farmaka are the major players in the Italy diabetes therapeutics market.

The Italy diabetes therapeutics market is expected to grow from $3.45 Bn in 2022 to $6.98 Bn in 2030 with a CAGR of 9.2% for the forecasted year 2022-2030.

The Italy diabetes therapeutics market is segmented by type, application, drug, route of administration, and distribution channel.

Related reports (by category)

Pharmaceuticals

Japan Seasonal Flu Vaccine Market Analysis

Pharmaceuticals

Finland Cardiovascular Drugs Market Analysis

Related reports (by geography)

Pharmaceuticals

Italy Oncology Therapeutics Market Analysis

Rare Diseases

Italy Hunter Syndrome Therapeutics Market Analysis

Clinical Trials